Insufficient credit history means you have no proven track record with creditors that lend money or other assets. This prevents lenders from assessing your credit risk.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Insufficient credit history means you have no proven track record with creditors with regard to borrowing money or other assets. Whether you’re applying for rental property, a personal loan, a student loan, a line of credit or something similar, creditors need to know that you will likely repay your debt on time. They determine this based on your credit history, which can be found in your credit report.

Some of the parties that can access your credit report include:

- Insurance companies

- Banks and financial institutions

- Landlords and employers

- Mortgage lenders, auto loan lenders and other lenders

Unfortunately, most lenders want to see proof of good credit usage, which means you often need credit history to build credit history—a classic chicken-or-the-egg problem. It may seem impossible, but understanding how key factors contribute to your credit history can help you navigate this situation.

Below, we demystify insufficient credit history and show you how to fix it in four steps.

How credit history contributes to credit scores

Lenders generally rely on a person’s credit history and score to evaluate their creditworthiness and calculate their interest rates. Although over 90 percent of consumers begin to accumulate credit history in their mid-to-late twenties, more than 8 million adults are “credit invisible,” which means they don’t just have an insufficient credit history—they have zero credit history.

The three major credit bureaus—TransUnion®, Experian® and Equifax®—collect information about the creditworthiness of individuals from lenders and other parties. When someone applies for credit, their potential creditor can make an inquiry into their credit score. These scores can generally range from 300, which is extremely poor credit, to 850, which is exceptionally good credit.

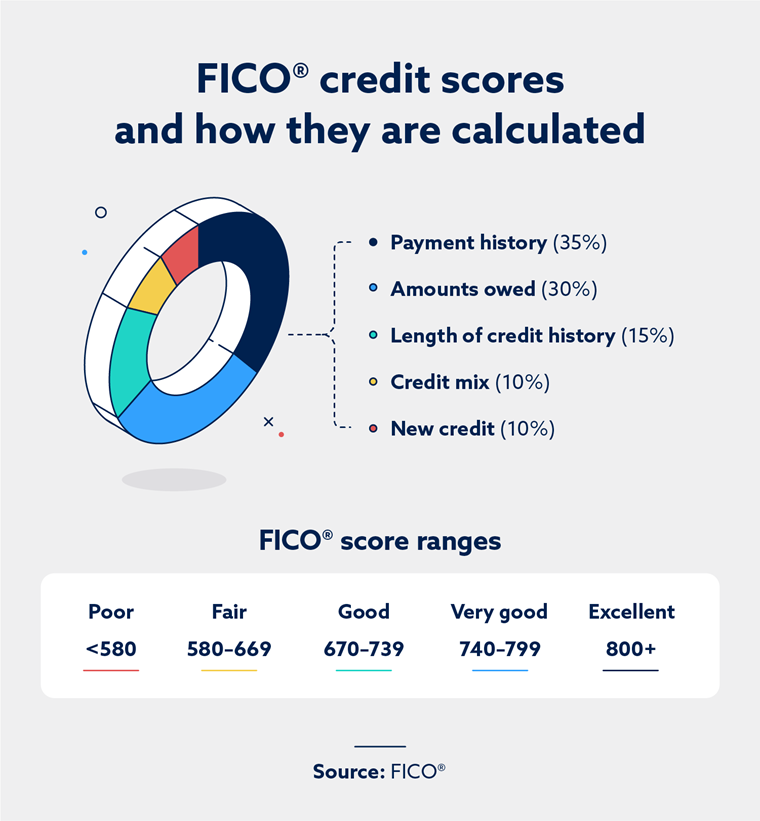

According to FICO, the algorithm for calculating a credit score contains five components that are assigned the following weights:

- 35 percent: Payment history

- 30 percent: Amounts owed

- 15 percent: Length of credit history

- 10 percent: Credit mix

- 10 percent: New credit

Looking at this breakdown, it’s clear that the most important aspect of your credit score is making regular, on-time payments for at least the minimum amount due. It’s also important to maintain a low credit utilization ratio, meaning the balances you carry on a monthly basis should be relatively low compared to your total borrowing limit.

Is one year of credit history enough?

Typically, you need six months of credit history for a credit score to be calculated and reported by the major credit bureaus. You may need to keep working beyond this point to have good enough credit to get approved at a reasonable interest rate, though.

The interest rate and payback period for a loan usually depend on your credit score, which in turn depends on the information on your credit report. For example, it’s unlikely that someone with less than one year of credit history would qualify for a 30-year mortgage.

Keep in mind that your credit score doesn’t last forever. You must continue to prove your creditworthiness by paying your debts on time and making at least the minimum payment due. This means that even with years of credit history, if you close all lines of credit and pay off all debts, you might return to an insufficient credit history status, although many items can stay on your report for up to 10 years.

No credit vs. bad credit: Which is better?

Having no credit means having limited or no credit history, which could disqualify you from credit cards or loans. However, it also means a clean slate without any negative marks or delinquencies—an opportunity to start building a positive credit history from scratch.

Bad credit is caused by missed payments, defaults or high levels of debt, which can lead to higher interest rates and unfavorable loan terms.

