The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

In certain circumstances, an unapproved inquiry can be removed from your credit report by sending a credit inquiry removal letter to the credit reporting agency or by disputing it online.

Credit scores naturally fluctuate from month to month depending on your usage, payments and transactions. For the most part, your credit score is directly tied to your actions, but there may occasionally be errors on your report. If you notice a sudden decline in your credit score, even if only by a few points, you may be suffering from the effect of an unwarranted credit inquiry.

Credit inquiries occur when a lender requests your full credit history from one of the credit reporting agencies. These inquiries into your credit history can affect your credit negatively and will typically stay on your report for up to two years. Inquiries reflect how many times you have applied for credit, which helps lenders judge whether you should be approved for an extension of credit.

In certain circumstances, an unapproved inquiry can be removed from your credit report by sending a credit inquiry removal letter to the credit reporting agency or by disputing it online.

The difference between hard and soft inquiries

Although there is no difference between the data provided in a hard and soft inquiry, they do not affect your credit the same way. A common misconception is that checking your own credit will negatively affect your score, but this is not true. When you check your own credit, it is considered a soft inquiry and will not show on your credit report or affect your score.

Hard inquiries, by contrast, occur when a lender pulls your credit report. A lender may pull your credit history while going through an application for a new loan, a new credit card or any line of credit. Additionally, banks and property managers may pull your credit while setting up accounts or determining approval for an apartment.

Occasionally, a hard credit inquiry can sometimes be pulled without your knowledge, approval or full understanding. Hard inquiries that were pulled without your request may be removed from your credit report under the Fair Credit Reporting Act.

How do credit inquiries affect your credit score?

Hard inquiries account for 10 percent of your FICO credit score. Although the exact effect on your credit score will vary depending on your credit history and current standing, you can typically expect to see a temporary one to five point drop in your overall credit score.

Although the exact hit to your credit score will vary, you can expect to see drops in your score when these inquiries start to add up. Occasionally lenders will either pull your credit by mistake, pull your credit multiple times or pull your credit without your knowledge whatsoever.

5 reasons why there are hard inquiries on your credit report

Hard inquiries are the byproduct of applying for a loan, credit card or housing. Knowing how to remove inquiries from a credit report is important to your financial health, but knowing the causes of these inquiries can be just as important. Here are the most common sources of hard inquiries.

1. Credit card application

Applying for a new credit card will often be met with a hard inquiry to your credit report. Financial institutions need to determine if you’re financially responsible enough for a credit card, and your credit history can also influence the credit limit you are awarded.

One exception, however, is if you’re applying for another credit card within the same financial institution. In this case, they may only run a soft inquiry if you are in good standing with your other account.

2. Home or auto loan

Just as with credit cards, lending institutions need to determine financial health before issuing a home or auto loan to a consumer—and they often do so in the form of a hard inquiry.

It’s important to note that you will not be penalized for shopping around for favorable rates. Typically, any number of hard inquiries as a result of home or auto loan applications are counted as only one entry if they occur within 45 days of each other.

3. Housing application

If you are applying to rent a home or an apartment, the landlord or rental agency may perform a hard inquiry as part of their approval process.

That being said, hard inquiries in this instance are rare, as most rental agencies check credit with soft inquiries. If you are concerned about a hard inquiry when applying for housing, it’s best to reach out to management before submitting an application.

4. Other loans

There are more types of loans than just the home and auto loans outlined above—individuals can apply for personal loans, debt consolidation loans and a host of other options. Unless you are told differently, assume that any loan application will result in a hard inquiry at some point in the process.

5. Requesting a credit limit increase

There is a possibility that requesting a credit limit increase will result in a hard inquiry to your credit report. This is rare, as most financial institutions will perform a soft inquiry and look at previous utilization history, but you should check with your institution before applying for more credit.

Can you remove inquiries from your credit report?

Hard inquiries may be removed from your credit history if they occurred without your approval. If you did not have knowledge of the hard inquiries pulled on your credit profile, you have the right to ask for the inquiry to be removed.

You can request a hard inquiry be removed if:

- The inquiry occurred without your knowledge

- The inquiry occurred without your approval

- The number of inquiries exceeded what you expected

Will removing an inquiry improve your credit score?

Removing an inquiry could improve your credit score, but it depends on the type of inquiry and how old it is.

Soft inquiries have no effect on your credit score, so there is no need to remove them—in fact, you may not even see them on your credit report. Hard inquiries, on the other hand, can result in a credit score drop of up to five points per inquiry. Successfully removing these entries could boost your score depending on the overall health and utilization of your credit.

Additionally, the age of the inquiry should be taken into account. Hard inquiries can stay on your credit report for up to two years, but they typically only impact your score for six months to one year. Therefore, if you’re attempting to remove a hard inquiry that is more than one year old, it may not improve your credit score.

How to send a credit inquiry removal letter

To send a credit inquiry removal letter, you should contact any credit reporting agency that is reporting the inquiry. Credit inquiry removal letters can be sent to both the credit reporting agencies and the lender who issued the credit inquiry.

1. Notify the lender first

Notifying the lender before you send a removal notice is the proper first step for removing hard inquiries.

Make sure to send the credit inquiry removal letter via certified mail. This form of mail will give you proof that the credit issuer or lender received the appropriate first notification to remove the hard inquiry.

2. Include a copy of your credit report

Including a copy of your credit report with the highlighted unapproved hard inquiries may help others reference your dispute. Although the credit reporting agencies will have easy access to your report, a hard copy can help investigators when processing your request.

