The United States Department of Veterans Affairs doesn’t have a minimum credit requirement for loans. However, private lenders are usually more favorable to applicants with a credit score of at least 500.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

The United States Department of Veterans Affairs (or VA for short) doesn’t have set credit requirements for loans. Yet, “What is the minimum credit score for a VA loan?” remains a common question. This is because there are private lenders who also offer VA loans—and who typically have specific credit requirements for borrowers.

Most private lenders are willing to work with applicants who have at least a 500 credit score. The higher your score, the more likely you are to obtain a loan. Here, we’ll discuss the nuances of credit scores and the military‘s requirements for VA loans. We’ll also share how Lexington Law Firm can assist you on your credit-building journey.

Key takeaways:

- The VA has a special debt relief program for veterans.

- Veterans can qualify for unique loans.

- The Servicemembers Civil Relief Act only applies to active-duty members.

The minimum credit score for a VA loan

The VA doesn’t require a minimum credit score for loans. Private lenders, however, will use your credit score to gauge your eligibility and set your interest rate. Applicants with higher credit scores tend to receive better rates, and private lenders tend to look favorably on applicants with good credit scores (670 – 739, according to the FICO® model).

That said, it’s still possible to get a loan with bad credit. Applicants with low credit scores can make a higher down payment if they have the capital to do so. Applying with a cosigner is also another valid alternative; lenders will look at the creditworthiness of both signees when deciding whether or not to approve you.

What are the VA loan eligibility requirements?

VA loans have unique qualifiers besides credit scores that applicants will need to keep in mind. Since the Department of Veterans Affairs primarily works with service members who’ve already retired, many active-duty service members may not be eligible for VA loans.

Below, we’ll break down the eligibility criteria for VA loans by category.

Credit and income Information

We know the VA doesn’t have strict limits on credit, but they do require proof of income. Applicants will also have much better odds if their debt-to-income ratio is below the 44 percent threshold.

Discharge status

So long as an applicant wasn’t dishonorably discharged from service, they are eligible for a loan. Unless a service member was deemed insane when they were charged, title 38 of the United States Code (38 U.S.C. § 5303) states that individuals are susceptible to a statutory bar to benefits if they were released or discharged for any of the following reasons:

- Was sentenced to a general court-martial

- Was a conscientious objector and refused to comply with lawful orders of competent military command

- Deserted their post

- Resignation by an officer for the good of the service

- Being absent without official leave (AWOL) for a consistent period of 180 days or more

- Requested release from service as an alien during a period of hostilities

Certificate of eligibility

You’ll need a certificate of eligibility (COE) to apply for a VA home loan. Once you gain a copy of your discharge/separation papers, you can request your COE by mail, phone, through a lender or via the VA’s online portal.

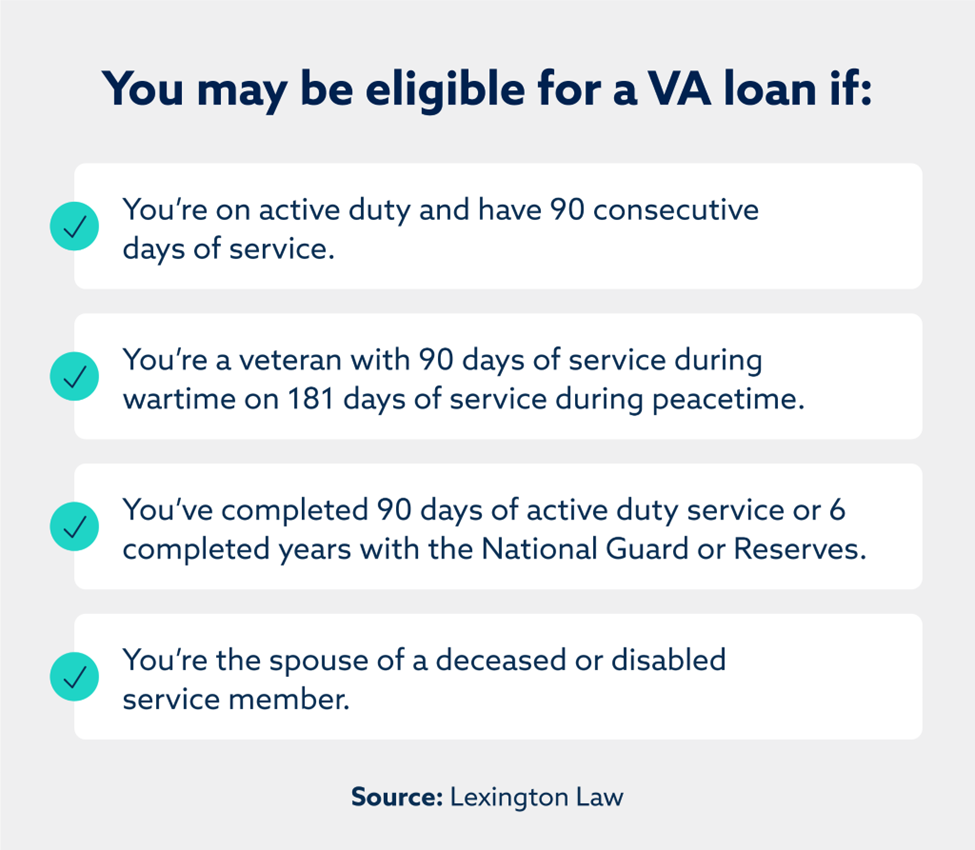

Military service status

The requirements for this category will vary depending on your relationship with the military.

- Active-duty service members: Must have 90 consecutive days of service.

