What is a bad credit score? Tips for improving your credit

May 06, 2025

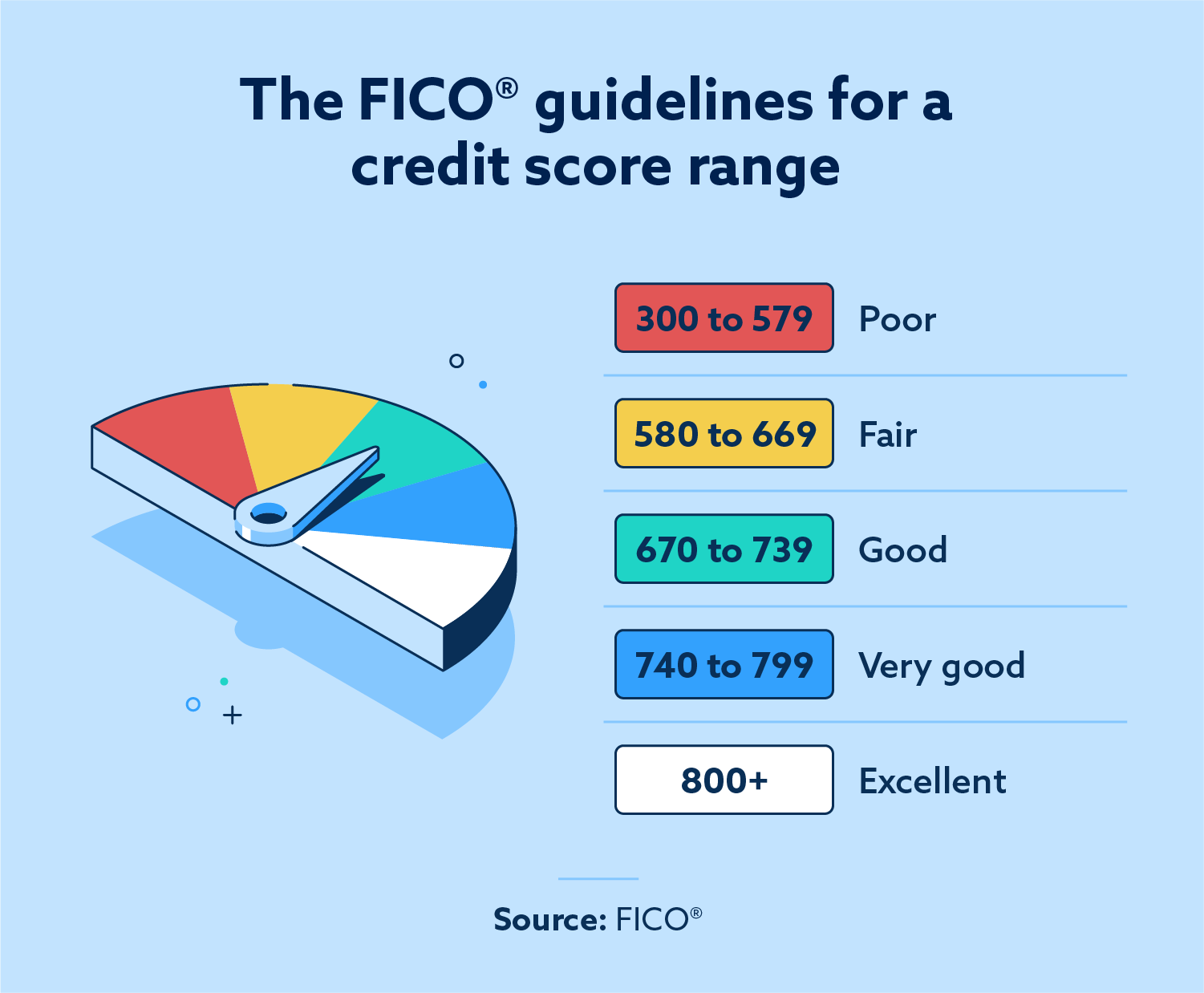

According to FICO®, a credit score between 300 and 579 is considered poor or bad, and scores between 580 and 669 are fair. Any score below 670 is generally considered a bad credit score, but there are ways to improve your credit.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Credit scores are represented on a scale from 300 to 850, and they’re used to give potential lenders a sense of an individual’s creditworthiness. A lower score means that someone is at greater risk of default, so lenders may choose to charge higher interest rates or not even extend credit to an individual with a low score at all.

Having a lower credit score can make it more difficult to access new credit like loans or credit cards. If you are able to get a loan or credit card with a poor score, you may end up paying very high interest rates that offset the risk the lender takes on by offering you credit.

Read on to get a better understanding of what leads to a poor credit score, how a poor credit score can affect you and what you can do to improve your credit.

What is a bad credit score?

So, what is a bad credit score? And what can you do if you want to improve your credit? Credit scoring models from FICO and VantageScore set the ranges for what is considered poor credit. That said, these same companies also transparently discuss what factors make up your credit score, so with the right financial moves, improving your score is entirely possible.

