Even though it’s technically legal, you should avoid using your business credit card for personal use.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

A business credit card is a type of card designed to be used for business expenses—supplies, inventory, rent, payroll and equipment. Using a business credit card allows you to separate those expenses from your personal ones. Plus, business credit cards also offer higher spending limits and better terms.

However, the line between business and personal expenses isn’t always clear-cut. For example, you might book a business trip and then extend your stay to allow for some vacation time. Or, you might swipe your business card when you meant to use your personal card. Whatever the scenario, you might be wondering, “Can I use my business credit card for personal use?”

Continue reading to discover what the law says, in addition to the potential consequences of using your business credit card for personal expenses.

Table of contents:

- Is it illegal to use a business credit card for personal use?

- 6 drawbacks of using a business credit card for personal expenses

- I accidentally used my business credit card for personal expenses—now what?

Is it illegal to use a business credit card for personal use?

While it’s technically legal to use your business card for personal expenses, it generally isn’t recommended. Most credit card issuers have terms and conditions prohibiting users from swiping their business cards for personal use.

For example, the Capital One® commercial card terms state the following:

“Organization represents, warrants, and covenants that the Card Program (including any and all Accounts and Cards) has been established and will only be used by Organization and its Employees for a commercial or other bonafide business purpose. Organization further represents and warrants that none of the Account(s) or Card(s), and Transaction(s) related to the Card Program have been established or will be used for personal, family, or household purposes.”

Below is another example of the terms and conditions from the Ink Business Unlimited® Credit Card:

“By becoming a Visa® Business Card cardmember, you agree that the card is being used only for business purposes and that the card is being issued to a public or private company including a sole proprietor or employees or contractors of an organization.”

Nearly all other business credit card companies have similar rules against using your business card for personal expenses.

6 drawbacks of using a business credit card for personal expenses

While you might want to use your business credit card for personal use due to higher spending limits and other perks, the drawbacks often outweigh the benefits. Below are six potential consequences you may want to be aware of before you swipe your business credit card for a personal expense.

1. Your credit card issuer could close your account

As previously mentioned, using your business credit card for personal use violates the terms and conditions for many cards.

If your credit card company notices a pattern of purchases that are generally inconsistent with typical business expenses, they may launch an investigation. The issuer reserves the right to cancel your card if they find evidence that you violated the terms of your cardholder agreement.

2. You may be personally liable

A main benefit of incorporating your business is limiting your personal liability. When you form a Limited Liability Company (LLC), the corporation becomes a separate legal entity responsible for its own debt. As the owner, your personal assets are protected if a lawsuit is filed against your business.

However, when you combine your personal and business spending, you could be opening yourself up to liability. Known as “piercing the corporate veil,” this allows the courts to hold business owners responsible if they have improperly commingled personal and business finances.

