The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Credit hacks like challenging errors on your credit, lowering credit use, increasing available credit, and becoming an authorized user may help increase your credit score.

Preparing for a mortgage application, looking to upgrade your credit card or simply wanting to improve your credit ASAP? While creditworthiness is a long-term investment and your score will need to be cultivated over time, these credit hacks may help you improve or repair your credit relatively fast. However, there are no guarantees when it comes to credit, so know that results will vary based on the specifics of your situation.

Below, we’ll break down our top 12 credit tactics into three broad categories: credit score hacks for quick gains, credit repair hacks for efficiently rebuilding damaged credit, and credit card hacks to help you improve your standing by effectively managing credit card debt.

Top 12 credit hacks

- Challenge inaccuracies on your credit report

- Consider paying off installment loans

- Lower your credit usage

- Increase your available credit

- Write a goodwill letter

- Become an authorized user

- Open a secured credit card

- Apply for a credit builder loan

- Work with a credit repair company

- Consolidate debt from multiple credit cards

- Use the snowball method to pay off credit cards

- Use the avalanche method to pay off credit cards

Credit score hacks

Determined by factors including debt repayment history, overall credit utilization, and the age of your credit lines, your credit score can affect many vital aspects of your financial life. Everything from credit card interest rates to whether you qualify for an apartment could depend on that number.

If you could use a credit boost for any reason, these actions could help you get a higher score in a short period of time.

1. Challenge inaccuracies on your credit report

In some cases, your credit score may be lower than it should be due to a reporting error. Here’s how to identify and remove inaccuracies like mistaken late payments from your report:

- Step 1: Request a copy of your credit reports from AnnualCreditReport.com.

- Step 2: Read your credit report carefully, specifically looking for any errors in personal information, listed accounts, late payments, or duplicates.

- Step 3: If you discover anything you believe is inaccurate, write a dispute letter (with return service requested) to the bureau’s address explaining the inaccuracy.

- Step 4: Wait 30 to 45 days for a response.

2. Consider paying off installment loans

Installment loans like mortgages, student loans, or personal loans are essentially lump-sum amounts that you borrow and then repay over time. Paying these off may have a positive impact on your credit score in some situations.

Loans and credit lines factor into your debt-to-income ratio (DTI), or the percentage of your income that goes toward repaying debts every month. Although your DTI doesn’t factor into your credit score, it does matter for many housing situations, as lenders prefer to see this number stay lower than 36 to 43 percent for homeowners and below 15 to 20 percent for renters.

If your DTI ratio is above that range and you have installment loans, you may want to consider paying off one or more to bring the ratio down. This could be especially helpful if you have one or more loans with a high interest rate.

3. Lower your credit usage

One of the most important credit scoring factors is how much of your available credit you use. It’s recommended to keep this ratio below 30 percent. Cutting a high credit utilization ratio to below that threshold could give you a relatively quick credit boost compared to longer-term strategies.

Let’s say you have one credit card with a $500 limit and charge $200 every month on it. In this example, your utilization rate is 40 percent. To keep your utilization rate below 30 percent, you’ll want to cut your charges to less than $150 per month.

4. Increase your available credit

If it’s not feasible to lower your credit usage, you may want to consider increasing your available credit. In the example above, if you add a second credit card with a $500 limit on top of your current $500-limit card, you would double your total available credit to $1,000. The same $200 charge each month would drop from 40 percent to 20 percent of your available credit.

Be aware, however, that applying for a new credit card comes with a hard inquiry, which will temporarily hurt your credit score. Also consider that you may be tempted to use more credit if it’s available, so this option may only be effective if it doesn’t otherwise affect your spending habits.

5. Write a goodwill letter

If a late or missed payment is dragging down your credit, a goodwill letter could get the negative mark removed from your credit report. This letter is essentially a request to a specific lender to have that item struck from your report based on an otherwise strong payment history.

Lenders are by no means required to follow through on these requests—hence the name. But since this tactic is free and carries virtually no negative consequences, it’s worth a shot. If you choose to try this, your letter should include:

- Your account number

- A description and the date of the negative mark

- Details about your history with the lender

- An explanation of why this was a one-off event that hasn’t happened since and won’t happen again

- A specific request to have the item removed from your credit report for all three bureaus

Credit repair hacks

Whether you’re working to correct past late payments, get out of a cycle of debt or fix past financial mistakes, credit repair can take time. But if you need to know how to quickly build credit after it’s been damaged, these four tactics may be able to help you restore your standing as soon as possible.