Building credit is possible with secured credit cards or small loans. Improving bad credit involves addressing debts and demonstrating responsible financial behavior. No credit may be beneficial for having a fresh start, but both situations require active efforts to improve creditworthiness.

How to fix insufficient credit history

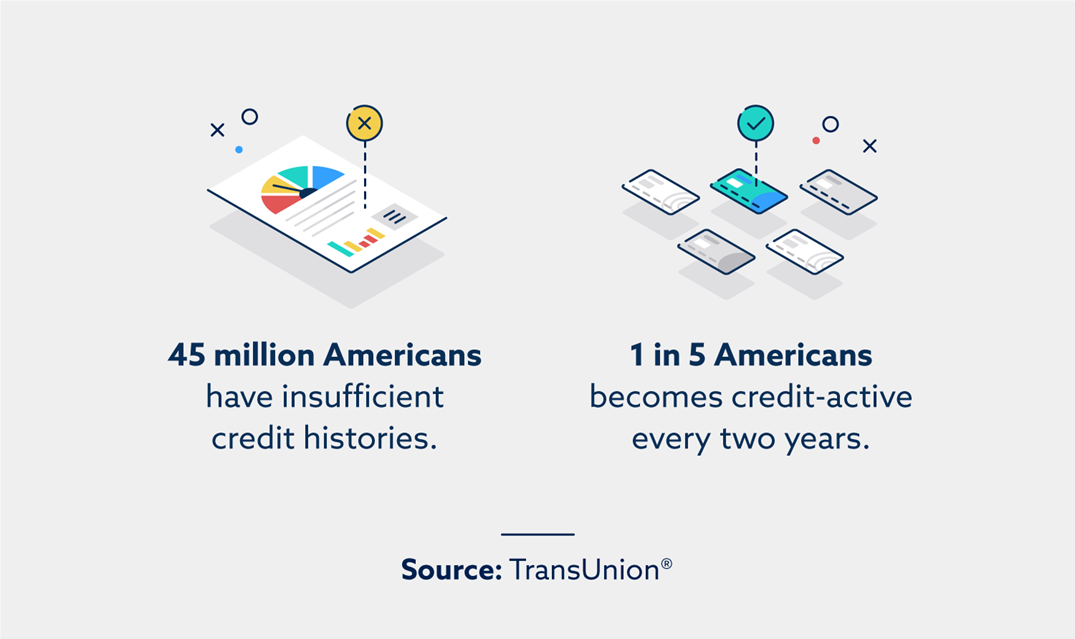

If you have an insufficient credit history, you are far from alone. TransUnion® reports that 45 million adults are essentially credit invisible, meaning they don’t have enough credit history to generate an accurate credit score. Only 20 percent of these adults become credit-active every two years.

Unfortunately, there are no quick fixes for insufficient credit history. The only way to build trust with lenders is to make consistent payments over time.

If you have insufficient credit history, it’s best to start building your credit now. A secured credit card, for example, allows you to build credit without taking any of the risk associated with borrowing money. You must maintain responsible purchasing habits and make regular payments to prove your creditworthiness.

When your credit history is insufficient, there are some strategies you can use to proactively build credit. Although there is no way to speed up the process of accumulating credit history, follow these steps to build a better history of creditworthiness.

1. Review your credit report for errors

A study by Consumer Reports discovered that 34 percent of people have had at least one error on their credit report. If you have a lower-than-anticipated credit score or none at all, review your credit report and dispute any errors with the credit bureaus. This is where a credit repair company can potentially help you.

If you’re deemed to have insufficient credit history, but you believe you have established credit, first consider whether it’s been more than six months since you last paid a debt in case your credit history has lapsed. Otherwise, confirm that all personally identifiable information (such as your legal name, Social Security number and driver’s license number) is accurate on your loan application.

If your legal name is even slightly misspelled or is missing a suffix (Jr., Sr., I, II, III, etc.), your credit report could be incorrect.

2. Get a secure credit card

If you have insufficient credit experience and, therefore, no credit history, you will find it difficult to get approved for a loan. Instead, you should consider secure credit cards as a stepping stone to getting more credit.

Secure credit cards are backed by a cash deposit instead of your promise to repay the lender (i.e., credit). Once you have made good on your promises to pay back all purchases and interest charges on your secured credit card, you can transition to an unsecured credit card. The unsecured credit card is usually when your credit history begins; six months later, you will likely have a credit score.

3. Pay your bills on time

Since between 35 percent and 40 percent of your credit score is calculated based on your payment history, you should pay your bills on time and in full. Anyone who extends credit to you expects repayment at regular intervals and for at least the minimum amount due. Late or incomplete payments may negatively affect your future credit.

4. Maintain or reduce credit utilization ratio

With 30 percent of your credit score depending on the balances you owe to lenders, maintaining a healthy credit utilization ratio is recommended. If possible, pay off balances in full every month instead of building up debt levels that become unsustainable.

As you now know, establishing credit and credit history is important, but the work doesn’t end there. It’s essential to monitor, maintain and, if needed, proactively work to improve your credit. Late payments, collections, defaults and bankruptcies can negatively impact your credit.

If you feel your credit health does not accurately reflect your credit history, Lexington Law Firm could help you address inaccurate negative items on your report. Get your free assessment today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.