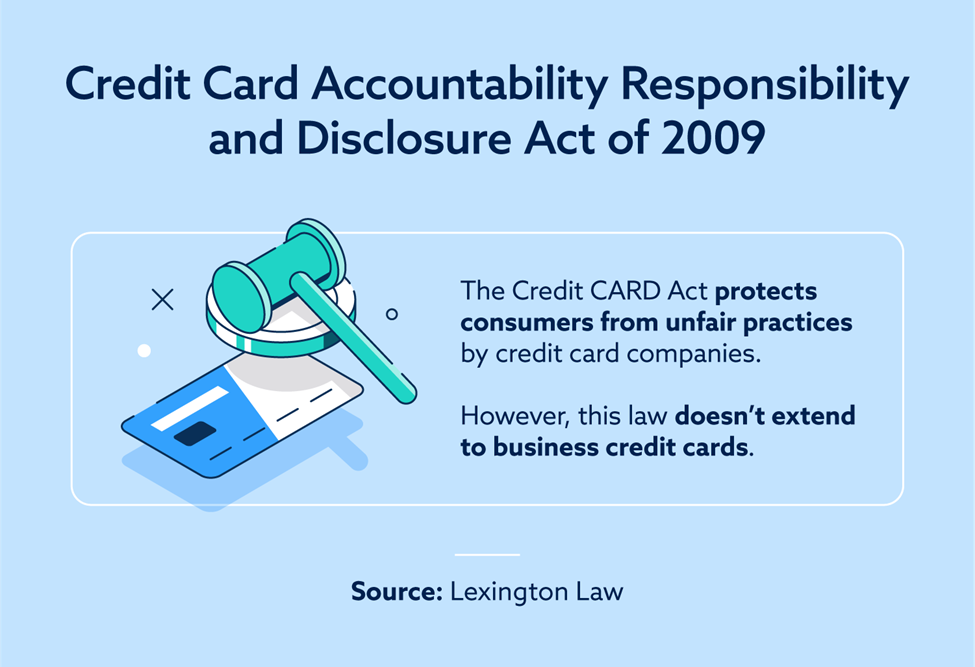

3. You may lose consumer protection

When you use a personal credit card, you’re protected under the Credit Card Accountability Responsibility and Disclosure Act of 2009 (Credit CARD Act). These protections include limits and advance notice requirements on APR, fee and finance charge increases. Since the Credit CARD Act doesn’t extend to business owners, you’ll miss out on these protections when you use your business card instead of your personal card.

Although some credit companies extend these protections to businesses, it’s not legally required, so check with your issuer.

4. Your credit scores may be impacted

Your personal credit score and business credit score are two separate entities and typically report to different credit bureaus.

Some people opt to use their business credit card to keep their personal credit utilization low. While this may seem like a good idea, there are other, less risky ways to lower credit utilization, such as making multiple payments in the same month.

Not to mention, if you make a personal purchase on your business credit card and fail to pay it off, this could negatively affect your business credit score. The consequences of poor business credit include an inability to get approved for loans, high interest rates and additional consequences that can hurt your business.

Failing to pay your balance can also hurt your personal credit due to the personal guarantee that you sign when you receive a business credit card. As the personal guarantor, if the business defaults on a loan, you’ll have to pay it off. If you can’t do so, your personal credit will likely take a hit.

5. You might struggle to track business expenses

When running a business, it’s essential to track your expenses to determine your profit margin. Doing so also helps you track cash flow and determine areas where you could cut costs. Using your business card for personal use can make tracking this much more difficult.

Additionally, you have to submit income and cash flow statements when applying for a business loan. If your personal and business expenses are intermixed, it can make the process of getting a loan more difficult.

6. Your taxes will be more complex

If your business is a corporation, you must file your business taxes separately from your personal income. When your personal and business expenses are mixed together, you’ll be scrambling to separate these once tax season approaches.

For example, if you frequently take clients out to dinner, it can be difficult to determine which bills were related to business and which were personal.

If the Internal Revenue Service (IRS) conducts an audit and finds that you claimed personal expenses as business expenses, you could get charged penalties or interest fees or potentially face legal action.

I accidentally used my business credit card for personal expenses—now what?

If you accidentally make a one-off personal charge on your business credit card, don’t fret. You can take the following steps to correct the mistake:

- Step 1: Flag the charge. Identify the charge so it doesn’t get mixed up in your business’s expenses.

- Step 2: Reimburse your business. Consider writing a check or transferring money to your business account to reimburse the charge.

- Step 3: Document the transaction. Maintain a record of this transaction that you can reference in case you’re audited by the IRS.

To summarize, using your business credit card for personal use isn’t recommended. While a one-off charge probably won’t hurt you, keeping your business and personal finances separate can protect against liability, streamline your expense tracking and simplify tax filing.

Remember that in some cases, your business credit card can affect your personal credit. Credit card companies may report delinquencies to consumer credit bureaus and business credit bureaus. To protect your personal credit, practice the same positive credit habits with your business credit card, including staying up-to-date on payments.

Looking to improve your personal credit? Start with a free credit assessment today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.