3. Send to the appropriate credit bureau

It is important to send your letter to the credit bureau with a record of the hard inquiry you want removed. Below are the addresses for each bureau:

Equifax

P.O. Box 740256

Atlanta, GA 30374-0256

Equifax Dispute Information Center

Experian

P.O. Box 4500

Allen, TX 75013

Experian Dispute Information Center

TransUnion LLC

Consumer Dispute Center

P.O. Box 2000

Chester, PA 19016

TransUnion Dispute Information Center

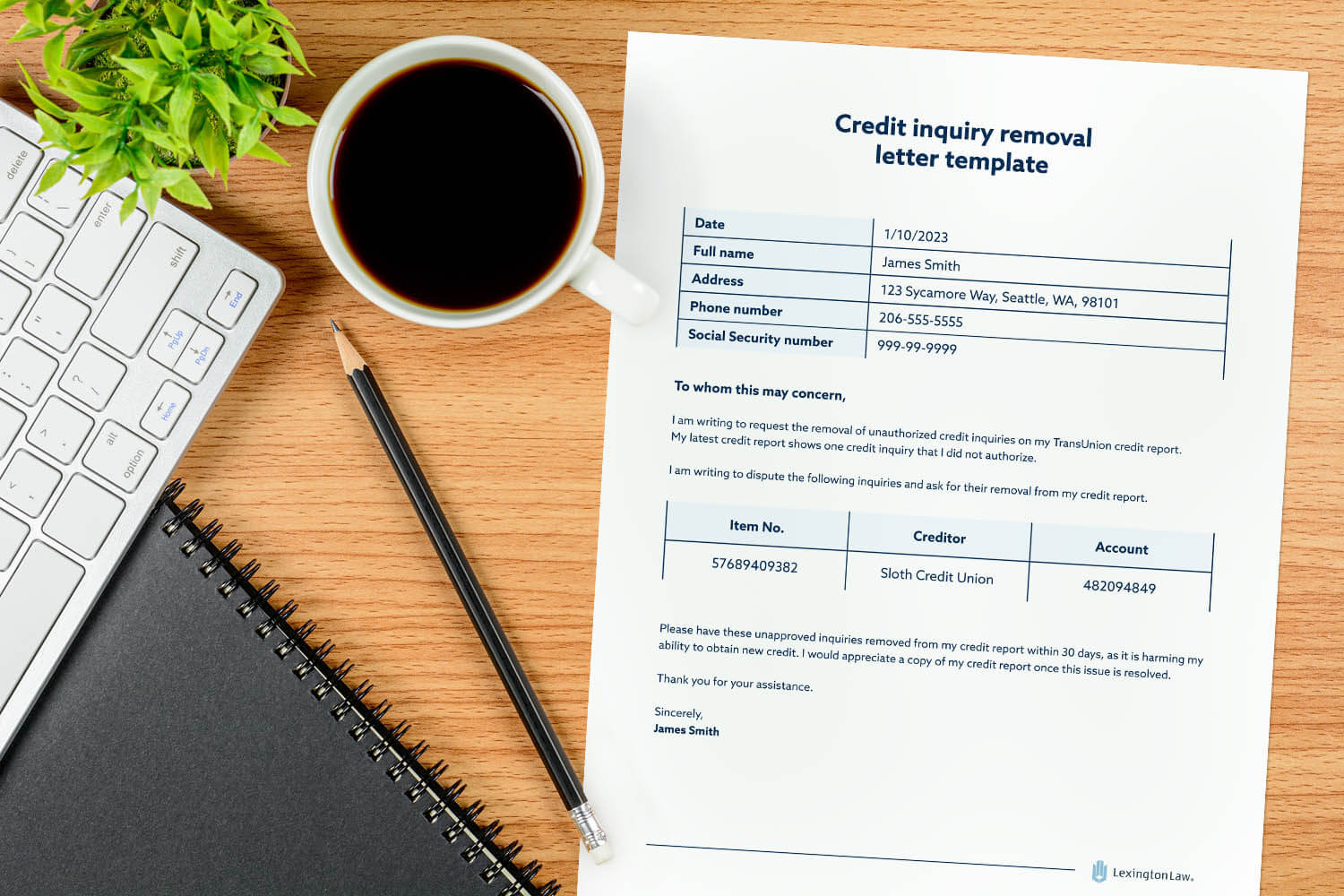

Credit inquiry removal letter template

Date

Your name

Your street number, street name

City, state, ZIP code

Your phone number

Social Security number

Name of credit bureau

Re: Reporting Unauthorized Credit Inquiry

To whom this may concern,

I am writing to request the removal of unauthorized credit inquiries on my (name of the credit bureau—Equifax, Experian and/or TransUnion) credit report. My latest credit report shows (number of hard inquiries you are disputing) credit inquiries that I did not authorize.

I am writing to dispute the following inquiries and ask for their removal from my credit report.

| Item No. | Creditor | Account |

|---|

Please have these unapproved inquiries removed from my credit report within 30 days, as it is harming my ability to obtain new credit. I would appreciate a copy of my credit report once this issue is resolved.

Thank you for your assistance.

Sincerely,

(Your Name)

How to stay on top of negative credit report items

Removing questionable negative items from your credit profile can be a long and time-consuming process that can seem daunting. Although a few points’ difference may not seem like a large priority, it is important to stay on top of these entries before they add up and get out of control.

If keeping your credit score high or improving your credit is a top priority, Lexington Law Firm might be a good option for you. Our credit repair services may help you with addressing questionable negative items on your credit report as you work on improving your credit.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.