6. Become an authorized user

By becoming an authorized user on someone else’s account, you can benefit from their on-time payments. An authorized user is essentially a secondary person who is authorized to use a credit line without being responsible for repaying it. This allows that authorized user to potentially improve their credit without making other significant changes to their own spending or accounts.

However, this does come with risk for the account holder and has some limitations on who is eligible. If the authorized user racks up debt the account holder can’t afford to pay off, this could backfire. Due to this liability, this is only a good option if you have someone in your life who shares an immense amount of mutual trust with you, such as a family member or significant other.

7. Open a secured credit card

Secured credit cards can be great credit-building options for those who have trouble qualifying for standard credit cards. These cards require an up-front deposit, which typically becomes the card’s credit limit.

By making on-time payments, you may be able to build your credit up enough to qualify for a standard credit card with a higher limit, which would also increase your total available credit and potentially lower your credit utilization rate.

8. Apply for a credit builder loan

Designed to help people with low or no credit improve their scores, credit builder loans work like regular loans—but in reverse. Rather than getting money up front that you pay back over time, you pay into a savings account for a set period of time and then receive the loan amount afterward.

Here are some tips for taking advantage of a credit builder loan:

- Ensure you can afford to dedicate enough funds every month to building up the full loan amount.

- Consider getting a smaller loan amount than you may need to keep your monthly payments manageable.

- Make each payment on time to help improve your credit.

- Have a plan for the funds you receive from the loan, such as paying off other debts, contributing to a savings account, or making a down payment.

9. Work with a credit repair company

For some people, fixing credit may be best left to professionals. Credit repair companies are capable of reviewing credit reports, sending challenges, sending requests, and making individualized long-term credit plans. For a monthly fee, their teams can help you address issues on your credit report to ensure the information on your report is fair, accurate, and substantiated.

Credit card hacks

Navigating credit cards can be tricky. If you aren’t careful, high interest rates and long repayment terms can lead to a cycle of debt that can be hard to escape—and even harder to recover from. These credit card hacks could improve your credit score by helping you gain control of your debts, manage your repayments or pay off your balances efficiently.