Here are the official numbers from FICO and VantageScore about what exactly a bad credit score is.

| What is a bad credit score? | |

|---|---|

| FICO | VantageScore |

| Poor (300-579) | Very Poor (300-499) |

| Fair (580-669) | Poor (500-600) |

| Good (670-739) | Fair (601-660) |

| Very Good (740-799) | Good (661-780) |

| Excellent (800-850) | Excellent (781-850) |

Most lenders use FICO to determine credit scores, but VantageScore is also sometimes used, so it’s helpful to know the ranges for both scoring models. In any case, a bad credit score, which is generally considered to be any score under 670, may not be a reflection of who you are as a person, but it can still have some negative effects on your life.

What is a bad FICO credit score?

As seen in the chart above, a credit score of 579 or below is considered bad or “poor” based on the FICO scale. On the other hand, your score must be 670 or above to have a good or “fair” FICO credit score.

What is a bad VantageScore credit score?

A “poor” or “subprime” VantageScore credit score is 600 or below, while a score below 500 is considered “very poor.” Your VantageScore credit score must be at least 661 to be considered good or “prime.”

What leads to a bad credit score?

While a poor credit score can have many causes, ultimately it comes down to problems with one of the five factors that make up your credit score.

Knowing these five factors can help you diagnose your own low score, and it can also help you make improvements. Here’s what makes up your score in order from greatest to least impact:

- Payment history (35 percent)

- Amounts owed (30 percent)

- Length of credit history (15 percent)

- Credit mix (10 percent)

- New credit (10 percent)

Combined, these five factors make up your credit score, with payment history and amounts owed representing the most significant portions.

As you think about the various negative items that can show up on your credit report, all of them are tied directly to one of the factors above. For instance, late payments can negatively affect your score because they reflect poorly on your payment history. Meanwhile, maxing out a credit card can also hurt your score because it can show that you have high credit utilization (which is a part of your “amounts owed”).

Here is a short list of reasons you may find yourself with a lower credit score:

- Late or overdue payments for loans, credit cards or medical bills

- Charge offs and collection accounts

- Maxed-out credit cards

- Bankruptcy

- Foreclosure or repossessions

- Identity theft

These negative items are recorded in your credit report, which lenders access when they consider your applications for loans or credit cards. In turn, these items often lower your credit score, which could be the reason that your applications are denied by potential lenders.

Negative items do eventually drop off your credit report, so responsible credit usage over time should slowly help your score despite any past negative items. That said, if any of the negative items listed on your credit report are inaccurate—perhaps due to identity theft—you have the right to dispute them. Working with a credit repair company may help you have incorrect negative items removed, potentially increasing your credit score.

Whatever the reasons for a poor credit score, it’s important to know how low credit can affect you and what you can do to fix it.

How can a bad credit score affect you?

A bad credit score is not a reflection of who you are as a person, but it can still have some negative effects on your life. Taking the time to determine why your score is low and what you can do about it now will spare you from the difficulties that come with having a poor score in the future.

