A credit limit is the maximum amount of money a person can currently borrow from a financial institution.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Credit cards and lines of credit let us borrow funds from banks, credit unions and various companies. Credit limits determine just how much money we can borrow without incurring penalties like overdraft fees. Americans tend to gradually increase their credit limits as they age; Experian® reported that the average credit card limit for Generation Z in 2022 was $11,290, while the average credit limit for Baby Boomers was $40,318 that same year.

“What is a credit limit?” may be such a common question because multiple factors can influence a person’s limit. We’ll explore this question and discuss how to increase your credit limit.

Key takeaways:

- Financial institutions largely set credit limits based on a borrower’s credit history.

- Credit utilization is based on your credit limit and your available credit.

- Regularly practicing good credit habits can increase your limit

Table of contents:

- How are credit card limits determined?

- Credit limit vs. available credit

- How does your credit limit affect your credit score?

- What happens if you go over your credit limit?

- How to increase your credit limit

- Work on your credit with Lexington Law Firm

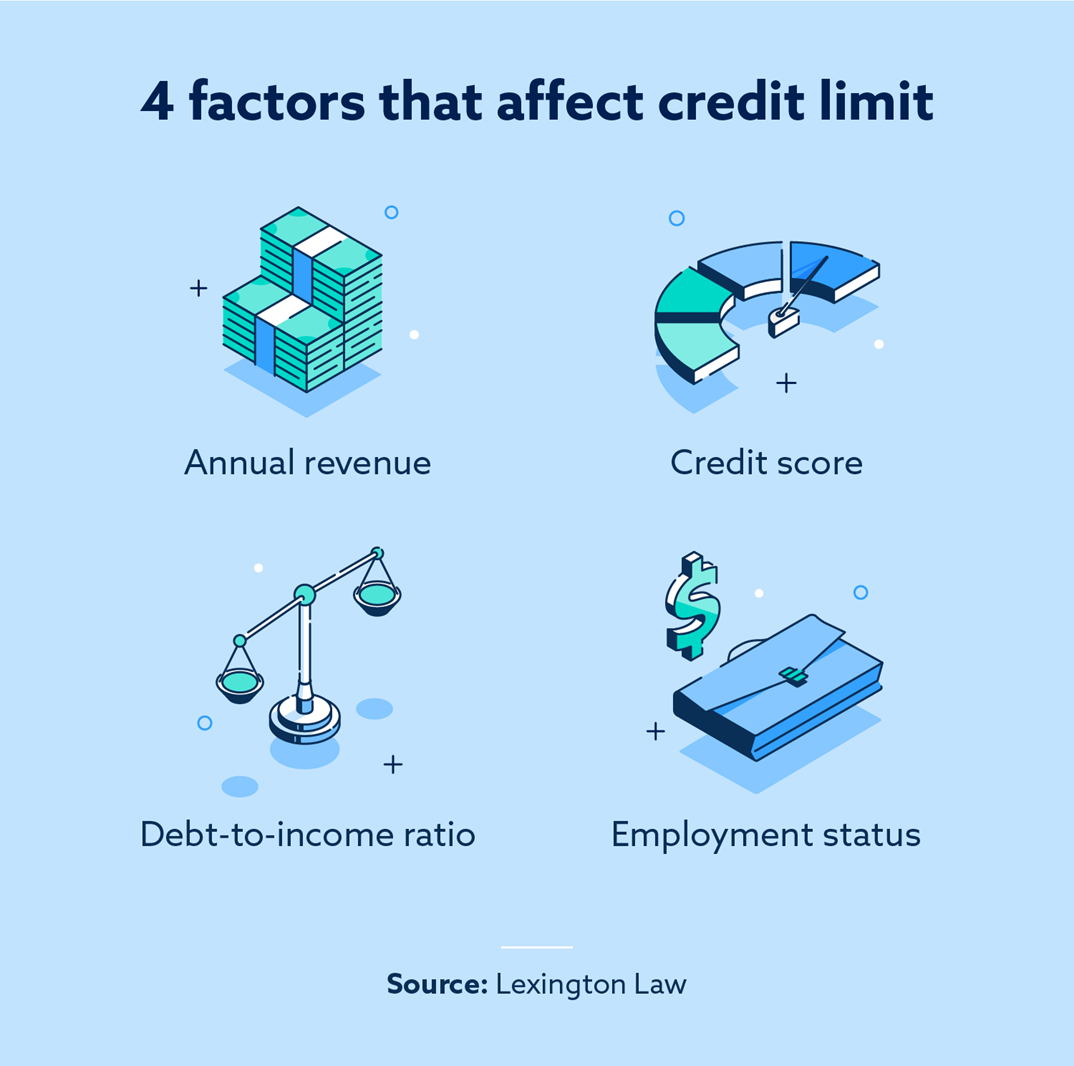

How are credit card limits determined?

Your credit limit is determined by the institution you borrow money from, whether they’re a bank, a credit union or a government agency. Credit limits take several factors into account, including your income and credit score. People with higher credit scores and income are normally approved for higher credit limits because lenders view them as financially responsible people.

Annual revenue

When a borrower applies for credit or asks for a credit limit increase, lenders look at annual revenue. From their perspective, a borrower with more income is more likely to make their payments on time—and vice versa.

Credit score

Credit scores help us qualify for auto loans, mortgage interest rates and credit cards—plus the limits we’ll receive when approved. If you have good credit, then you’ll likely be eligible for high-limit credit cards from the get-go.

