The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

The 7 most common FCRA violations are withholding notices, privacy violations, requesting report for impermissible purposes, failure to follow proper debt disclosure procedures, furnishing and reporting inaccurate information, furnishing and reporting old information, and mixing files.

Key takeaways

- If a consumer reporting agency (CRA) mixes your files with another consumer’s, that counts as an FCRA violation.

- Up to $1,000 in damages can be awarded for FCRA violations.

- FCRA violations fall into two categories: willful and negligent.

In 2023, the Consumer Financial Protection Bureau received about 1,657,600 complaints from people concerning errors in their credit reports. Congress created the Fair Credit Reporting Act (FCRA) in 1970 to help consumers against unfair credit reporting practices. Discovering FCRA violations on your report can result in positive changes to your credit score.

Below, we’ll explore seven common FCRA violations in this guide and break down your credit reporting rights. After reading, you’ll know what to look out for on your credit report, and you’ll have more credit repair resources to dispute inaccuracies.

What is the Fair Credit Reporting Act (FCRA)?

The Fair Credit Reporting Act is a bill created by Congress to protect consumers’ credit information for other parties. By requiring FCRA compliance, the government reduces the likelihood that data on your credit report can hinder your attempts to find work, buy a house and pursue a better quality of life.

7 Fair Credit Reporting Act Violations explained

Here are the seven most common Fair Credit Reporting Act violations, along with tips on how to remedy these violations once they’ve been identified.

1. Withholding notices

As a consumer, you’re entitled to know how your credit information is reported, handled and used by a credit bureau. If you aren’t properly informed of how your data is being used, a violation occurs.

The following actions are considered withholding a notice:

- A creditor refuses to notify you of your right to dispute inaccurate credit information

- A creditor fails to provide you with your credit information when it’s used to make a credit decision

- Creditors don’t notify you when negative credit information (like repeated late payments) is supplied to consumer reporting agencies (CRAs)

Bottom line: An FCRA violation occurs when credit bureaus don’t communicate how your credit information is being used.

2. Privacy violations

Your information should only be shared with authorized people or entities that have demonstrated a valid need for your credit information.

Entities that typically have a justifiable reason to see your credit information include:

- Landlords, to see if you have a pattern of making payments on time

- Credit card companies and lenders, to determine if you’re a responsible borrower

- Insurers, to make sure that you are able to make responsible financial decisions

Credit bureaus are normally careful not to share your credit report with unauthorized parties. If your information is mishandled, however, you may be entitled to damages.

Bottom line: Select parties are entitled to your credit information under specific circumstances. Mishandling sensitive information is considered an FCRA violation.

3. Requesting a credit report for an impermissible purpose

A credit bureau may violate the FCRA if they supply your credit information to someone for an impermissible purpose.

Impermissible purposes would include:

- An employer who pulls your credit information without written permission

- A creditor that pulls your report to check on your current financial status for no provided reason (such as a recent application for a new credit card)

- An employer requests your credit report without your express permission

Bottom line: Entities that require your credit report without a valid reason risk violating the FCRA.

4. Failing to follow proper debt dispute procedures

The FCRA requires agencies to handle credit disputes in very specific ways. That includes conducting a reasonable investigation of your dispute, modifying and correcting any found inaccurate information, and removing the disputed item from your credit report within 30 to 45 days after receiving notice.

Sometimes, a credit bureau can neglect any or all of these responsibilities, meaning they’ve violated proper debt dispute procedures.

Bottom line: Failing to handle credit disputes in a timely and accurate fashion counts as an FCRA violation.

5. Furnishing and reporting inaccurate information

Entities like credit card companies or loan collectors should not intentionally supply incorrect information to a CRA under any circumstances.

Some examples of reporting inaccuracies include:

- Overstating or misstating total balances due

- Reporting a debt that has been paid off as a charge-off

- Reporting payments paid on time as late

- Mistakenly listing you as a debtor on an account

Bottom line: Creditors should not intentionally give inaccurate information to CRAs.

