A 609 dispute letter is actually not a dispute but is simply a way of requesting that the credit bureaus provide you with certain documentation that substantiates the authenticity of the bureaus’ reporting.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

There’s nothing worse than finding inaccurate information on your credit report, especially if it’s dragging your credit score down. During your research, you may have read articles about a method of communicating with the credit bureaus called a “609 dispute letter.”

A letter sent to the bureaus requesting this information is actually not a dispute, but is simply a way of requesting that the credit bureaus provide you with certain documentation that substantiates the authenticity of the bureaus’ reporting. If the credit bureaus are unable to provide the requested documentation, it could indicate that the item may be inaccurate.

What is section 609?

Section 609 of the Fair Credit Reporting Act (FCRA) outlines a consumer’s right to order copies of their credit report and the information that appears on it. Section 609 doesn’t explicitly discuss your right to dispute inaccurate information, but it does assert your right to a copy of all the information in your credit file.

Understanding your rights is a major part of learning how to protect your credit reports. This is important because your credit score is based on the information in your credit reports and is an indicator of how responsible you are with your finances and your ability to pay bills on time.

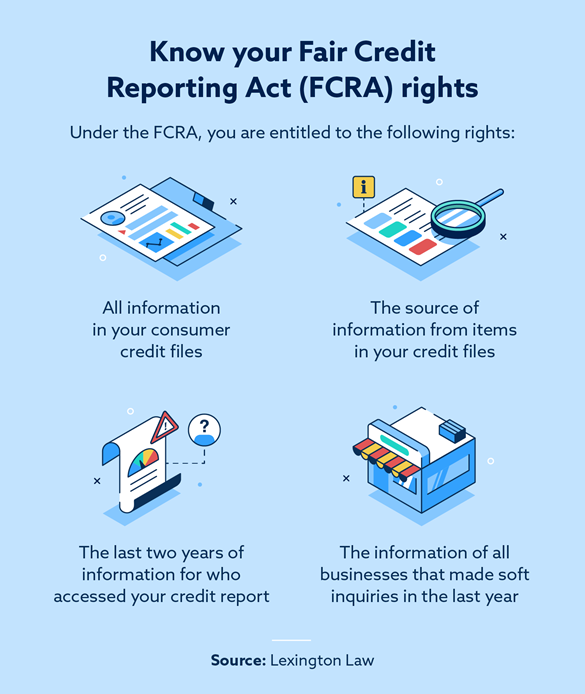

Under section 609, you have the right to request:

- All of the information in your consumer credit files

- The source of that information

- Each entity that has accessed your credit report within the past two years (unless it was to complete an investigation)

- Businesses that have made soft inquiries within the past year

Contrary to what some might think, section 609 does not require credit bureaus to provide proof of your accounts.

The FCRA gives you the right to dispute information you believe to be unfair, inaccurate or unsubstantiated. Credit reporting agencies are responsible for removing any disputed information that can’t be verified or confirmed. (So, if the information is found to be accurate, the bureaus aren’t required to remove it.) They’re also obligated to provide a description of the dispute process if you request it in writing.

609 letter template

There’s nothing proprietary about the format or wording of a 609 letter, although it does require your own documentation. There are a few 609 letter templates you can follow to ensure you are including the correct information.

Below is a sample of a typical 609 letter, as well as a downloadable PDF version that you can print:

Dear Credit Bureau (Experian, TransUnion, or Equifax),

I am exercising my right under the Fair Credit Reporting Act, Section 609, to request information regarding an item that is listed on my consumer credit report.

[List account names and account numbers]

Per section 609, I am entitled to see the source of the information, which is the original contract that contains my signature.

As proof of my identity, I have included copies of my birth certificate, Social Security card, passport, driver’s license, W-2, rental agreement, and cell phone bill. I have also included a copy of my credit report with the account I am requesting to have verified.

If you are unable to verify the account with the original contract, the information should be removed from my credit report within 30 days.

