The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Quick Answer: Annuities are financial products you buy, usually from insurance companies, to provide a steady stream of income over time. You pay a lump sum or make payments, and in return you receive regular payouts, often during retirement, to help cover expenses and ensure financial stability.

Most people know about 401(k)s and IRAs, but many other options for retirement planning and wealth-building are available. Annuities are a popular financial product that can be helpful in retirement, but they come with some potential downsides.

So, how do annuities work? Keep reading to learn more about annuities and understand whether this option is right for you.

What is an annuity?

Annuities are a type of insurance product, but instead of insuring yourself or your property against potential future losses, annuities let you insure income. Specifically, they help ensure you’ll receive an agreed-upon amount of money periodically at some point in the future, which makes them a popular option for retirement planning.

Annuities can be immediate or deferred, as well as fixed, variable or indexed. They’re typically sold by banks, brokers, investment companies and life insurance companies.

The basic concept behind annuities is that you purchase a product now, which you pay for upfront or by making ongoing payments – sometimes in the form of insurance premiums – over a period of years.

How are annuities paid?

Depending on the annuity product you purchase, you can receive payments for a certain period or for the rest of your life once the annuity payout begins. Those payments typically come periodically, such as monthly, quarterly or annually.

You can also choose immediate annuities that begin payouts as soon as you successfully sign up.

Generally speaking, you can safely expect to get back more in annuity payments than you pay into the product. That’s why they’re considered an investment.

This is because your annuity purchase price or payments are put into a collective fund with all other payments being made by annuity customers for that product. Those funds are invested, and the earnings over time result in a profit for you and the provider.

The main types of annuities

How much you can earn, when and how it pays out, and the risk associated with your investment all depend on what type of annuity you buy. The types of annuities are summarized below:

Deferred annuities versus immediate annuities

The first major decision to make when purchasing an annuity is whether you want a deferred or an immediate annuity.

Immediate annuities are good for people who want income right away, like retirees. You pay a lump sum, and the payouts start almost immediately, helping cover living expenses.

Deferred annuities are better for people saving for the future. You invest money now, let it grow over time, and receive payouts later, often during retirement.

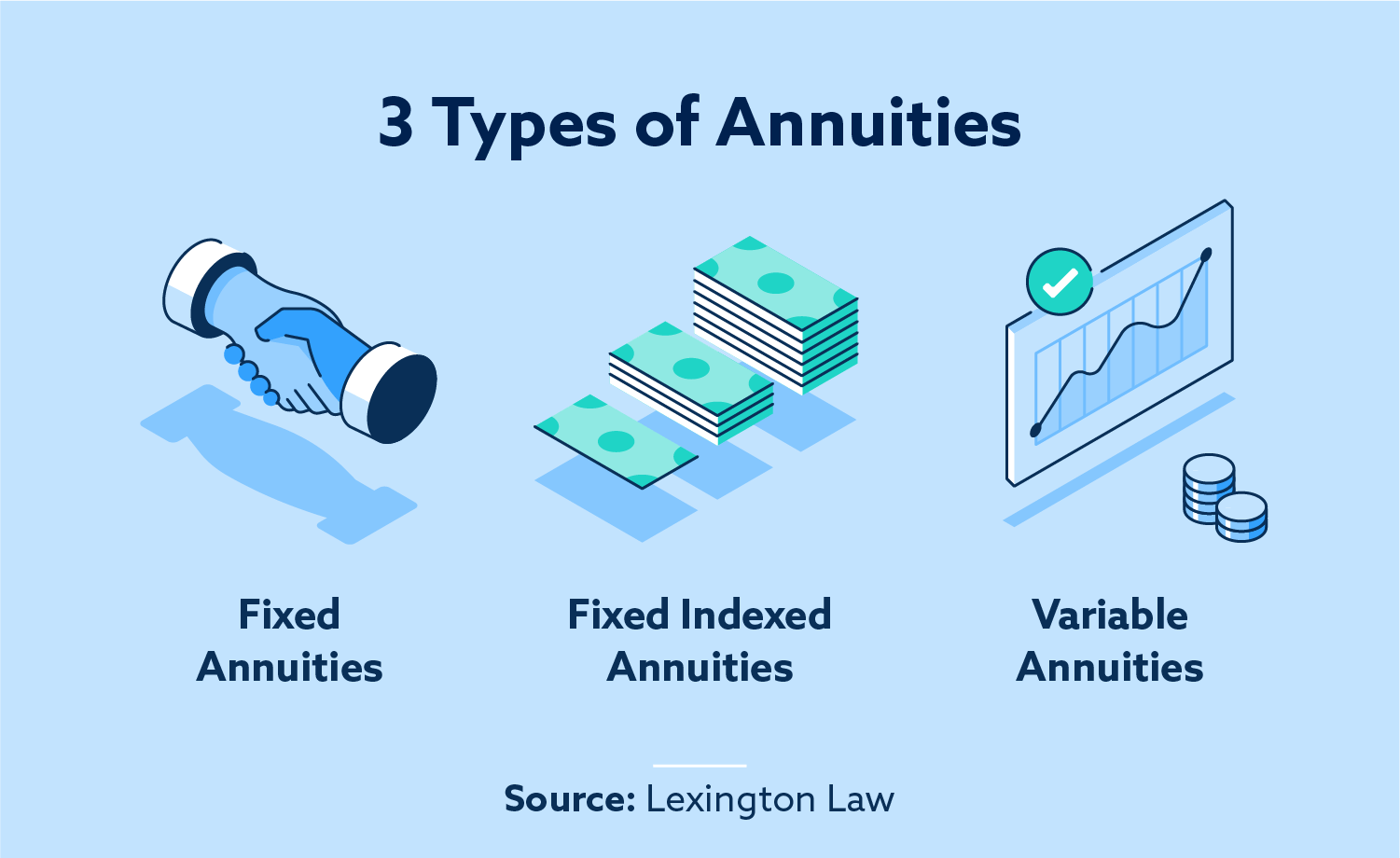

Three categories of annuities

Once you decide when you want your payouts to begin, you’ll need to pick a more specific type of annuity to invest in. Both immediate and deferred annuities have three major categories, which are outlined below.