Debt-to-income ratio

Lenders can use your debt-to-income ratio to set your credit limit by weighing your monthly debt payments against your total income. A low debt-to-income ratio can prompt lenders to offer higher credit limits since your spending habits show you regularly make responsible financial choices.

Employment status

Your employment status can also affect your credit limit largely due to timing. If you apply for a credit card or ask for a limit increase while you’re seeking a job, you’ll most likely receive a lower limit than you would as a full-time employee.

Credit limit vs. available credit

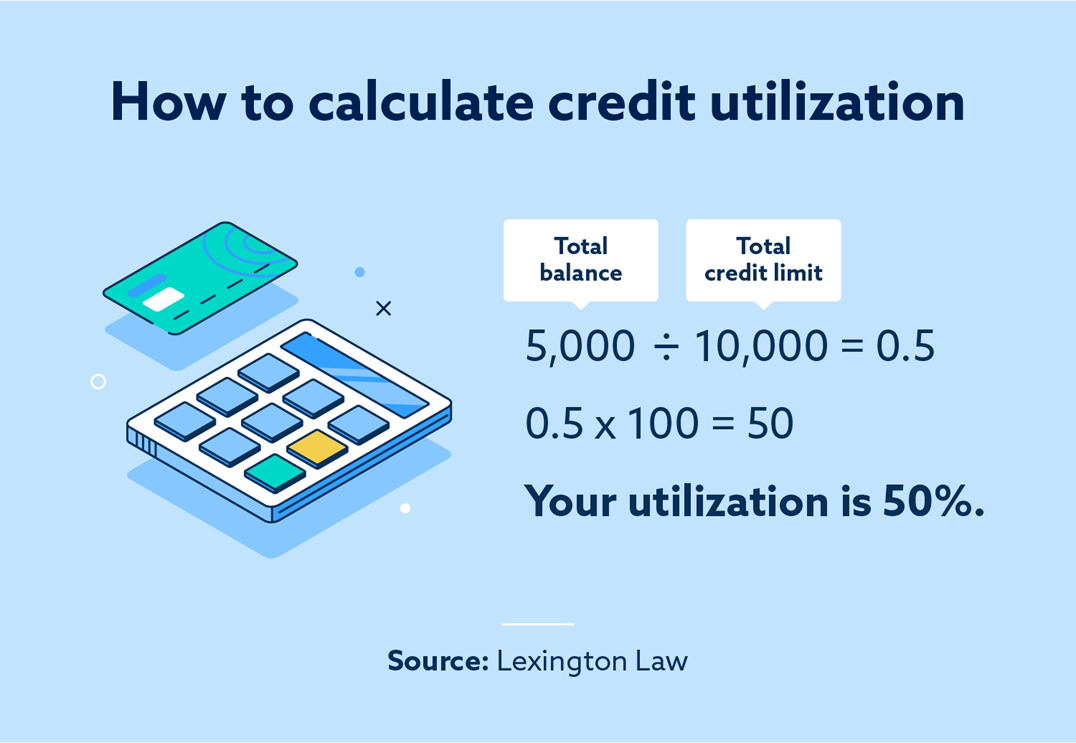

A person’s credit limit and their available credit are heavily tied together, which can cause people to confuse these two terms. To clarify, your available credit refers to the amount of money you can still borrow after calculating your debt. On the other hand, your credit limit refers to the total amount of money that your lender lets you borrow.

For example, if you have a $10,000 credit limit and spend $5,000, you’ll still have another $5,000 in available credit that you can access during this billing cycle. Your credit utilization ratio is calculated by weighing your available credit against your total credit limit. In this case, your credit utilization would be 50 percent.

How does your credit limit affect your credit score?

Whenever you ask a lender to increase your credit limit, they’ll perform a hard inquiry to review your credit history and help inform their decision. Inquiries briefly cause your score to dip, which is why conventional wisdom recommends not attempting to increase your credit limit right before applying for something vital—like a home or a new car.

Credit limits can also affect your score if you consistently have a high utilization ratio. Credit cards with high limits typically help borrowers maintain lower utilization ratios, which is beneficial for credit health.

What happens if you go over your credit limit?

Exceeding your credit limit can have negative consequences, especially if you do so repeatedly. Some of the drawbacks you might encounter include:

- Account review: A lender may review your longtime credit habits, which could potentially lead to a credit limit reduction.

- Credit score changes: Credit utilization makes up 30 percent of your FICO® credit score. Repeatedly going over your credit limit could significantly hurt your credit.

- Increased interest rates: Depending on your lender’s policies, they may issue a penalty APR on the offending account, which can be much higher than your standard rate.

- Overdraft fees: Most lenders will charge a $35 overdraft (or over-the-limit fee) after a specified time period if you don’t pay off your balance.

How to increase your credit limit

If you consistently make your monthly payments on time and keep your utilization low, the credit card issuer may approve your request to increase your limit. But remember to allow six to 12 months before asking. Your issuer probably won’t raise your limit after just one or two months of opening the account or if you’ve been making late payments.

Some credit card issuers will actively increase your limit after they review your account history. Sometimes, they’ll ask you to update your income. If you’ve earned a raise recently, you can provide that information, and the lender may increase your limit. When an issuer reviews your account like this, it does not cause a hard inquiry because you didn’t ask for them to review the account.

Work on your credit with Lexington Law Firm

Credit cards are fantastic resources that can positively impact your life when used responsibly. Even if you get approved for a high credit limit, it’s best to monitor your spending and borrowing habits. Lexington Law Firm offers great services like credit education tools and credit report analysis that may help you with your credit.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.