Repairing your credit after divorce

August 15, 2024

Fallout from a divorce can negatively impact a person’s credit, so if you find yourself in the midst of a divorce, you should prepare for the financial toll and take steps to protect your credit.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Divorce can affect all areas of an individual’s life, including health and well-being, friendships, and finances. Even an uncontested divorce can be a drain on an individual’s income and savings. According to Forbes, the average cost of a divorce in the United States is between $15,000 and $20,000, which includes filing fees, mediation, serving papers, and retainers. On top of these costs, individuals may also need to pay for moving, securing a new place to live, buying basic necessities, and paying off shared debt.

Because it can be complicated to split expenses, even when both individuals agree to communicate and reach a mutual agreement, there’s still the potential for credit to be damaged. Learn how divorce can affect your credit and how you can work on credit repair after divorce.

How can divorce affect your credit?

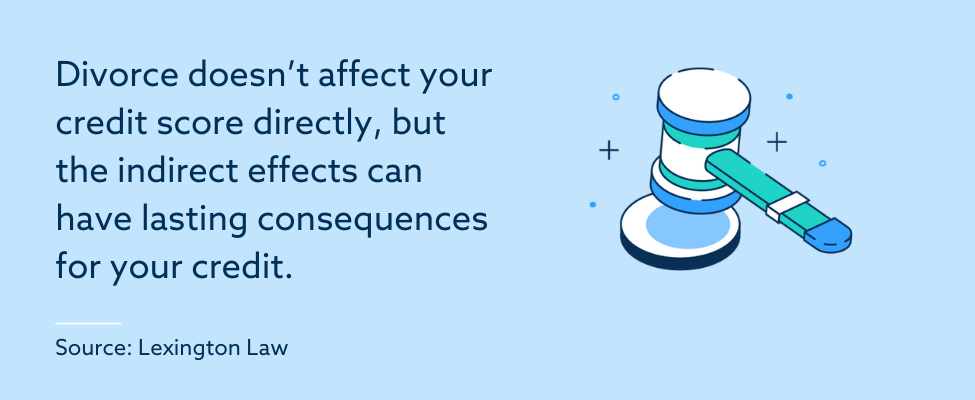

Divorce doesn’t affect your credit score directly, but the indirect effects can have lasting consequences for your credit. Going through a divorce can result in changes in household incomes, expenses and even current savings, so splitting up joint accounts, accessing your disposable income and knowing how to protect your credit can be huge factors in keeping your finances in check.

Joint accounts

A divorce decree often outlines which debts each individual is responsible for. However, lenders won’t necessarily know about your divorce decree or abide by it, meaning they may still hold you accountable for any joint accounts that your name is still on. If your ex forgets or deliberately refuses to make payments on time and in full on any of those accounts, it may negatively affect your credit too.

Credit utilization

According to many finance experts, a low credit utilization ratio is great for those trying to achieve or maintain good credit. This is the ratio of how much credit you’re using compared to how much total available credit you have. When you go through a divorce, it may be necessary to live off of credit, which can severely increase your credit utilization. To help prevent this, check your balances regularly and make sure you keep your utilization low.

Income

Divorce usually splits your family income in two, which results in lifestyle changes. This is especially true if your spouse was the primary breadwinner. This change in income can often make it harder to pay credit obligations on time, which can result in negative marks on credit reports.

Without your ex-spouse’s income to report when applying for new credit, you may find you don’t qualify, can’t secure prime rates or receive lower credit limits when you are approved.

