The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

You can get out of credit card debt by taking stock of your debt, finding your preferred payment strategy, creating a budget and sticking to it.

Getting out of credit card debt can be difficult, but there are steps you can take that will help, such as finding your preferred payment strategy and creating a budget. Depending on the size of your debt, this process can take some time, so it is important to be patient. Remember that credit card debt is common, but with careful planning, many people are able to free themselves from debt entirely.

Read on to learn more about how to get out of credit card debt by following three simple steps.

Step 1: Take stock of your debt

Before creating a debt repayment plan, take stock of your debt first. If you have other debts aside from your credit card, remember to take them into account as well.

Here’s what to do when evaluating your debt:

- Determine your credit card balances. Figure out your balances for each of your credit cards and list them out from highest to lowest.

- Figure out your interest rates. Just like with your balances, figure out the interest rate for each credit card and list them from highest to lowest.

- Compare your debt, income and other expenses. Determine how much you owe in debt, along with any other necessary expenses.

Knowing and fully understanding your current financial situation is critical in making the right decision when it comes to your credit card debt. Prioritizing paying off certain accounts over others will have different benefits.

After following the steps above, you’ll have all of the financial information you need to guide your decision-making. It may be shocking to see the total amount of your debts and expenses, and it can be overwhelming. Remember that no matter how much debt you have, if you invest time and energy into making a feasible repayment plan, you’re setting yourself up for success moving forward.

Once you have a grasp on your finances, you’re ready to take the next step.

