The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law Firm’s editorial disclosure for more information.

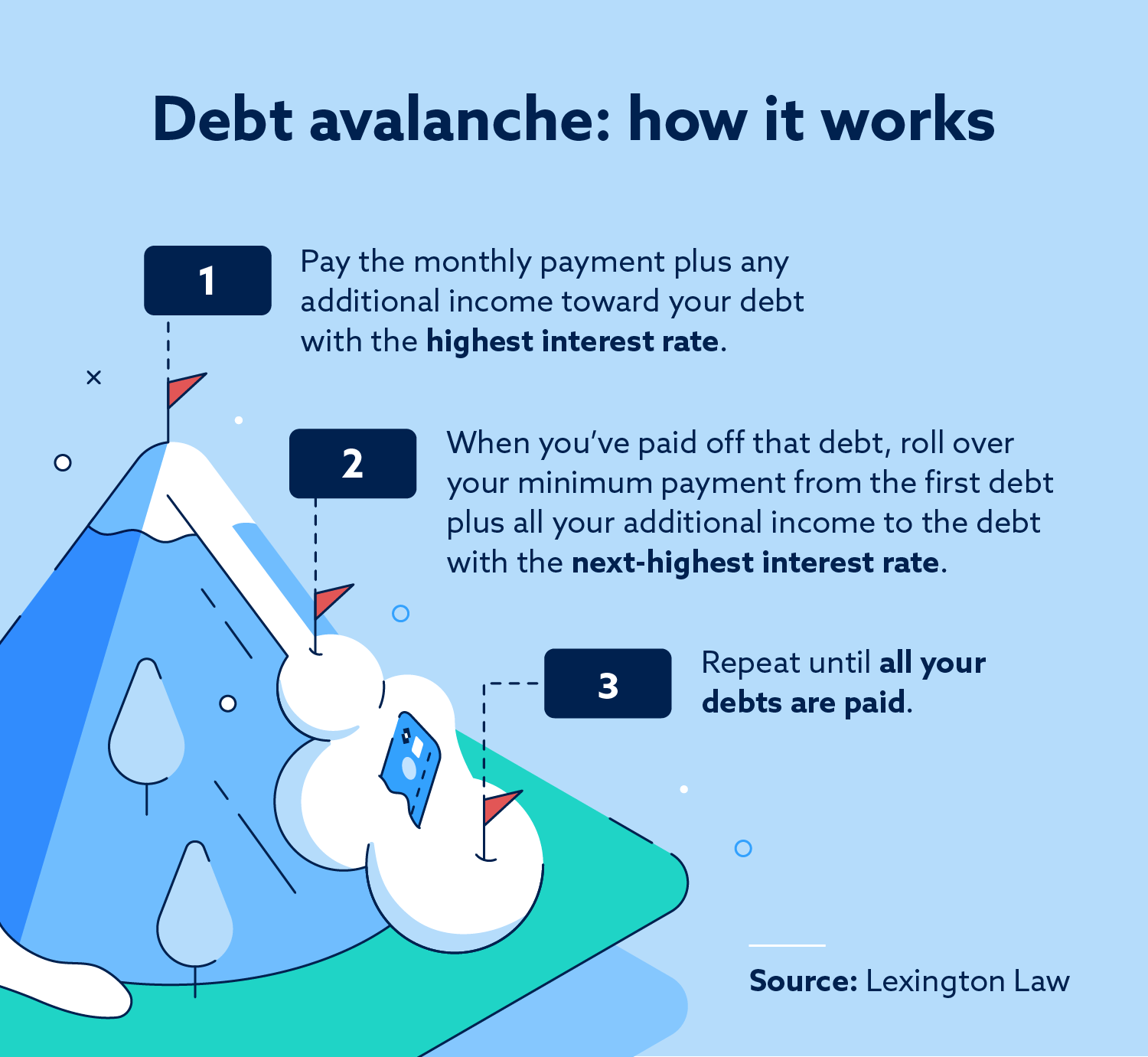

The debt avalanche method is an accelerated debt repayment strategy that involves paying off the debt with the highest interest first, then rolling those payments to your next highest-interest debt until all your debt is paid off.

Getting out of debt can seem overwhelming when you’re sitting at your kitchen table trying to pay bills each month or if debt collectors are harassing you. It’s even worse when all you can think about is everything else you could spend money on: a family vacation, a new car. But with a bit of dedication and a plan, it’s possible to regain your financial freedom with an accelerated debt repayment strategy like the debt avalanche method.

Read on to learn how to use the debt avalanche method to pay off your debt faster than you may have thought possible.

What is the debt avalanche method?