Sincerely,

[Signature]

[Printed name]

[Phone number]

[Address, Social Security number, date of birth]

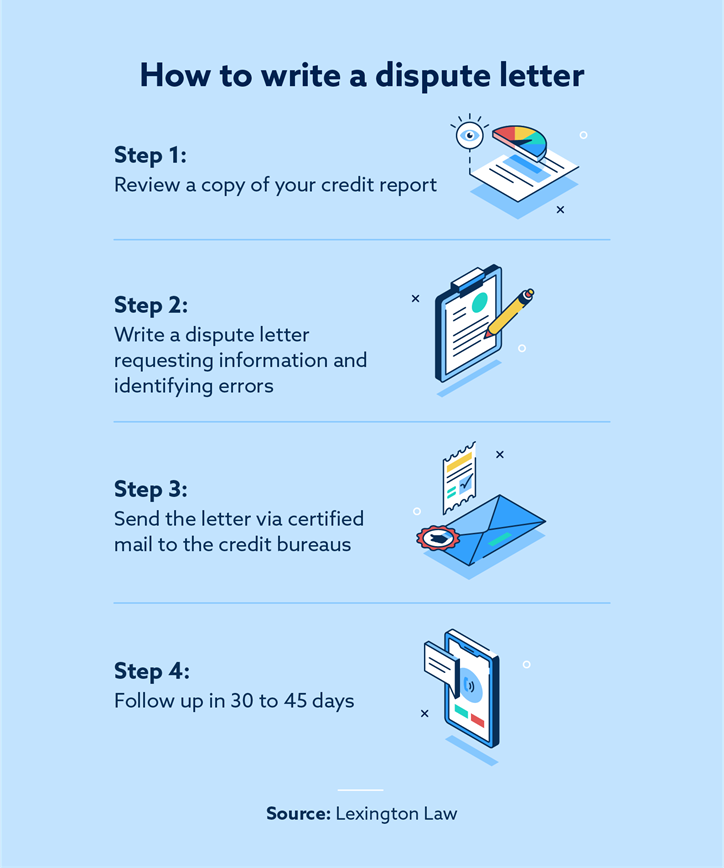

How to write a dispute letter

Credit dispute letters that work follow a simple process that you can do yourself. Below, we’ve listed the steps you can take to send a dispute letter regarding inaccurate information on your credit report.

Step 1: First, you’ll want to get a copy of your credit report, which will include a detailed list of positive and negative marks affecting your credit.

Step 2: Now that you know where the potential errors are, you can write your dispute letter that includes the following information:

- Name, address, phone number, and date of birth

- Statement asserting your rights under the FCRA

- Credit bureau account numbers and account names

- A copy of your credit report with specific items circled or highlighted

- Proof of identification like a government-issued ID

- Request for removal of unverifiable negative information

- Any additional documents that may help

Step 3: Once you have completed the letter, send the letter via certified mail so you receive a receipt upon delivery. To find the credit bureaus’ addresses, you can visit the Equifax®, Experian® and TransUnion® websites.

Step 4: Lastly, it may be helpful to follow up with the credit bureaus by phone if you have not heard from them within 30 to 45 days.

Why a 609 letter matters

Derogatory marks on your credit report can significantly affect your credit, which makes it difficult to acquire loans, rent a home, and sign up for services. Inaccurate information on your credit report can affect your personal finances, and sometimes these errors go unnoticed.

For example, if you make all of your credit card payments on time, but a late payment is reported in error, your score may drop by a significant number of points. This drop in your score can increase interest rates on any credit offers you get, which increases the overall cost of borrowing. It can also affect your ability to get a job, as some employers check your credit as part of the pre-employment screening process.

Are 609 letters effective?

There’s no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit report—it’s just another method of gathering information and seeking verification of the accuracy of the report. If disputes are successful, the credit bureaus may remove the negative item. Any accurate or verifiable information will stay on your credit report—a 609 letter doesn’t guarantee its removal. However, you may increase your chances of removal if you follow a 609 letter template and provide enough information.

The flaw in the 609 letter theory is that the FCRA doesn’t require credit bureaus to keep or provide signed contracts or proof of debts, meaning that the information could still be found valid even if the specific documents you’re looking for aren’t produced. If you need assistance with a credit reporting dispute, allow Lexington Law Firm to help. We have a team of consultants that could help challenge errors on your credit report, and we provide additional credit repair services as well. Get your free credit report consultation and learn more.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.