Step 2: Find your preferred payment strategy

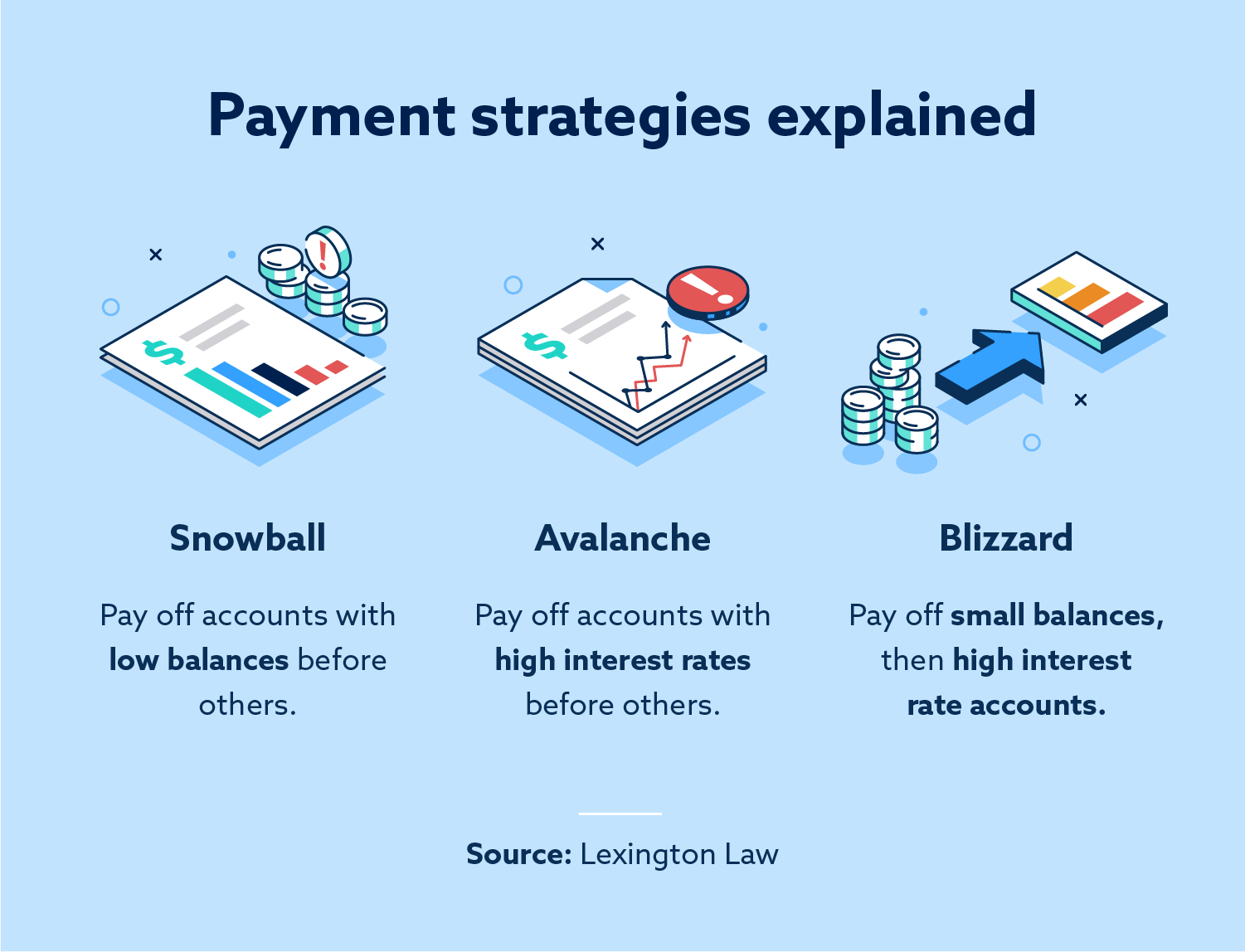

Three of the most common strategies for repaying your credit card debt are the snowball, avalanche and blizzard methods. Automating your payments can also help. Each of these methods has its own pros and cons, and will benefit people in different situations.

Snowball

With the snowball method, you pay off your accounts with the smallest balances first, working up to the ones with the highest. Always make the minimum monthly payment for each account, but use any remaining money on the card with the lowest balance. Once that card is paid off, put your extra money toward the card with the next lowest balance, and so on.

This method can be emotionally rewarding, but it won’t save you as much money as others in the long run.

Advantages:

- Decreases your number of open accounts faster

- Is emotionally rewarding, as you can see progress quicker

- Can be easier to stick to

Disadvantages:

- Does not save you as much money over time as other methods

Avalanche

The avalanche method involves paying off debts with the highest interest rates first. Every month, make minimum payments on each of your accounts, except the one with the highest interest rate. With this account, pay the minimum plus any extra you can afford.

The avalanche method can save you a lot of money in the long run by reducing your interest charges, but it can be challenging to stick to.

Advantages:

- Saves you more money in the long run by reducing interest charges

- Can help pay off other debts faster with money saved from interest charges

Disadvantages:

- Can be more difficult to follow

- Makes it harder to see your progress

Blizzard

The blizzard method can be seen as a combination of the snowball and avalanche methods: Pay off your smallest debt first to get the emotional and psychological benefits of the snowball method, then switch to paying off your account with the highest interest rate.

The blizzard method will give you the best of both worlds and more freedom in your financial decisions.

Advantages:

- Offers the advantages of both the snowball and avalanche methods

- Is emotionally rewarding and can save you more money than the snowball method

- Offers more freedom in choosing what debts to pay off

Disadvantages:

- Still does not save you as much money as the avalanche method alone

Automation

Automating your debt payment can make the process much easier. Fortunately, there are many different websites, apps and services that can help you automate your payments. These tools can connect to your bank accounts, credit cards, loans and much more. You can also automate your credit card payments for free with automatic bill pay features.

Automation can give you the peace of mind that other methods can’t, as long as you can consistently afford your monthly payments.

Advantages:

- Stops you from forgetting any payments

- Gives you less to worry about when it comes to your bills and payments

Disadvantages:

- Makes it easier to lose track of progress and your debt repayment goals

Working with the strategies above, you might want to consider using a balance transfer card with a zero percent introductory APR. These cards let you transfer debt from one account to another, and moving debt from a high-interest account to one with zero percent APR can save you a lot of money.

Step 3: Create a budget and stick to the plan

Once you’ve chosen your payment strategy, you’re ready to create a budget. This budget will help you track and plan out your spending, making it easier for you to get out of credit card debt. When it comes to any financial plan, budgeting is key. Here are a few steps you can take when figuring out your budget.

1. Calculate income

How much income can you rely on every month? How much is left after taxes? These are important questions to ask yourself when crafting your budget. Include all forms of income, even outside sources of income that are not related to your job.

Here are some sources of income you may include:

- Income from work

- Gifts from family and friends

- Tax refunds

- Savings interest

- Stock dividends

2. Determine required expenses

Write down a list of all the expenses you have for the month—anything from house and car payments to grocery bills and insurance. Use bank statements, credit card bills, receipts and anything else you can to track your expenses.

Some typical expenses that you should include are:

- Mortgage or rent payments

- Insurance payments

- Car payments

- Utility bills

- Grocery bills

3. Create a payoff strategy

Once you’ve calculated your income and determined your required expenses, you’re ready for your payoff strategy. You can either make the minimum payment each month, pay more than the minimum or use a balance transfer card. Following one of the payment strategies above will make creating your payoff strategy easier.

After you’ve created your budget, it’s important to stick to your payoff strategy. Make sure that your plans, goals and timeline are realistic. Track your progress and remember to hold yourself accountable.

Automated payments can help you make your payments on time, and removing your credit cards from any online stores will help you avoid unnecessary purchases that can further increase your debt.

If you have mounting credit card debt and you don’t know where to turn, the credit repair consultants at Lexington Law Firm are seasoned and knowledgeable with the credit repair process and could assist you in repairing your credit.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.