Secured credit cards can help build credit when used responsibly. These cards are also backed by a cash deposit that lenders use as collateral.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Secured credit cards can help you improve your credit if you use them regularly, pay off your full balance each month and keep your credit utilization low. With secured credit cards, borrowers place a deposit that also doubles as a credit. This deposit lets lenders issue secured cards to people with no credit history or bad credit.

This guide will explore the pros and cons of using secured credit cards and share several ways they can help build credit. We’ll also cover a few credit repair services that can aid individuals with low or no credit.

Key takeaways:

- Secured credit cards use an initial deposit as a credit limit.

- Secured credit cards often have higher than average APR.

- Making timely payments is the fastest way to build credit with a secured card.

What is a secured credit card?

A secured credit card is similar to a traditional card in most respects, except that secured cards are backed by a cash deposit that lenders use as collateral.

Not all lenders readily offer credit cards for bad-credit or no-credit applicants. However, a secured credit card is considered lower risk since cardholders borrow funds from their initial cash deposit. If a cardholder misses a payment, the lender can simply use their deposit to pay off the balance.

Here are a few key points to keep in mind with secured credit cards:

- Credit limit: The credit limit for a secured credit card is usually equal to the amount of cash you provide as a deposit.

- Annual percentage rate: The annual percentage rate (APR), or the interest rate your issuer will charge if you don’t pay off your monthly balance, is typically higher on a secured credit card.

- Goods and services: Similar to a traditional credit card, a secured credit card can be used to pay for goods and services, including many bills.

Using a secured credit card with good credit habits can help you improve your credit profile and apply for a better credit card or a loan.

How does a secured credit card work?

A person can use a secured credit card for virtually every instance they use a traditional card unless indicated otherwise in their cardholder agreement. Here’s an overview of how secured credit cards normally work:

- Once your application is approved, your secured credit card requires a cash deposit.

- Your purchases are backed by this deposit, reducing risk for the lender.

- Payments made on the card don’t come out of that deposit. You’ll need to pay your credit card balance with separate funds each month. Missed payments will still incur interest based on your card’s current balance.

As long as you pay off your balance, the deposit will be returned to you when you close the account. But if you don’t make payments on time, the deposit acts as collateral, and the lender will keep the deposit to pay what you owe.

What is the difference between a secured and an unsecured credit card?

An unsecured credit card requires no deposit or collateral to open. However, unsecured cards have much more stringent credit and income requirements for applicants. Think of your cash deposit as “securing” the credit you’ll borrow with a secured card.

Do secured cards build credit?

Responsibly using secured cards can steadily build and repair credit over time. FICO®, one of the primary credit score providers, ranks payment history as the most impactful factor when calculating credit scores. Consistently paying off the balance on your secured card will help your credit, while a missed or past-due payment can induce sharp decreases in your credit.

How long does it take to build credit with a secured credit card?

New credit accounts for 10 percent of your FICO score. Building credit from scratch can take up to six months, and if you already have credit, it can take many months of consistent, on-time payments on your secured credit card to see notable improvements.

How to get a secured credit card

Secured credit card applications aren’t very different from their unsecured counterparts. Here’s what you can expect from the application process.

Step 1. Shop around

Start by looking for secured credit cards with no annual fees—or, if necessary, a low annual fee. If you’re concerned about affording the deposit, you may want to look for options with minimums below $100. It’s also worthwhile to prioritize cards with the lowest APR possible in case you need to make partial balance payments.

Step 2. Apply for the card of your choice

Applications can usually be completed online in just a few minutes after providing basic personal information like your address, phone number, Social Security number and income.

Step 3. Make an initial deposit

To open your account, you’ll need to make a deposit that satisfies your approved minimum. This will either be the same amount or a little less than your credit limit.

Step 4. Make additional deposits if desired

Your lender may permit you to make additional deposits to raise your credit limit even higher.

Step 5. Make monthly payments

As with any credit card, you’ll need to continue making on-time payments—in full, if possible—to maintain good standing and build up your credit.

Banks that offer secured credit cards and secured credit card examples

Most of the major national banks, credit unions and credit card companies offer secured credit cards, including Bank of America, Citi, Wells Fargo and more. Here are a few examples of popular options:

- No credit history needed: The Citi® Secured Mastercard® has no annual fee, offers a 22.74 percent APR and requires no credit history for application.

- Cash back: The Discover it® Secured Credit Card carries no annual fee, comes with a 28.24 percent APR and offers 1 percent cash back on all purchases plus an extra 2 percent on gas station and restaurant purchases.