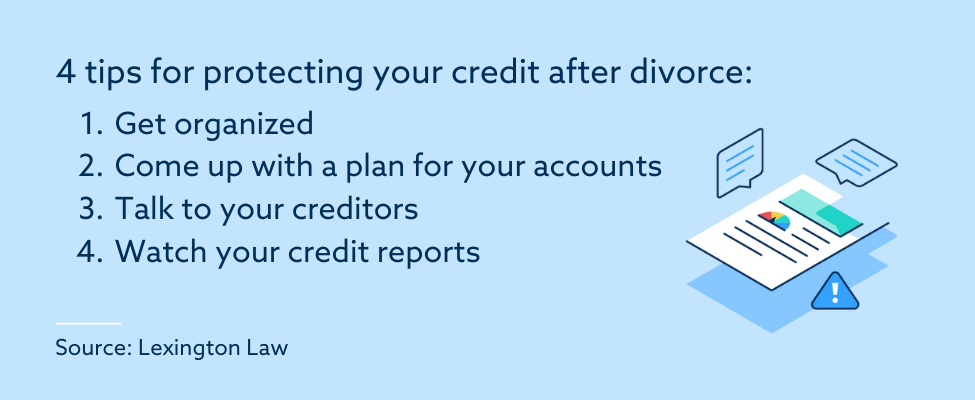

4 tips for protecting your credit after divorce

Fortunately, you can take some steps early on to maintain your credit during and after a divorce.

1. Get organized

Start by making a list of all relevant accounts, including joint bank accounts and credit obligations. Try to sit down with your ex, either through mediation or through personal contact, to discuss how the bills will be divided and who’s planning on assuming each debt.

2. Come up with a plan for your accounts

Ideally, you’ll want to pay off and close all joint accounts immediately. If you’ve chosen to split these accounts and continue to pay, it’s important to continue making payments on time. Make a new household budget and stick to it to help ensure you set aside money for these accounts.

3. Talk to your creditors

In some cases, you may be able to speak to your lenders to let them know you’re going through a divorce and need modifications to existing accounts. A loan modification is the term used to describe a change in an existing loan term. Loan modifications can reduce interest rates or convert a variable rate to a fixed interest rate.

They can also include a capitalization of specific amounts, meaning sometimes a bank or lender will add past-due amounts to the total balance of the loan, which gives you longer to pay and catches the account up to date. FHA mortgage lenders may also be willing to change or extend the terms of a loan from 30 to 40 years, which would lower the monthly mortgage payment, making it easier to handle.

If you expect any difficulties paying an existing account, it’s important to reach out to creditors before negative items end up on your credit reports. Reaching out early may make your lender more inclined to help.

4. Watch your credit reports

Pay close attention to your credit reports, looking for inaccurate and unfair items. You can contact the credit bureaus and set up fraud alerts. Fraud alerts require credit bureaus and lenders to contact you when anyone attempts to open a new line of credit in your name. If you can’t be reached to verify the account is yours, the application for credit is denied.

Strategies for repairing your credit after divorce

Rebuilding your credit after a divorce can be challenging and stressful, but there are steps you can take to help you improve your credit and ensure additional accounts aren’t created in your name.

First, be sure to keep your credit utilization low. Create a budget and avoid purchasing items on credit that you can’t afford. Make your payments on time and in full every month to prevent balances from increasing.

If you closed numerous accounts during your divorce, apply for a new line of credit solely in your name. While the initial hard inquiry can temporarily affect your credit, over time the new account can help you establish new payment history. In cases where the divorce has damaged your credit, try getting a cosigner, or apply for a secured card that can help you work to rebuild your credit.

Finally, seek out a credit repair service to help you with any credit issues the divorce caused. At Lexington Law, we can help you work to address inaccuracies on your credit reports, especially those that hurt your credit. We have several plans to suit every individual’s budget and needs.

Paola Bergauer was born in San Jose, California then moved with her family to Hawaii and later Arizona. In 2012 she earned a Bachelor’s degree in both Psychology and Political Science. In 2014 she graduated from Arizona Summit Law School earning her Juris Doctor. During law school, she had the opportunity to participate in externships where she was able to assist in the representation of clients who were pleading asylum in front of Immigration Court. Paola was also a senior staff editor in her law school’s Law Review. Prior to joining Lexington Law, Paola has worked in Immigration, Criminal Defense, and Personal Injury. Paola is licensed to practice in Arizona and is an Associate Attorney in the Phoenix office.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.