1. Fixed annuities

Fixed annuities pay out an agreed-upon, guaranteed amount each time you receive income.

Pros:

- Guaranteed Returns: They offer a stable, predictable interest rate, making them low-risk.

- Principal Protection: Your initial investment is safe from market losses.

- Simplicity: Fixed annuities are easy to understand compared to other investment products.

Cons:

- Low Returns: Fixed annuities offer guaranteed interest rates, but the returns are often lower than other investments like stocks or mutual funds.

- Inflation Risk: Over time, inflation can reduce the value of your fixed payments.

- Fees: Some fixed annuities come with hidden fees, reducing your overall earnings.

2. Variable annuities

Variable annuities are tied to a group of mutual funds. The amount of your annuity payout depends on the performance of those funds. That can mean greater long-term reward, but it also comes with more risk than either of the other two categories of annuities.

Pros:

- Growth Potential: Your money is invested in sub-accounts (like mutual funds), offering higher returns than fixed annuities.

- Death Benefits: Many include a payout to beneficiaries if you pass away.

Cons:

- High Fees: They often come with high management fees, insurance charges, and surrender fees.

- Market Risk: Your investment can lose value if markets decline.

- Complexity: They can be difficult to understand due to their structure and options.

- Tax Penalties: Withdrawals before age 59.5 can face a 10% penalty, plus taxes.

3. Fixed indexed annuities

Fixed indexed annuities (FIAs) combine features of fixed and variable annuities. Your money earns interest based on the performance of a stock market index, like the S&P 500, but without direct investment in the market.

They offer growth potential tied to the index but also protect your principal from market losses. FIAs guarantee you won’t lose money due to market drops, though returns are often capped or limited. They’re popular for people looking for safer growth while planning for retirement.

Pros:

- Principal Protection: Your money is protected from market losses, even if the index declines.

- Growth Potential: Interest is tied to a stock market index, offering more growth than traditional fixed annuities.

- Lower Risk: Combines market-linked growth with safety, ideal for conservative investors.

Cons:

- Capped Returns: Growth is limited by caps, spreads, or participation rates, reducing your potential earnings.

- Complexity: FIAs can be difficult to understand due to their structure and rules.

- Inflation Risk: Fixed returns may not keep up with inflation over time.

- Fees: Some FIAs include fees for riders or other features, reducing your overall return.

Can you withdraw your money early?

You may be able to withdraw money from an annuity early if you find you need your investment back or can’t wait until payouts are scheduled to begin. But this can be a costly move.

First, if you take money out of a retirement account, including some annuities, before reaching retirement age, the IRS may levy a 10% penalty. You’ll also have to pay any applicable taxes on the income.

For the purposes of annuities, penalties and taxes are only paid on the amount you earned on the investment. You’re not taxed on the amount you paid into the annuity because you were already taxed on that amount when you earned it the first time.

In some unusual cases, the IRS waives the 10% penalty. Such cases include the total disability of the annuity owner or the annuity owner taking early withdrawals to pay for qualified education expenses.

What happens to annuities when the owner dies?

Understanding the terms of your annuity contract and what happens to payments after you die is essential. Ultimately, what happens to any money left in an annuity contract when an owner passes will depend on the type of annuity you purchase. Some annuities allow for leftover funds to be paid out to a beneficiary. However, other plans will stop payments once an owner dies.

You can choose which option you prefer when signing the annuity agreement.

How are annuities taxed?

Taxes on annuities can be complex, so it’s important to consult a tax professional to understand what your tax burden might be. Typically, payments you make toward an annuity aren’t made with pretax dollars. That means the money you pay into an annuity is already taxed, so you won’t pay income tax on it again in the future.

But you might owe taxes on any earnings you make from the investment. So, when you begin to receive payouts, you’ll have to report the income and calculate how much of it is taxable.

Is an annuity right for you?

Deciding whether any investment is suitable for you is an individual matter. You must look at your current financial state, your goals for the future and the level of risk you’re comfortable with.

Since annuities are based on contracts, they’re typically considered less risky than stock market investments, but no investment is completely guaranteed. Consider talking to a financial adviser to understand what investment and retirement planning options might be right for you.

The main criticism of annuities is that they’re pretty inaccessible. So in an emergency, you’ll struggle to get the money out without being heavily penalized.

Planning for the future

As you look forward to retirement and beyond, a part of having robust financial health is maintaining your credit score. You never know when you’ll need to apply for your next loan or credit card, and your credit report and score will play a large part in your approval process.

If you’re unsure where your credit stands or how to improve it, you can start now with a free credit assessment that includes your credit score, a short credit report summary and a free credit repair recommendation.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.