- High credit limit: For those who can make a $49, $99 or $200 security deposit, Capital One’s Platinum Secured Mastercard® offers up to a $1,000 credit limit with no annual fee and with a 30.74 percent APR.

- Credit union: Digital Federal Credit Union’s Visa® Platinum Secured Credit Card boasts a 16.75 percent APR and no annual fee but does require membership in the credit union.

How to use a secured credit card to rebuild credit

Once you have a secured credit card, you can begin using it to build or improve your credit, which could ultimately lead you on a path to a good credit score and the opportunity to get a car loan or mortgage with favorable rates. Here are a few tips for using your card effectively to build credit.

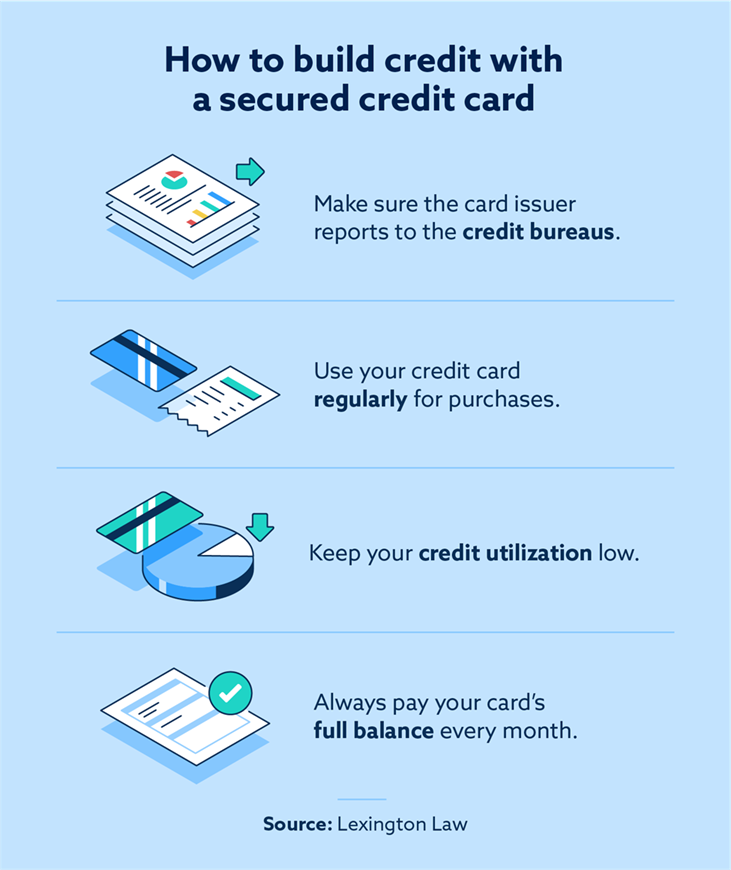

Make sure your card issuer reports to the credit bureaus

There are three major credit bureaus that keep track of your credit history, so you’ll want to be sure your credit card issuer is reporting your payments so you can build your credit. Check the credit card agreement or call the card’s issuing financial institution to check before you apply.

Use your card regularly

Your card will only impact your credit reports if you use it, so you’ll want to make regular purchases with it. However, it’s important to use your card responsibly, so aim for manageable purchases like groceries or small bills.

Keep your credit utilization low

One of the factors affecting your credit score is credit utilization, which is the ratio of total available credit to credit you’re actually using. A low ratio suggests to creditors that you are a low-risk borrower, which can improve your credit. We recommend using under 30 percent of your total available credit and paying off anything above that as quickly as possible.

Pay off your full balance every month

An important part of managing a credit card is paying off the full balance every month, which helps you avoid paying any interest or falling behind on payments. A late or missed payment can lead to a negative item on your credit reports that could hurt your credit.

Secured credit card vs. prepaid debit card

On the surface, a secured credit card may seem like the same thing as a prepaid debit card. However, there are a few key differences:

- Credit history: Debit cards do not contribute to your credit history, while credit card payments do.

- Deposit collateral vs. prepaid cash: A secured credit card does not use your deposit to pay your balance—unless the lender needs to use it as collateral for a missed payment. Prepaid debit cards draw from the deposited cash any time they are used to make payments.

Review your credit with Lexington Law Firm

Secured credit cards offer an excellent way to build credit and successfully apply for traditional cards later on. Traditional credit cards offer attractive interest rates and credit limits, and many also offer more cashback reward options.

If you’re looking to get a secured credit card to fix your credit, it helps to review your credit report before sending out applications. The team at Lexington Law Firm can help you better understand the information on your reports, and we could even help you address errors on your reports through our services.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.