Building a good credit score takes time—when building your credit from scratch, you can typically expect to see a score within six months.

Key takeaways

- It typically takes about six months of responsible credit use to generate your first FICO® score, and roughly one to two years of on-time payments to reach a good score.

- Payment history and credit utilization carry the most weight in your score, so consistent on-time payments matter more than any single tactic.

- Rebuilding credit after a setback often takes longer than building credit from scratch, since you’re also working to offset existing negative marks.

- Tools like secured cards, credit-builder loans and becoming an authorized user can speed up the early stages without requiring you to take on debt you can’t manage.

- Late payments, high utilization and loan defaults are the mistakes most likely to add months or years back onto your timeline.

Building a good credit score takes time. If you’re starting from scratch, expect to see your first score within about six months, with another year or so of responsible use before you reach a good score range. How long it takes to build good credit beyond that first milestone depends largely on your circumstances, since rebuilding credit after a setback like a missed payment or bankruptcy typically takes longer than building it from nothing.

Your credit score affects far more than your ability to get approved for a credit card. It shapes the interest rates you’re offered, your odds of approval for loans and even what you pay for auto insurance in many states. This guide walks through a realistic timeline for building credit, what determines how fast you move through it and which habits to avoid so you don’t add months back onto the process.

How Long Does it Take a First Time User to Get a Credit Score?

It takes about six months on average to generate a credit score for the first time, since FICO® and most other scoring models need at least six months of reported account activity before they can calculate a number.

Plenty of people don’t have a score simply because they haven’t opened a qualifying account yet, not because anything is wrong with their finances. Recent graduates, new immigrants and anyone who has paid for everything in cash often fall into this category. Opening a single credit card or taking out a small loan and reporting on-time activity for a few months is usually enough to generate that first score. The factors that determine how quickly it improves from there are covered in the sections below.

How Long Does it Take to Get to the Next Credit Score Level?

These ranges are general estimates for how long it takes to build good credit through each tier, and your actual pace may vary based on your starting point, payment consistency and the specific accounts on your report.

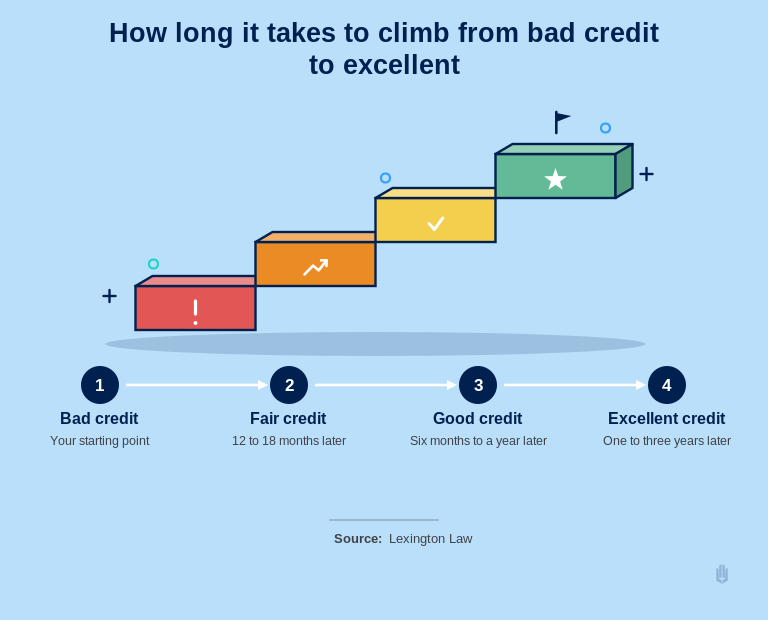

Bad to Fair

Moving from a bad score into fair territory often takes 12 to 18 months of consistent on-time payments. This stretch usually overlaps with an effort to rebuild credit after a missed payment, collections account or default, since those negative marks need time to age and lose weight in the scoring formula even as new positive history accumulates.

Fair to Good

Fair scores tend to climb into good territory within six months to a year for borrowers who keep utilization low and avoid new derogatory marks, since this range usually reflects a shorter or thinner credit history rather than active damage that needs to be overcome.

Good to Excellent

Good scores often take another one to three years to reach excellent territory, largely because length of credit history carries real weight at this stage and there’s no shortcut for waiting out the clock on your oldest accounts.

What Goes Into Your Credit Score?

Most lenders rely on either a FICO score or a VantageScore® when deciding whether to extend credit, and while the two models weigh similar factors, they apply different percentages to each one.

FICO Scores

A FICO score is a three-digit number between 300 and 850 that lenders use to gauge how likely you are to repay borrowed money, with a higher score signaling lower risk to the lender.

- Payment history (35 percent): On-time payments help your score, while late payments cause it to drop.

- Credit utilization (30 percent): This compares your balances to your available credit, so a $3,000 balance on a $10,000 limit puts you at 30 percent utilization.

- Length of credit history (15 percent): Longer histories of on-time payments tend to support a higher score.