6. Furnishing and reporting outdated information

If you find the information in your credit report is not updated after a change in your credit (like an account being closed), this could be in violation of the FCRA.

Examples of this kind of FCRA violation include:

- Reporting information older than seven to 10 years old

- Failing to report debt as being discharged in bankruptcy

- Reporting old debts as current

- Reporting a closed account as being still active

Bottom line: Creditors or CRAs failing to update your credit information violates the FCRA.

7. Mixing your files with another party’s

In some instances, a credit bureau can mistakenly “mix” your file with that of another person with similar information. This violates the credit bureau’s obligation to report accurate credit information about every borrower.

Mixed file violations include combining credit information of people with similar names living in the same area, such as if there are two people named “John Smith” who live in the same zip code, or not including “Jr.,” “Sr.,” “II” or other differences for people with similar surnames.

Bottom line: Mixing credit information between two similar accounts is considered an FCRA violation.

What are your rights under the Fair Credit Reporting Act?

Every consumer in the U.S. has certain protected rights under the FCRA. Below, you’ll find a summary of what these rights include.

|

The FCRA Right to: |

Examples |

|---|---|

|

Know if information in your credit file is used against you |

Getting denied new credit based on previous late payments reported by TransUnion |

|

Ask for a credit score |

Asking for your credit score before applying for a mortgage |

|

Know what information is in your file |

Were you denied a loan based on recent credit card applications |

|

Obtain a security freeze |

Contacting credit bureuas to freeze your account |

|

Dispute inaccurate information |

Disputing a paid off card that’s still on your report |

|

An accurate, complete and verifiable credit report |

Equifax updating a report within 30 days of finding inaccuracies |

|

An up-to-date credit report |

A chapter 7 bankruptcy must be removed after 10 years |

|

Limit unsolicited offers based on your credit report |

Receiving too many offers for preascreened cards |

|

Limit access to your credit file |

Other parties can only view relevant data on your report |

|

Require consent for employers to view your reports |

Interviewers must gain consent before viewing your report |

|

Seek damages from violators |