The debt avalanche method is an accelerated debt repayment method. When using this strategy, you make minimum monthly payments on all your debts and put any additional funds toward paying down the debt with the highest interest rate.

Once you’ve repaid that debt, roll that minimum payment and additional funds over into the debt with the next highest interest rate. Repeat the process until you’ve paid off all your debts.

The debt avalanche method is a good strategy for most types of debt:

- Student debt

- Credit card debt

- Auto loans

- Medical debt

Debt avalanche vs. debt snowball: What’s the difference?

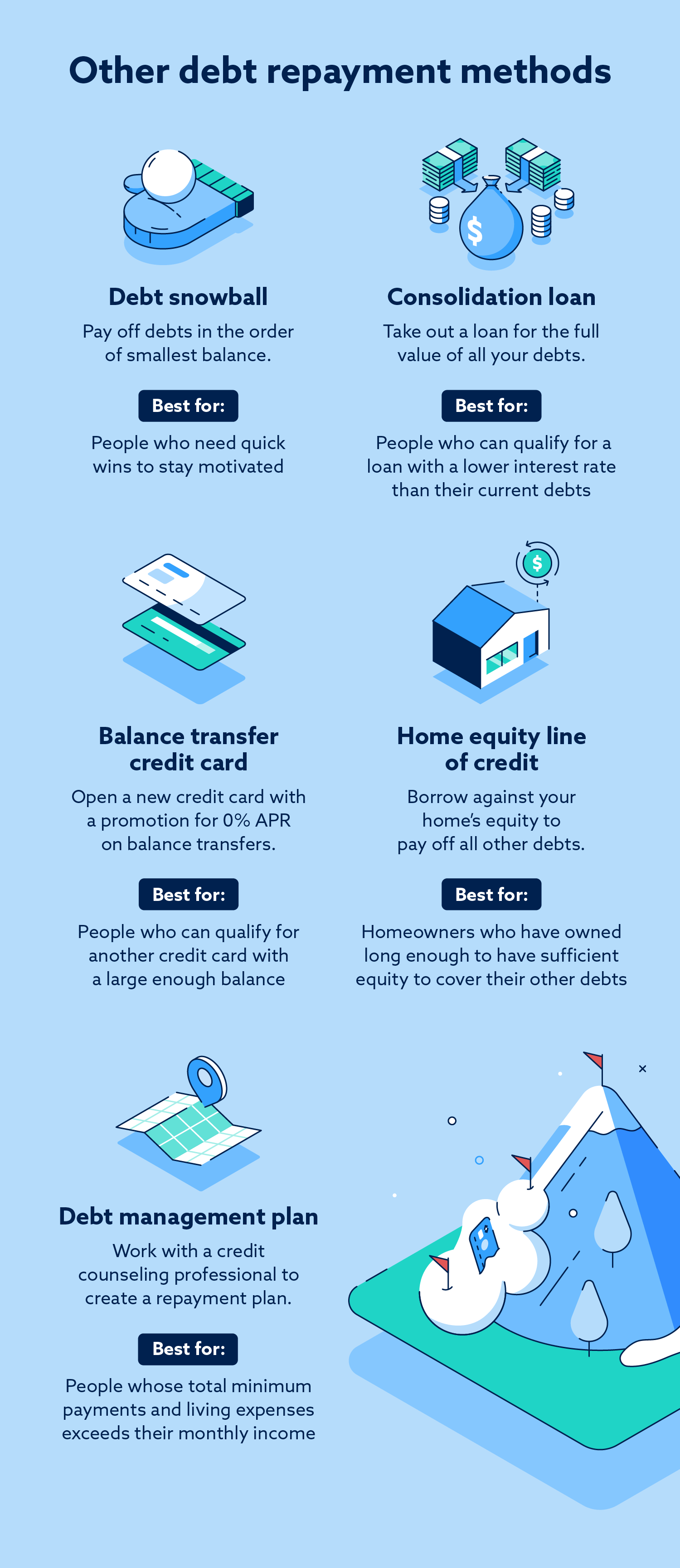

The debt avalanche is often compared to the debt snowball—another accelerated debt repayment method. In a debt snowball, instead of paying off the debt with the highest interest rate, you direct all your extra money toward paying off the debt with the lowest balance.

While both methods will pay off debt faster than if you had no strategy, you’ll see more quick wins if you opt for the snowball method, making it a good option for people who are easily discouraged.

You can also combine the two methods by prioritizing paying off the smallest debt with the highest interest rate to save on interest and see quick wins.

How to use the debt avalanche method to pay down debt

To use the debt avalanche method, follow these steps:

- Build up an emergency fund. This will ensure an unexpected bill doesn’t throw off your payment plan. Experts recommend having enough in your emergency fund to cover six months of living expenses.

