The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

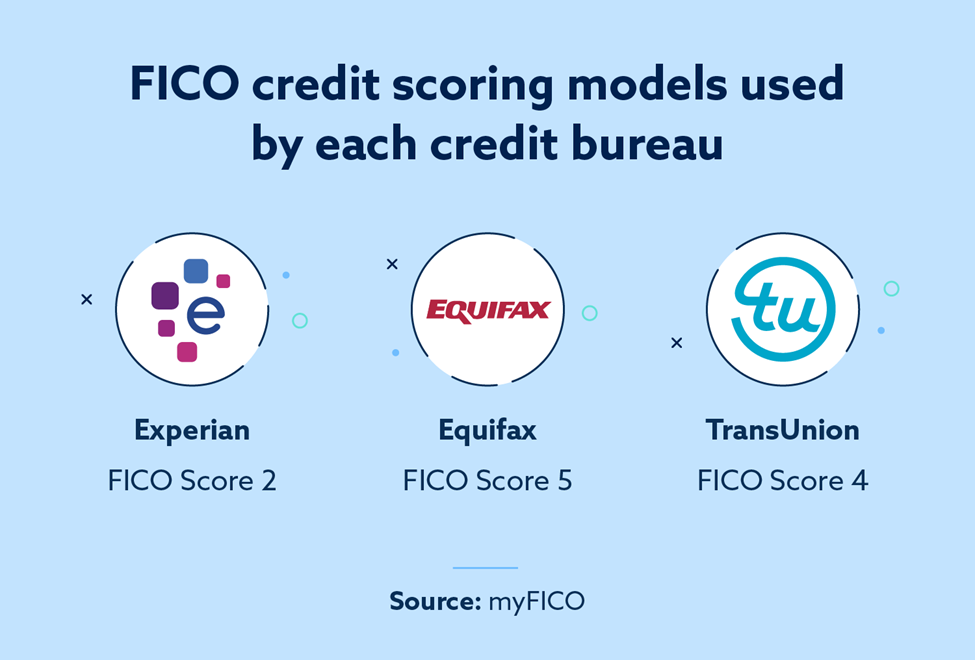

FICO Score 2, 5 and 4 are the scoring models used by Experian, Equifax and TransUnion, respectively, for mortgage lending calculations.

Your credit score is used to determine your creditworthiness across many industries, and there are several different types of credit scores a lender may use. What a credit card issuer looks for may be different from what a home lender looks for, so each scoring model is intended to cater to different needs.

Knowing what FICO® Score mortgage lenders use can help you prepare for your home loan application. Below, we’ll go into more detail on the FICO scoring model, how it’s used and how you can improve your score to qualify for a better home loan.

Which credit score is used for mortgage applications?

Experian®, Equifax® and TransUnion® each use a type of FICO scoring model for assessing mortgage applications—versions 2, 5 and 4, respectively. The primary difference between these three models is which bureau they pull data from (for example, FICO Score 2 is based on data from Experian, FICO Score 5 is based on data from Equifax, etc.). Aside from that, they use very similar metrics for determining your creditworthiness.

Mortgage companies often pull scores from all three bureaus and use the middle score to make a decision about your mortgage application. That means that checking your credit score from one bureau may not be enough to see the full scope of your standing—to do that, you’ll want to check your credit score with all three bureaus.

FICO 8 vs. mortgage score

Though FICO 8 is the most popular scoring model, it isn’t currently used for home lending. The scores used for mortgages are FICO 2, 4 and 5. FICO 8 is what’s referred to as a base score, which means it’s used to determine whether an applicant is generally likely to repay their debt on time and in full. Version 8 is also a more recent update to FICO’s scoring model than the versions used for home lending.

What credit score is needed to buy a house?

The minimum credit score needed to buy a house could be as low as 580, but could be as high as 640. FHA and VA loans, for example, require a minimum score of 580 to qualify, while a USDA loan requires a minimum of 640.

How does your credit score affect your mortgage application?

Your credit score affects whether you will be approved for a mortgage and the interest rate you’ll pay on the loan you receive. If your score is below the minimum requirements for a given loan type, you may not qualify for that loan. But if you do qualify for a loan, a higher credit score may qualify you for a better interest rate.

