An authorized user is an individual added to a credit card by the owner of the account or primary cardholder. The authorized user, also referred to as the additional cardholder, can make purchases using the credit card, although the responsibility to make payments falls on the primary cardholder.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Building credit from scratch can be a difficult task, especially for those with limited credit knowledge. One way to get your feet wet with credit is by becoming an authorized user on someone else’s account. As an authorized user, you can leverage someone else’s positive credit habits to improve your own creditworthiness.

However, there are important factors to consider before becoming an authorized user yourself or adding an authorized user to your account. Read on to learn more.

Table of contents:

- What is an authorized user?

- Who can be an authorized user?

- Is an authorized user responsible for credit card debt?

- How does being an authorized user affect your credit?

- How to add an authorized user

- How to remove an authorized user

- Joint credit card vs. authorized user

- Authorized user FAQ

- Monitoring your credit as an authorized user

What is an authorized user?

An authorized user is a person added to someone else’s credit card account who has permission to make charges. The main user who owns the account is the primary cardholder, while an authorized user is sometimes referred to as an additional cardholder.

Who can be an authorized user?

Anyone can be an authorized user, provided they meet the card issuer’s requirements and the primary cardholder adds them to the account. Typically, the primary cardholder and authorized user have an established, trusted relationship.

Here are the most common scenarios where adding an individual to your account is beneficial.

- Parent/child: Parents may add their children as authorized users to their account to help them build credit history and give them access to the line of credit for emergencies or family expenses.

- Employer/employee: Business owners may add trusted employees as authorized users for business-related expenses.

- Couples: Couples may designate one spouse as the primary cardholder and the other spouse as the authorized user, especially when one partner has a higher credit score than the other.

Is an authorized user responsible for credit card debt?

No, being an authorized user doesn’t make you responsible for paying credit card debt. While an authorized user can make purchases, payment responsibilities fall to the primary cardholder. Authorized users have no legal responsibility to make payments.

How does being an authorized user affect your credit?

Accounts you’re an authorized user of are typically included in your credit report, which can help you build credit history. Also known as piggybacking credit, this allows you to use the primary cardholder’s positive credit habits to build your credit.

While being an authorized user can help increase your credit score, it can also have the opposite effect. If the primary cardholder falls behind on payments or maintains a high credit utilization ratio, this can negatively impact your credit.

It’s important to note that not all credit card issuers report authorized user activity to the three major credit bureaus. Consider checking with the primary cardholder’s issuer before becoming an authorized user to make sure they report to the credit bureaus.

How to add an authorized user

To add an authorized user, reach out to your credit card company online, by phone or in-person. Your credit card company will likely require the authorized user’s name, address, birth date and Social Security number to add them to the account.

Once you add someone as an authorized user, your credit card company will mail you a second card that the authorized user can use, although you can decide whether or not you give it to them. Keep in mind that you don’t need to give the authorized user a physical card for them to receive the credit-building benefits.

Here are additional tips to remember when adding an authorized user:

- Only add authorized users you trust since they will have access to your credit line.

- If your credit card company offers this option, consider setting up spending limits for authorized users to prevent overspending.

- Set up alerts to notify you when an authorized user makes a purchase.

How to remove an authorized user

You can easily remove an authorized user if your circumstances have changed. Similarly to adding an authorized user, just contact your credit card company and request the authorized user be removed from the account. Consider also contacting the authorized user to notify them that you’re removing them from the account.

Here are some circumstances in which you may want to remove an authorized user from your account:

- There’s been a change in relationship: For example, if your partner is an authorized user on your account and you break up

- The account has been misused: If an authorized user is overspending on your account and negatively affecting your finances. For example, if your teen’s spending habits are out of control

There are also scenarios in which you may want to remove yourself as an authorized user from someone else’s account, such as:

- You achieved financial independence: If you’ve established a credit history and no longer need access to the account, consider removing yourself to manage your finances independently.

- The primary cardholder’s poor credit habits are affecting your credit score: If the primary cardholder is falling behind on payments, your credit could also take a hit, so it’s best to cut ties.