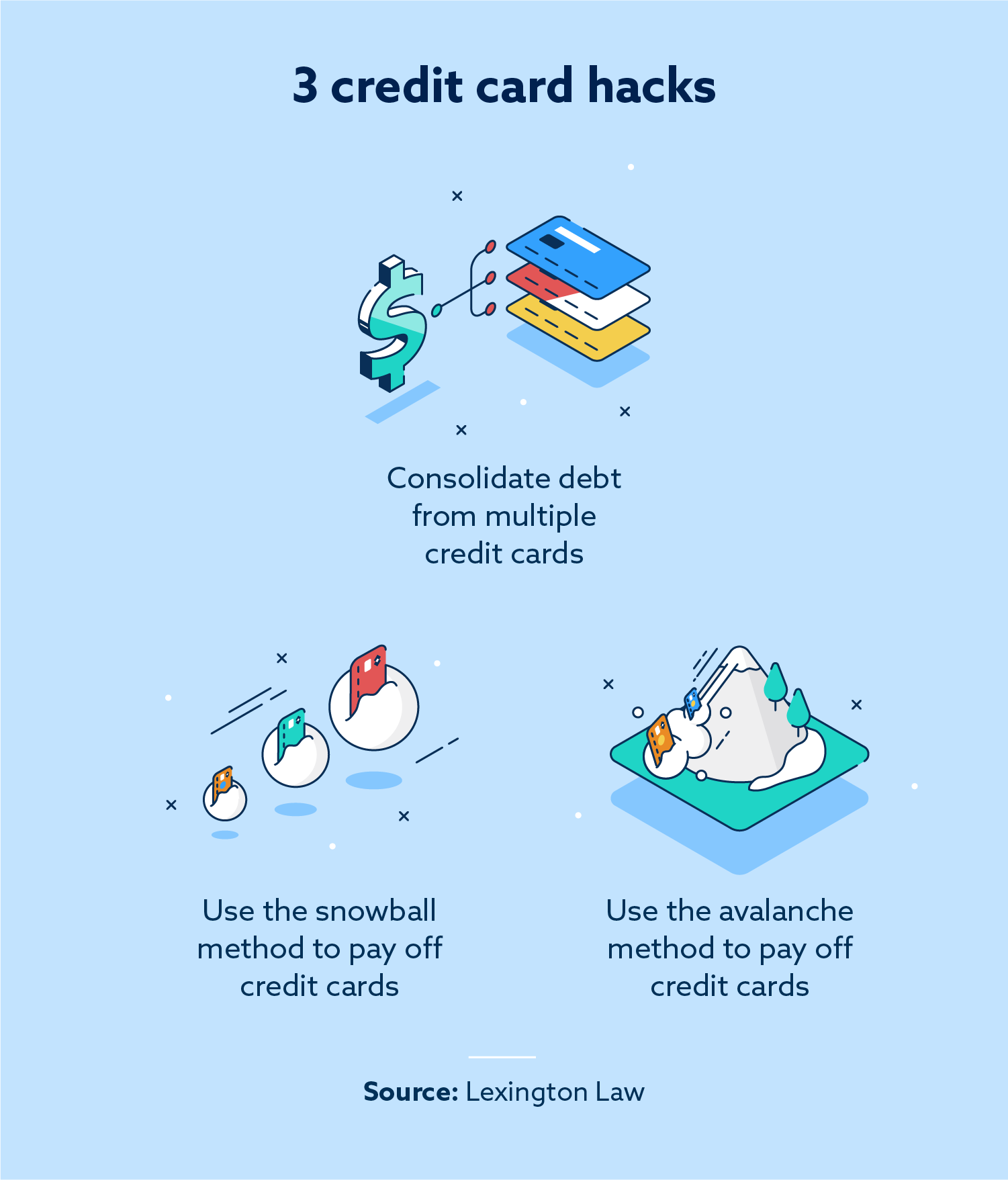

10. Consolidate debt from multiple credit cards

If you’re having trouble managing repayments for multiple credit cards with balances that carry over from month to month, consider consolidating them with a personal loan or balance transfer.

Consolidating credit card debt with a personal loan

With typically high interest rates, credit cards come with expensive debt when their balances are repaid gradually. If you’re balancing debt from multiple credit cards but you have relatively strong credit, consider applying for a debt consolidation loan from a bank.

The personal loan you choose should be big enough to pay off all or most of your current credit card balances at once. The resulting loan should have considerably lower interest rates and offer the added benefit of reducing multiple monthly due dates to just one.

Consolidating credit card debt with a balance transfer

A balance transfer is basically a way to move debt from one account to another. This is particularly beneficial if you’re able to transfer a balance from a high-interest credit card to one featuring a promotional period with low or no interest. This window of time gives you an opportunity to pay off the debt from one credit card gradually without incurring interest charges.

11. Use the snowball method to pay off credit cards

For this approach to managing debt across multiple credit cards, you’ll focus on paying off the card with the lowest balance first. This strategy allows you to take an organized approach to debt reduction over time. Here’s what that process looks like.

- Step 1: Set a monthly budget for the amount of money you can afford to allocate to credit card debt.

- Step 2: Make only the minimum payments on every card except the one with the lowest balance.

- Step 3: Spend the rest of your monthly credit card budget on paying down the card with the lowest total balance.

- Step 4: Once you’ve paid that card’s balance in full, repeat the process for the card with the next-highest balance.

12. Use the avalanche method to pay off credit cards

Another way to manage multiple credit card payments is to target the card with the highest interest rate. The benefit of this approach is that it saves you money in the long term by reducing the amount of money you have to put toward interest payments. The process is otherwise the same as the snowball method.

- Step 1: Decide on a budget for paying off credit card debt each month.

- Step 2: Each month, pay the minimum amount due on every credit card except for the one with the highest interest rate.

- Step 3: Dedicate your remaining credit card budget to over-paying the minimum on the card with the highest interest rate.

- Step 4: When you’ve paid this card off, do the same for the card with the next-highest interest rate.

Can credit hacking help you reach your credit goals?

At the end of the day, there’s no substitute for executing a long-term credit plan and sticking to it.

There’s no shortcut to consistently using credit responsibly, managing your credit utilization ratio, and making on-time payments. However, these credit hacks could set you on your way toward repairing your credit quickly or growing your credit score sustainably. In the meantime, you may want to see if using a credit repair service may be beneficial for your unique situation. You can get a free credit snapshot today to see where you stand and how credit repair can help you work to reach your credit goals.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.