- Credit mix (10 percent): A combination of account types, like a credit card and an auto loan, generally outperforms a single account type.

- New credit (10 percent): Opening several accounts in a short window can look risky to lenders evaluating new applications.

VantageScore®

VantageScore® is an alternative scoring model built by the three major credit bureaus and used by a growing share of lenders, with its own weighting across six factors.

- Payment history (40-41 percent): The single largest factor in this model, similar to FICO.

- Depth of credit (20-21 percent): Combines credit mix and account age into one category.

- Credit utilization (20 percent): Weighs balances against available credit, much like the FICO factor of the same name.

- Recent credit (11 percent): Reflects how many new accounts or inquiries have shown up lately.

- Balances (6-11 percent): Looks at your total balances across all accounts, separate from utilization.

- Available credit (2-3 percent): Considers how much unused credit you’re carrying across open accounts.

How To Build Credit Faster

These habits can shorten your timeline without requiring you to take on debt you can’t comfortably manage.

- Know your report: Pull your free reports at annualcreditreport.com so you know exactly what’s already being reported before you add anything new.

- Pay on time: Set up autopay for at least the minimum due, since payment history outweighs every other factor in both major scoring models.

- Use your cards wisely: Keep balances well below your limit and pay down what you carry whenever possible to keep utilization low.

- Get what you can afford: Auto loans, credit cards and mortgages all build your credit mix, but only take one on if the payment fits comfortably in your budget.

- Consider starter cards and loans: Secured credit cards and credit-builder loans are built for thin or damaged credit files and report to the bureaus just like traditional products. A secured credit card in particular can raise your score within a few months of consistent, low-balance use.

- Become an authorized user: Being added to a family member’s account in good standing can let their positive history show up on your report, provided the card issuer reports authorized users.

- Don’t close old accounts: Keeping older accounts open preserves your length of credit history even if you stop using the card regularly.

- Borrow only when it serves a purpose: Taking out a loan purely to diversify your mix tends to add risk without meaningfully speeding up your timeline.

- Check for incorrect information: An account that isn’t yours or a payment marked late in error can slow your progress. A free credit assessment from Lexington Law can help you spot those issues early.

What to Avoid When Building Your Credit

Building good credit takes months, but a single misstep can set you back by years, so it pays to manage your accounts carefully from the start.

- Late payments: A single late payment can stay on your report for up to seven years and is the fastest way to undo months of progress, so set reminders or autopay to avoid missing a due date.

- Multiple applications: Applying for several accounts in a short window signals risk to lenders. Compare offers first, then apply for one rather than three or four at once.

- High utilization: Running up your balances hurts your score and your finances, so keep balances well below your limit and follow a consistent plan to pay off debt you’re already carrying.

- Loan default: Missing payments for several consecutive months can lead to default, which compounds the damage with each missed payment and may even result in legal action from the lender.

- Maxing out your card: Using all of your available credit on a single card spikes your utilization ratio even if you pay it off shortly after, since issuers typically report your balance once per cycle.

- Closing old accounts: Shutting down your oldest card shortens your average account age and can reduce your total available credit, both of which work against you. If a closed account is reporting incorrectly, removing a closed account from your report may be worth pursuing.

How long it takes to fix bad credit after one of these mistakes depends on the severity. In general, plan on a longer road than the original timeline to build good credit, since you’re working to offset existing damage rather than starting clean. People wondering how long it takes to rebuild credit after a default or collections account are often looking at 12 to 24 months of rebuild credit work: steady on-time payments, lower balances and patience while the negative marks age.

Build a Strong Credit Future with Lexington Law

Negative items on your credit report, especially inaccurate ones, can quietly undo months of work toward building good credit if they go unchecked. A single error in collections status or an account that isn’t yours can hold your score back well past the timelines outlined above, even while you do everything else right. For some readers, the real concern isn’t a timeline at all but a credit score fix: removing an item that shouldn’t be there in the first place.

Lexington Law Firm’s advocates review your credit report, work with you to identify potentially inaccurate or unfair items and dispute them with the bureaus and creditors on your behalf, so you’re not stuck untangling reporting errors alone while you work to rebuild credit. Start with a free credit assessment to see where your report stands and whether any items are worth challenging.

Building good credit FAQs

Improving your credit score in 30 days is possible in a limited way, usually by paying down a high balance to lower your utilization before your next reporting date. For a bigger issue like fixing credit score damage from a late payment or default, plan on it taking several months rather than weeks.

The fastest way to build credit is usually to become an authorized user on a family member’s well-managed account or open a secured card and keep utilization low from the first statement. Both approaches start reporting positive history right away instead of waiting on other factors to improve.

You don’t start with a default credit score; instead, no score exists until you have at least one account reporting to the bureaus for roughly six months. Once that history exists, your starting score typically falls in the fair range rather than at the very bottom or top of the scale.

Checking your own credit score does not hurt it, since that’s considered a soft inquiry and isn’t visible to lenders. Only a hard inquiry, triggered when you formally apply for new credit, can cause a small, temporary dip.

Note:

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.