Suing if an FCRA violation impacts you |

Suing for damages after an FCRA violation

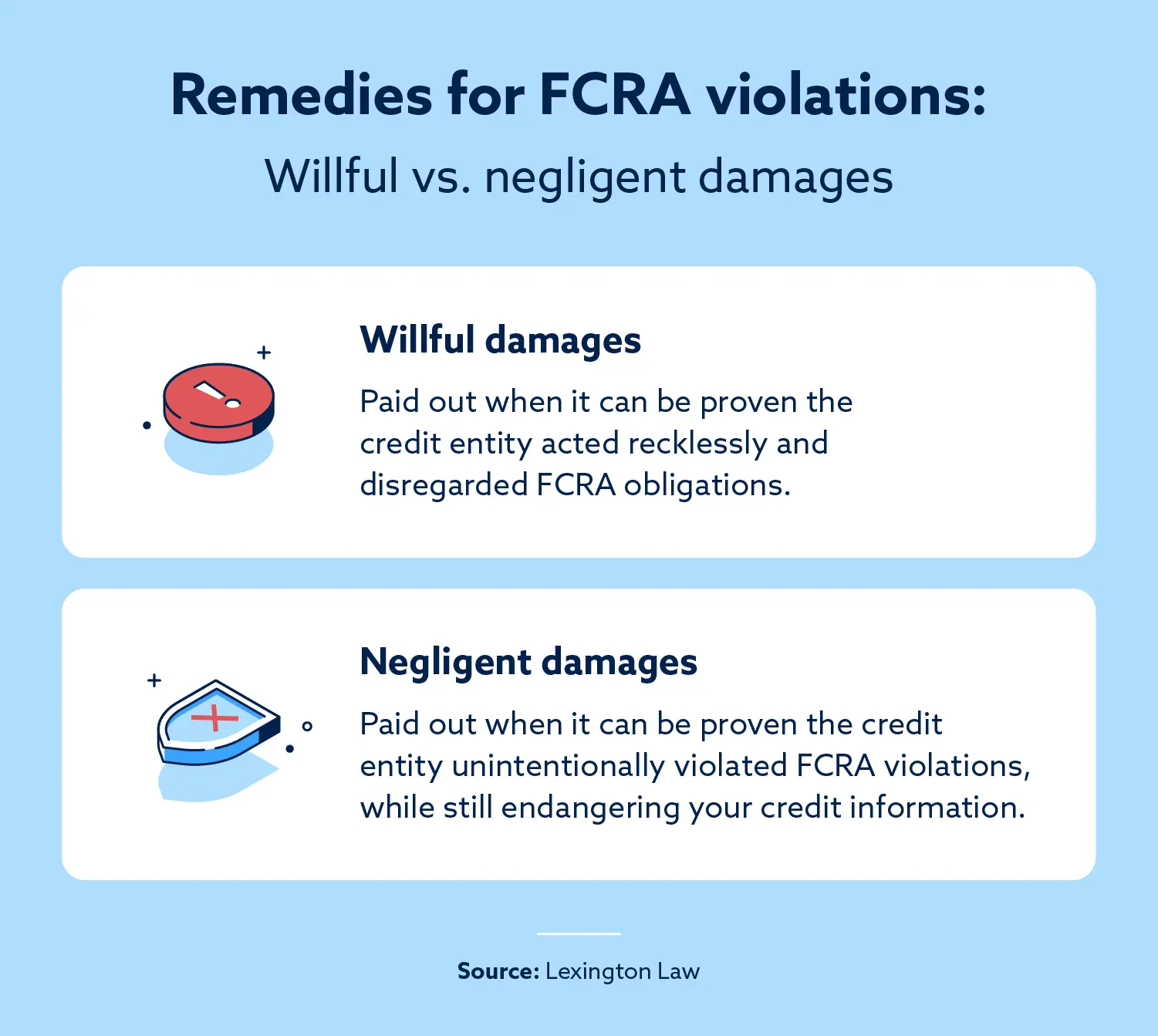

From a legal perspective, “damages” refer to reparations that a person seeks when they’ve been negatively affected by another party. If an FCRA violation by another party results in lost funds or harm to your reputation, you can seek damages in court.

Once you’ve identified that the Fair Credit Reporting Act has been violated by a CRA or another credit entity, you’re able to sue that entity in court for one of two types of damages: willful or negligent violation.

Willful violation

A willful violation means you can prove that the CRA or credit entity acted recklessly with your information and didn’t respect their obligations, both to the FCRA and your protected rights under the FCRA.

This doesn’t mean you and your attorney have to prove beyond a reasonable doubt that the entity intentionally violated your rights — just that they did so in the first place and that they should have known to not do so.

If you can prove this in court, you may be able to recover the following damages:

Basic damages:

- Provable damages with no set limit, or

- Statutory damages between $100 and $1,000

- Punitive damages as decided by the court

- Attorney fees and costs

Damages from an individual violator who lied or used your credit report for an improper purpose:

- Provable damages with no set limit, or

- $1,000 flat

- Punitive damages as decided by the court

- Attorney fees and costs

Negligent violation

A negligent violation means the CRA or credit entity violated your rights under the FCRA without knowing they did so or without meaning to.

If you’ve identified and proven negligent violations when it comes to your credit, you may be entitled to the following damages:

- Actual damages with no set limit or minimum

- Attorney fees and costs

Before you call your lawyer, you should be aware that there is a penalty for an unnecessary, or “frivolous,” FCRA lawsuit that can come with a hefty fine — you’ll need to pay the other party’s attorney fees if it’s found your suit was filed in bad faith or for purposes of harassment.

Let Lexington Law Firm Help You Dispute Credit Errors

Investigate any suspicious information on your credit report, as they might turn out to be errors incurred by FCRA violations. If that’s the case, contact Lexington Law Firm to get help disputing these inaccuracies. Learn more about our services to see how you can challenge errors more successfully.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.