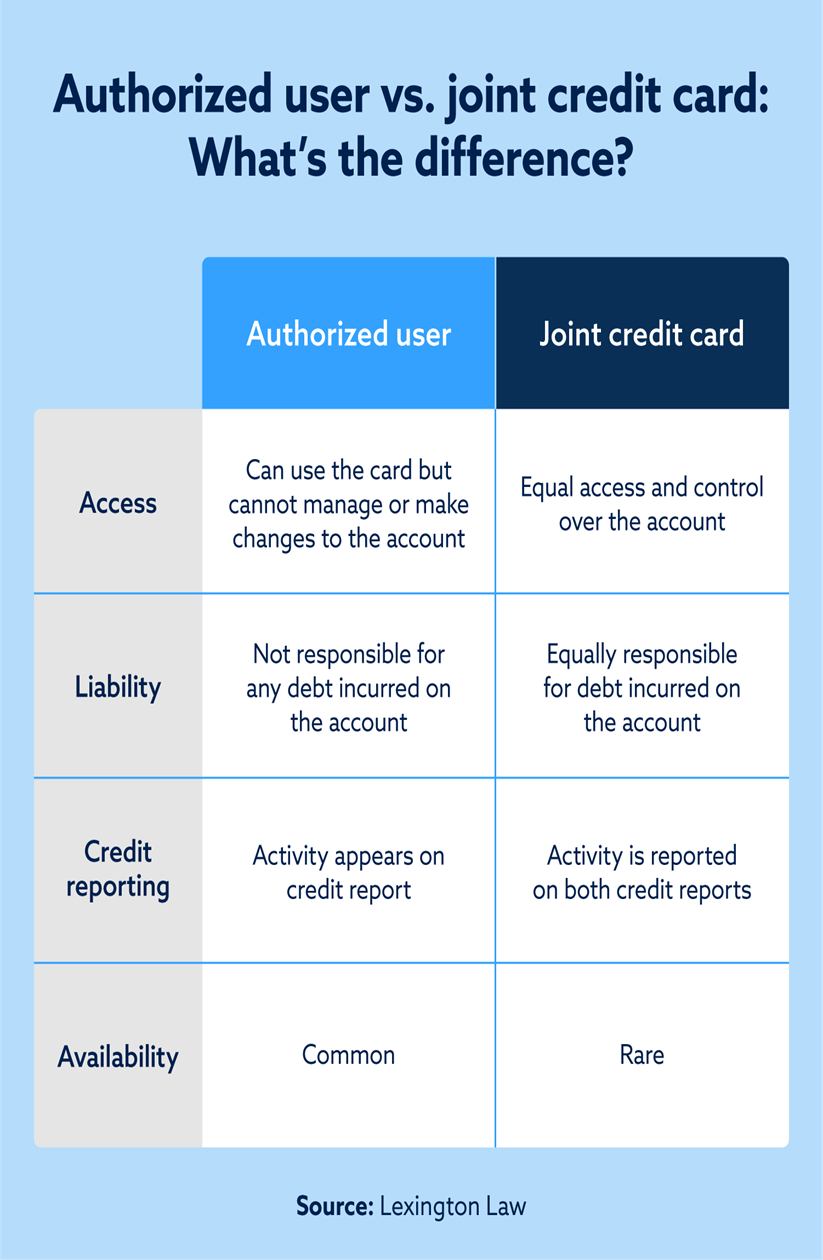

Joint credit card vs. authorized user

A joint credit card allows two people to share one account equally. The main difference between an authorized user and a joint credit card is who is legally obligated to make payments. While both parties are responsible for paying debt on a joint card, an authorized user isn’t required to make payments.

Keep in mind that fewer credit card issuers are offering joint accounts since companies prefer that only one individual is liable for the account. Meanwhile, most credit card issuers offer the option to add authorized users.

Authorized user FAQ

Still unsure whether becoming an authorized user is right for you? We’ve answered some common questions below.

How old do you have to be to be an authorized user on a credit card?

Some credit card issuers have age requirements ranging from 13 to 16, while others have no minimum age requirement.

How long does it take for authorized user accounts to show on your credit report?

Authorized user accounts will typically appear on your credit report within 30 to 45 days after you’re added to the account, as long as your credit card issuer reports to the credit bureaus.

What is the difference between having a cosigner and becoming an authorized user?

A cosigner shares responsibility for repaying the debt, while an authorized user isn’t legally obligated to make payments.

Monitoring your credit as an authorized user

Becoming an authorized user is a great way to kick-start your credit journey. As you start to build credit, it’s important to monitor your credit and ensure that no inaccurate negative items are impacting your score.

When you sign up for a free credit assessment with Lexington Law Firm, you’ll receive your credit score, credit report summary and a credit repair recommendation. View your credit snapshot today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.