- Veterans: Must have 90 days of service during wartime or 181 days of service during peacetime.

- National Guard or Reservists: Are required to have 90 days of active duty service or six completed years of service.

- Spouses: Spouses of deceased or disabled service members.

Occupancy requirements

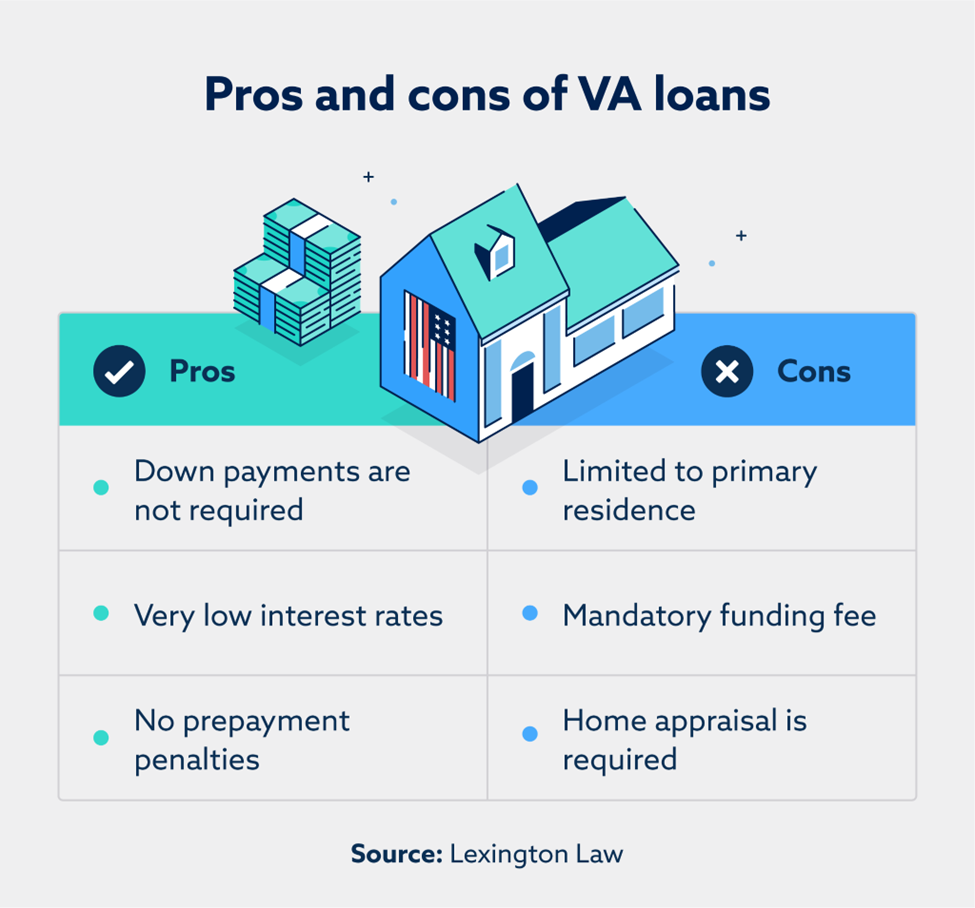

The VA has specific occupancy requirements to deter people from misusing their loans. VA loans are intended for primary residences, not investment properties or vacation homes. To that end, applicants can only secure VA for their primary residence and will need to submit proof of homeownership in most instances.

Applicants will also have 60 days after closing on a property to move in and occupy it as their primary residence. In certain circumstances (such as if an applicant is on active duty), this 60-day window will be extended.

What are the benefits of using a VA loan?

VA loans provide a host of advantages to anyone who can secure them. Several examples include:

- No down payment: If you can secure a VA loan for your home, you won’t be required to offer a down payment. Applicants who want to lower their interest rate will still have the option to place a down payment.

- Low-interest rates: Because VA loans are backed by the government, they traditionally come with some of the lowest interest rates available.

- PMI isn’t required: Once again, thanks to government backing, VA loans let applicants save money by forgoing private mortgage insurance (PMI).

3 simple ways to improve your credit

We’ve established that private lenders prefer applicants with good credit. FICO, one of the most respected credit reporting companies in the world, defines good credit scores as any that fall between 670 and 739.

If your score isn’t already in that range, here are a few strategies to help you along the way.

Regularly make your payments on time

FICO considers payment history to be the most important factor when determining what affects your credit score. VantageScore®, a credit reporting company founded by Equifax®, Experian® and TransUnion®, also holds payment history in high regard.

Missing a payment can drastically hurt your credit. On the other hand, consistently making payments on time, even if it’s just the minimum payment, will steadily yield positive results.

Maintain a low credit utilization rate

Credit utilization looks at your credit borrowing trends—your current balances compared with your total credit limit determines your credit utilization rate for a given period. FICO and VantageScore urge borrowers to keep their utilization rates below 10 percent, though 30 percent and below is the next best option.

Dispute errors on your credit report

Errors can appear on your credit report that can dramatically lower your credit. It’s possible to challenge these errors and potentially have them removed, though many people may need help handling credit disputes.

Lexington Law Firm works to help people address these errors on their reports. Plus, we can also contact the major credit reporting bureaus on your behalf.

Monitor your credit with Lexington Law Firm

Low or recovering credit scores may create a challenge in securing a VA loan. However, it’s never too late to increase your score and bolster your eligibility. Lexington Law Firm offers free credit assessments for veterans and service members whose credit may have altered during their time in the military. Sign up for your free assessment today to see where you’re at.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.