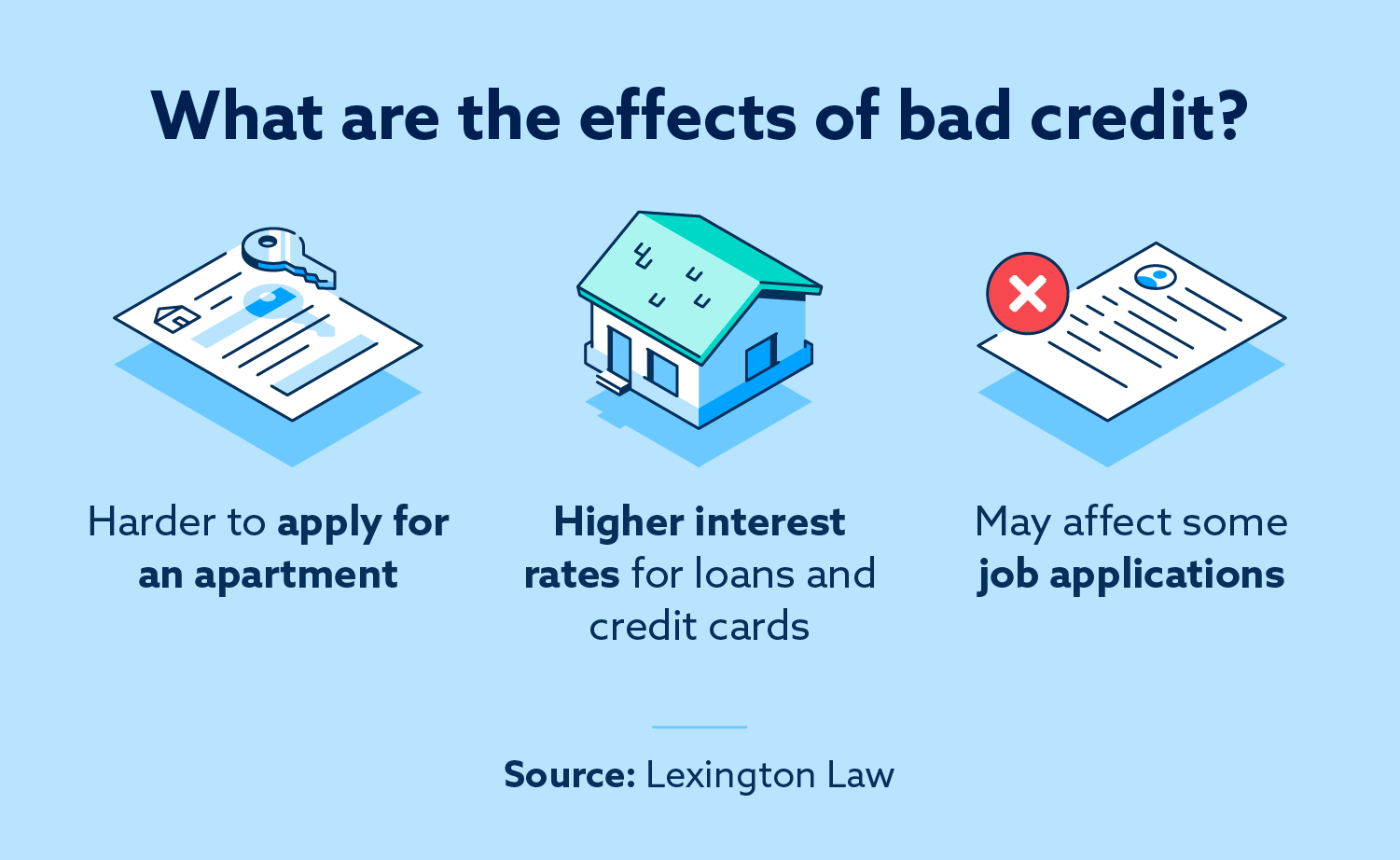

A bad credit score can lead to any or all of the following:

- Difficulty getting access to new credit like a loan or a credit card

- Trouble getting approved for a mortgage

- Higher interest rates for credit accounts

- Difficulty renting an apartment

- Problems with job applications that require a credit check

Most people lean on the credit system to make large purchases, especially cars and houses. A poor credit score can effectively shut you out from access to credit, making it difficult or impossible to make these important or even life-changing purchases.

Finding ways to improve your credit score now may help you benefit from a higher credit score when you need it most.

What can you do to improve your credit score?

If you have a low credit score, you can take steps to potentially improve your credit score. All of the following tips are important for anyone looking to improve their credit score. Credit scores are generally weighted to favor more recent information. Therefore, if you start building good credit habits now, then any past difficulties may eventually be overwritten by new successes.

Here are some steps to take to start improving your credit now:

- Get a copy of your credit reports. You can access a free credit report from each of the three credit bureaus—TransUnion®, Experian® and Equifax®—once each year at AnnualCreditReport.com. Knowing what’s on your report is the crucial first step to improving your score.

- Look up your credit score. Access your score through your bank, credit card provider or a free online service like Credit Karma. By knowing your current score, you can set goals for improvement and monitor how your changes are affecting you.

- Get a secured credit card. A secured credit card is backed by a deposit, so it’s typically a less risky option. Using one of these cards carefully over time can help boost your score.

- Consolidate your debt. You may need to consolidate your existing debt or use a balance transfer card to get your payments to a reasonable level.

- Make on-time payments. Once you’re able to make monthly payments on any existing debts, it’s important to pay on time and in full every month. Payment history is the most influential factor in your credit score, so stay on top of your payments.

- Be mindful of credit limits. Your credit score reflects how well you keep your credit spending below your credit limits. Aim to keep your credit card balances at 30 percent of your limit or less across all of your cards.

With diligence and responsible usage over time, you can improve your credit score. Doing so can open up a number of doors for you, including the potential to secure a car loan or mortgage with reasonable rates. Having a low credit score can cost you over time by robbing you of opportunities for jobs or apartments—or even costing you thousands of dollars more in interest payments.

A bad credit score can cause difficulties, but it isn’t a permanent number or a statement about who you are as a person. Take some time to evaluate your credit report to figure out where you can make changes that will positively influence your score. If you notice any inaccuracies or unfair items while reviewing your report, reach out to the team at Lexington Law Firm to see if they can help you repair your credit by disputing incorrect information with the credit bureaus.

Joe was born and raised in the south suburbs of Chicago, Illinois, but recently moved to Scottsdale, Arizona. Joe graduated Summa Cum Laude from the University of Illinois at Chicago, where he received his Bachelor of Science in Integrated Health Studies. He then earned his Juris Doctor Cum Laude from the University of Illinois College of Law. Before joining Lexington Law Firm, Joe gained legal experience working for a law firm in downtown Chicago that specializes in medical malpractice, toxic torts, and other civil litigation matters. Joe is licensed to practice law in Illinois and Arizona. In his free time, Joe enjoys playing hockey, hiking Arizona trails, and spending time with friends and family.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.