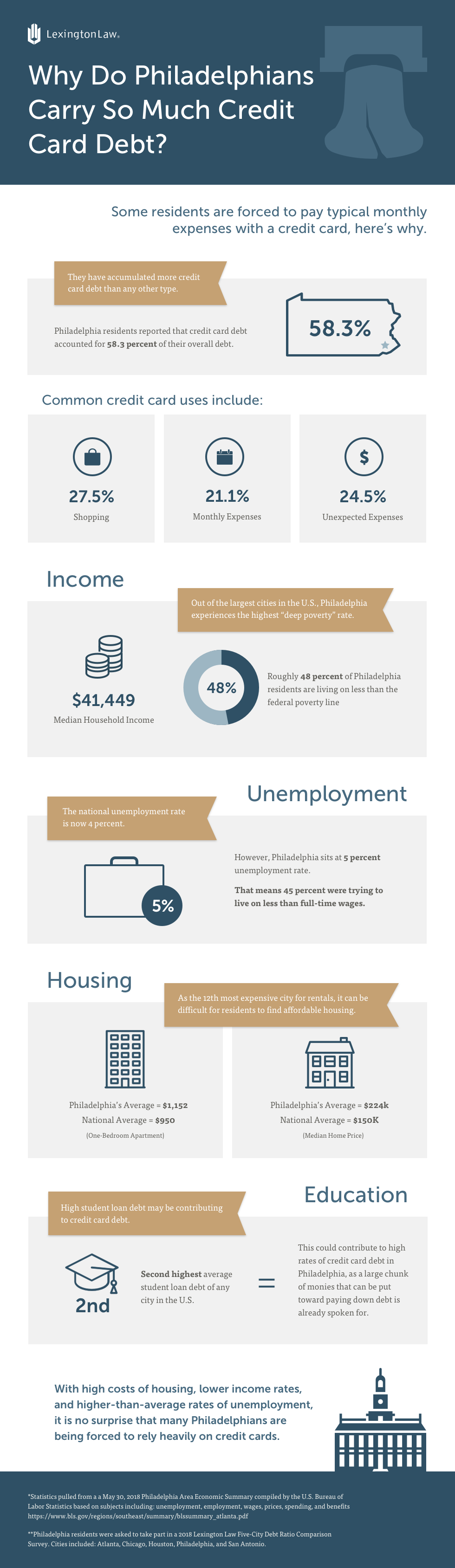

Philadelphia is known for many things: good food, rich history, and… credit card debt? While that may not be something the City of Brotherly Love is commonly known for, it is true: according to a recent Lexington Law survey of residents of five major U.S. cities, Philadelphia residents reported that credit card debt accounted for 58.3 percent of their overall debt. They have accumulated more credit card debt than any other type, and overall, they are supporting more credit card debt than any other city’s residents.

Credit card debt differs from student loan debt, mortgage debt, and personal loan debt, in that it is theoretically completely avoidable simply by living within one’s means. Most people recognize it is best to rely on savings for large purchases or emergencies, and to refrain from spending more than they can afford on high-interest credit cards. However, that being said, unexpected unavoidable expenses — such as car repairs or medical bills — do often need to go on a credit card.

Digging deeper, though, many Philadelphia residents claimed to have routinely used their credit cards for shopping (27.5 percent) or monthly expenses (21.1 percent). Just 24.5 percent of cardholders reported having used their card for unexpected expenses such as car repairs or minor medical charges.

So why are so many Philadelphians choosing to use credit cards in this way? Additionally, why are some residents forced to pay typical monthly expenses with a credit card? Let us examine living conditions, including income, unemployment, housing costs, and education in the city of Philadelphia to find out more.

Although it is one of the 25 largest cities in the U.S., the median household income in Philadelphia is on the lower end, at $41,449. (For reference, the highest median household income was $103,801 in San Francisco, CA, and the lowest was $25,980 in Detroit, MI.) So what does this mean? Urban living is expensive, regardless of the city. Considering the cost of living (which we will dive into more deeply later on), it is hard for residents of Philadelphia to make ends meet.

In order to make it to the top one percent of income earners in the city, a household must bring home $489,305 annually. This is much higher than the national average of $389,436.

Out of the largest cities in the U.S., Philadelphia experiences the highest “deep poverty” rate, which is defined as income at half the poverty line or less. As of 2018, the federal poverty line is $25,100 for a family of four. From this, we know that roughly 48 percent of Philadelphia residents are living on less than the federal poverty line, and 12 percent of them are considered to be in deep poverty, which may contribute to the high credit card debt rates. The income disparity in the city of Philadelphia is stark: the top one percent must make far more than the national average, and the bottom 12 percent are living so far below the poverty line, making ends meet is next to impossible.

While the economy seems to have recovered nicely from the Great Recession, and unemployment rates across the country have continued to decrease, there are still those who are unemployed or underemployed. The national unemployment rate is now 4 percent. However, the unemployment rate in Philadelphia sits at 5 percent. While this is the lowest recorded rate of unemployment in the Philadelphia metro area since 1990, it is still higher than the national average.

Of course, being employed does not automatically translate to having adequate employment. According to our survey, only 55 percent of respondents were employed full-time, and even they were having a hard time making ends meet on a monthly basis. That means 45 percent (of our admittedly small sampling of Philadelphians) were trying to live on less than full-time wages.

This is another factor contributing to the high amount of credit card debt carried by Philadelphians.

Even though unemployment rates are high compared to the national average, and income is lower than the national average, Philadelphia remains competitive and expensive when it comes to housing. As the 12th most expensive city for rentals, it can be difficult for residents to find affordable housing. The average one-bedroom apartment in Philadelphia will cost around $1,152; the national median price for a one-bedroom apartment is $950.

The situation is not much better for those hoping to own their homes. According to Zillow, the median home price in Philadelphia is $224,000, while home values actually hover around $149,600. So, even though some homes in Philadelphia may fall on the slightly more affordable side, they are still above the national median price of a home ($217,300). This is yet another possible indicator of why Philadelphians carry so much credit card debt: living in the city is very expensive, especially when compared with the other largest cities in the U.S. For many of those cities, even though housing costs are high, income and low rates of unemployment are able to offset said costs.

Lack of education in Philadelphia is not much of a factor in these other statistics; in fact, of those surveyed, the highest number (30.9 percent) claimed to have a bachelor’s degree, and 20 percent held either a master’s degree or a PhD. Of those who are currently in school, 64 percent were seeking either a bachelor’s degree or a master’s degree.

While these numbers do not appear to correlate with the amount of credit card debt, they definitely have an impact on student loan debt. In fact, Philadelphia students and recent graduates have the second highest average student loan debt of any city in the U.S. This could be a factor contributing to the high rates of credit card debt in Philadelphia, as a large chunk of monies that can be put toward paying down debt is already spoken for.

With high costs of housing, lower income rates, and higher-than-average rates of unemployment, it is no surprise that many Philadelphians are being forced to rely heavily on credit cards.

“Charged off as bad debt” means the lender has written off the account as a…

Credit freezes and credit locks both help prevent identity theft. Discover their differences, plus actionable…

Building a good credit score takes time—when building your credit from scratch, you can typically…

Late payments can stay on your credit report for up to seven years. We’ll show…

Our guide will teach you how to read a credit report so you can catch…

You can help improve your credit score by paying bills on time, keeping credit card…

{kind=link}

{kind=link}