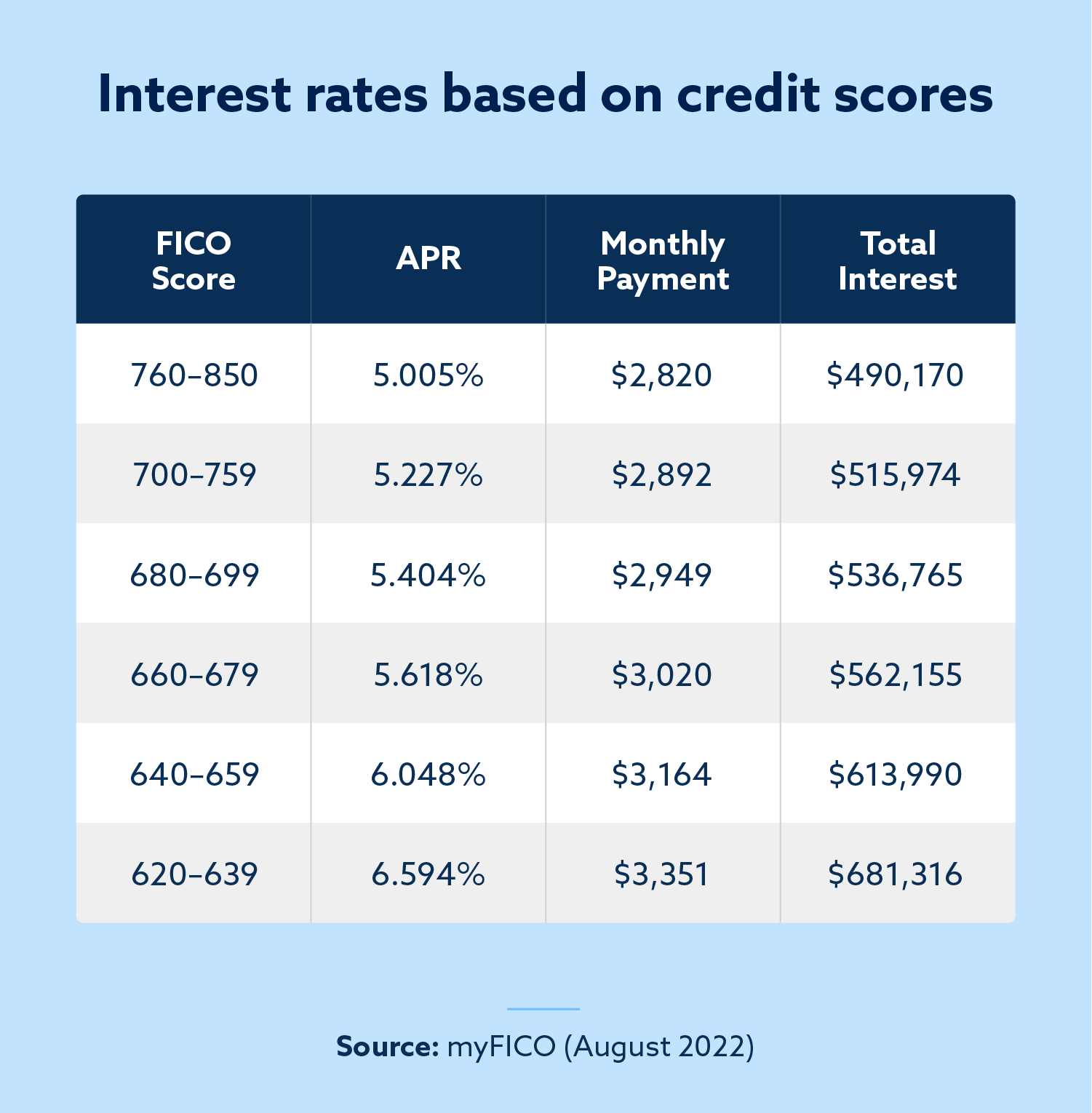

Interest rates based on credit scores

So, just how much does your credit score influence your interest rate? Over the course of a 30-year loan, even a fraction of a percentage point in interest can add up to tens of thousands of dollars. Here’s a sample calculation based on the most recent average home price numbers.

What other factors affect your mortgage terms?

So we know that your credit score helps determine your interest rate, but what else do mortgage lenders look at to determine your mortgage terms? According to the Consumer Financial Protection Bureau, they also consider your:

- Overall credit report

- Past credit history with the lender

- Total existing debt

- Savings accounts

- Existing financial assets

- Reported income

All these factors combine to provide a holistic view of your creditworthiness. If you’re deemed a higher risk for a loan, you may receive a higher interest rate, costing you more money over the course of your loan.

How to improve your credit score to apply for a mortgage

Whether you want to reach the minimum credit score that first-time home buyers need to qualify for a loan (580+) or you simply want to qualify for a better mortgage rate, you’ll want to maximize your score.

If you’re preparing to apply for a mortgage, here are a few steps you can take to work toward improving your credit score first.

Step 1: Check your score

You can check your FICO Score through your credit card company, your bank or a free credit reporting service. Checking your score is generally free and doesn’t hurt your score, so don’t hesitate to take a look.

Since mortgage loans don’t have their own industry score, your FICO Score will fall within the base range of 300 – 850. It’s worth noting that industry-specific scores like FICO Auto Score expand to 250 – 900.

Step 2: Check your credit report

Your credit report can be requested for free once per year from each of the three major credit bureaus (or once per week, through December 2022). Then, read your report and make sure there is no inaccurate information, such as:

- Misspellings or inaccurate personal information

- Closed accounts showing up as open (or vice versa)

- Accounts you don’t recognize

If you do find inaccurate information, you can dispute them, which could improve your score if successful. Or, hire a credit repair company to identify and dispute reporting errors for you.

Step 3: Include rent on your credit report

If you use a dedicated third-party app or website to process rent payments, check their website or contact customer service to see if they report payments to any of the credit bureaus. If you pay directly to a landlord or rental agency, check with them to see if they report payments.

If not, you can ask your landlord or rental agency to consider reporting or adopting one of these services. You can also sign up for third-party rent reporting services that will do it for you.

Step 4: Continue making on-time payments

As you prepare for your mortgage application, remember to continue making regular payments and, if possible, paying off any credit cards in full each month. Over time this may improve your score.

Step 5: Lower your credit utilization if possible

Your credit utilization refers to the percentage of your available credit that you use each month. FICO suggests keeping your utilization rate under 30 percent, but the lower the better.. This means that if your credit lines amount to $1,000, try to carry no more than a $300 balance each month.

Credit repair for mortgage loan applications

Knowing what FICO Score mortgage lenders use could help you take control of your credit. This could save you thousands of dollars a year on interest—or mean the difference between qualifying for a loan and being denied.

If you’re not sure where you stand with your credit, a free credit snapshot is a great place to start. Once you have a good idea of your overall creditworthiness, the credit consultants at Lexington Law Firm can help you work toward improving your credit.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.