- Make a list of all your debts. Include their balances, interest rates and minimum payment amounts. Organize your list from the highest interest rate to the lowest.

- Total your monthly expenses and income. Add up all the money you spend on monthly living expenses and monthly minimum payments on debt. Also note your monthly income.

- Determine how much money you have to put toward additional debt payments. Tally what you have left over each month after paying monthly expenses and minimum payments. You’ll put this “extra money” toward debt each month.

- Each month, put the extra money toward the debt with the highest interest rate. This should be in addition to the regular monthly minimum payments.

- Put any unexpected income toward the debt with the highest interest rate. If you get any unexpected income, such as a tax refund or bonus at work, put that toward your accelerated payment as well.

- When you’ve paid that debt off, roll over that debt’s minimum payment and your extra monthly income toward the debt with the next highest interest rate. Continue paying the minimum payment on all other debts.

- Repeat until you’ve cleared all your debts. As you pay off debts, your payments to the other debts will increase.

Debt avalanche example

Let’s look at an example use of the debt avalanche method.

You have three outstanding debts:

- A student loan for $10,000 with 5 percent interest and a minimum monthly payment of $400

- A credit card debt of $5,000 with 25 percent interest and a minimum monthly payment of $100

- A home repair loan for $3,000 with 15 percent interest and a minimum monthly payment of $275

And after monthly living expenses and the three minimum payments, you have $250 leftover in your budget to put toward accelerated payments.

Since your credit card debt has the highest interest rate, start by paying the extra $250 in addition to the $100 monthly payment. That means you’ll pay $350 each month.

Once you’ve paid off your credit card debt, your debt with the next highest interest rate is the home repair loan, so that’s where you’ll start sending your extra payments each month. Roll over the $350 you paid monthly for the credit debt to the home repair loan. Added to the minimum payment of $275, you’ll pay $625 toward the loan each month.

When the home repair loan debt is clear, focus on your student loan, which has the lowest interest rate of your three debts. Roll over the $625 you were paying to the home repair loan to the minimum payment for the student loan, for a total monthly payment of $1,025.

If you use the debt snowball method discussed earlier, you’d start by paying off your smallest debt, which in this case is the home repair loan.

Pros and cons of the debt avalanche method

The debt avalanche method is one of the most logical and cost-effective debt repayment plans, but it isn’t perfect.

The advantages of the debt avalanche method are:

- You’ll save on interest. This method helps you pay off your debt early, saving you what you would have paid in interest.

- You’ll pay back your debt faster. By steadily making payments larger than the minimum, you can shave months off your repayment plan.

The disadvantages of the debt avalanche method are:

- Larger debts can take longer to pay back. If you know you need small wins to stay motivated, this can negatively impact your ability to stick with your accelerated payment plan.

- Unexpected bills or unstable income can hinder your progress. This method only works if you can make regular payments larger than your minimum payment.

Other ways to pay off credit card debt

While many people find the debt avalanche method to be a helpful strategy for getting out of debt, there are other ways to pay off debt that may better fit your situation.

You can also use any of the following methods:

- Balance transfer credit card: Some credit cards have promotional offers for 0 percent APR on balance transfers to new customers. If you qualify, you can transfer your debt on a high-interest credit card to one of these cards. Pay attention to when the promotional 0 percent APR ends, or you’ll have to pay interest again. In this situation, it makes the most sense to devote any extra income after monthly expenses to this debt to clear it faster.

- Debt consolidation loan: Take out a loan for the amount of all your debt and use the money to pay off those individual debts. Then pay off your consolidation loan each month. This makes repayment easier because you’re only making one monthly payment, but be careful that the interest rate on your consolidation loan is less than the interest rates on your other debt. Otherwise, you’ll end up paying more in interest over time.

- Home equity line of credit: Borrow against your home’s equity. Often these lines of credit have lower interest rates than credit cards.

- Debt management plans: If you cannot pay off your debt within five years even with a strict budget, or if your total monthly minimum payments are more than your monthly income, consider getting professional help. A debt counselor can help you create a debt management plan to pay off your debt. However, secured debt (a debt with collateral, such as your car or your home) won’t qualify for a debt management plan.

Is the debt avalanche method right for you?

The debt avalanche method is an excellent option for repaying debt faster, but it doesn’t fit every situation. If you are intent on saving money while you repay debt and are motivated enough to keep going without small wins along the way, the debt avalanche method may be your path to financial freedom. While using the debt avalanche—or any accelerated debt repayment plan—it’s essential to continue with behaviors that maintain or improve your credit. Stay current on all your bills, create and stick to a budget and track your spending. Lexington Law Firm may be able to help you on your journey to repair your credit. Take our free credit assessment today to learn more.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.