The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

There are pros and cons to using either cash or credit, so you’ll have to decide which option works best for your purchases.

The experts can be quite split on whether you should be paying for your purchases with cash or credit. The simple answer is that the cash vs. credit debate is complicated—there are pros and cons to using either one. The right choice depends on each individual’s circumstances and preferences. If you need help deciding whether cash or credit is right for you, keep reading for a complete breakdown of the positives and negatives of each choice.

Should you use cash?

While it may feel like no one carries around cash anymore, that isn’t necessarily the case. Instead, people who still prefer to make purchases with cash often do so with their debit cards. A debit card is like using cash because you can only spend the money available in your account, and the money is removed immediately. Therefore, you can’t spend more than you have—just like with cash.

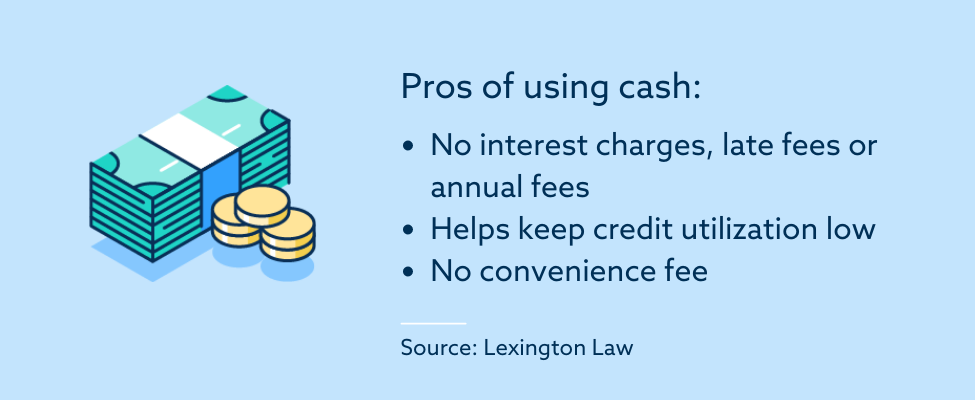

Pros

So, what are the benefits of choosing cash in a world of credit cards with points, cashback rewards and perks? Here are some of the benefits of paying with cash:

- No interest charges, late fees or annual fees: You save money in two ways with cash. First, you typically have to pay an annual fee to get a card with the best perks. Second, cash ensures you can only spend what you have, so you never pay interest or late fees on your purchases. In comparison, the average credit card interest rates typically range from 18 to 26 percent.

- Helps keep credit utilization low: Your credit utilization ratio is the amount of credit you use every month versus the amount of credit you have available to you. To prevent your credit utilization from negatively impacting your credit, you ideally want to keep it below 30 percent. That means that even if you have credit cards, it can be good to make more purchases in cash so it looks like you don’t need to access very much of the credit available to you.

- No convenience fee: Some merchants charge a convenience fee when you pay by credit card. Credit card companies charge a percentage of every transaction to the merchant, which can quickly add up. Some merchants discourage customers from paying via credit card by charging them a convenience fee. In these situations, it’s cheaper to pay with cash.

Cons

And here are some of the drawbacks of paying with cash:

- Doesn’t help build credit: Unfortunately, paying for everything with cash can leave you with a thin or nonexistent credit report. A large portion of your credit report and score is your payment history, which for many people comes from credit cards. Since your credit health can impact many aspects of your life, this can cause a significant problem.

- No long-term benefits like cash back and rewards: Of course, using cash doesn’t come with the incentives that many credit cards have, like cash back, travel rewards, gift cards, discounts and so on.

- Harder to maintain records of purchases: Unless you keep detailed records and always take receipts for your cash purchases, it will be harder to sort and record your purchases for budgeting, taxes, work chargebacks and more.

Should you use credit?

So, if cash doesn’t seem like the right choice, should you be using credit? Just like cash, using credit comes with positives as well drawbacks that you should consider.

Pros

- Building credit: Credit cards are a great way to build credit. And strong credit can help you in the future with mortgages, auto loans, rental leases and even some employment opportunities. Additionally, responsible credit card use can help you rebuild your credit score if you have bad credit. Of course, your credit can also be damaged by your credit card usage (if you have any missed or late payments), so you should be careful with your credit.

- Cash back and rewards: If you can use your credit card responsibly, it can actually end up making you a profit. You can earn cash back or rewards on travel or gift cards, which can save you money.

- Identity theft protection: Credit cards can help alert you to identity theft early by flagging suspicious purchases made with your card. Under the Fair Credit Billing Act (FCBA), victims of identity theft have certain rights, and businesses must follow protocol to help consumers get their money back. If cash or your debit card is stolen from you, it can be harder to get refunds for fraudulent purchases.

- Purchase protection: Some cards come with purchase protection that covers if items purchased on the card have been damaged or stolen. Additionally, credit cards can offer things like travel insurance, auto insurance and extended warranties (depending on the card).

- No foreign transaction fees: As opposed to debit cards, you can sign up for a credit card with no foreign transaction fees (note that this doesn’t apply to all credit cards). If you travel a lot, these cards can save you a lot of money in foreign transaction fees.

Cons

- Possible damage to credit score: There’s the potential you’ll hurt your credit if you don’t use your lines of credit properly. A single missed or late payment can drop your credit score by several points and stay on your credit report for many years.

- Remembering payments: Each credit card comes with a specific monthly payment deadline. You’ll have to remember this date to ensure you don’t accidentally miss a payment. However, you can eliminate this step by signing up for autopay.

- Potential for interest charges: Credit card and line of credit interest rates can range from 18 to 26 percent. If you’re not paying off your balance in full every month, you could end up spending hundreds or thousands more on interest.

Other factors to consider for cash vs. credit

Some other important factors to consider in your cash vs. credit decision are:

- What method is accepted by the vendor you want to purchase from? For example, a car dealer often won’t let you buy a car on a credit card but will gladly accept a bank draft (i.e., cash). Other vendors only accept cards, no cash.

- What method makes you more likely to overspend? For many people, the easy tap of a credit card can make them more susceptible to going into debt. In this case, cash or a prepaid credit card may be the safer choice.

- Do you need to build credit? Credit can be a very useful tool in your financial tool belt. If you can act responsibly and pay your bills on time and in full every month, having credit accounts will only help build your credit profile. If you know you’re going to need a car loan or mortgage sometime soon, getting a credit account now to work on improving your credit can be very helpful for those future applications.

Tips for using credit responsibly

Remember, there are advantages and disadvantages to both cash and credit. Ultimately, each person has to consider their priorities and preferences to understand what best fits their situation.

As we’ve outlined, credit can come with many benefits for the responsible consumer. So, if you’re leaning toward using credit, remember to keep these tips in mind:

- Don’t spend more than you can afford.

- Pay off your balance every month to avoid interest charges, late fees and a negative impact on your credit score.

- Set up autopay so you never miss a payment.

- Consider when credit is the best choice for payment. If there will be a convenience fee, pay for that purchase with cash.

- Keep credit utilization below 30 percent.

Remember that even if you prefer cash, you should always keep an eye on your credit reports. Your credit score opens the door to many financial opportunities, so you must do all you can to keep it healthy. The credit consultants at Lexington Law Firm can evaluate your credit report and suggest a credit repair plan for you. Get started today—your future self will thank you.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.