The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Illegal debt collection practices include debt parking, phantom debt collection, not providing sufficient communication of debt, creditor harassment and more.

While many debt collectors are prone to making honest mistakes, many knowingly break the law in an effort to collect debt from you. In 2019, approximately 75,200 consumers filed complaints regarding debt collectors—all of which were related to unfair and abusive debt collection practices.

Attempts to collect debt not owed continues to be the most common debt collection practice. According to the Bureau of Consumer Financial Protection’s annual report, 48 percent of people said they were asked to pay a debt that was not theirs and 25 percent said they were charged with a debt from an identity fraud instance. Aside from this, 22 percent said they had already paid the debts, while four percent of consumers said the debt was discharged in bankruptcy and was no longer owed.

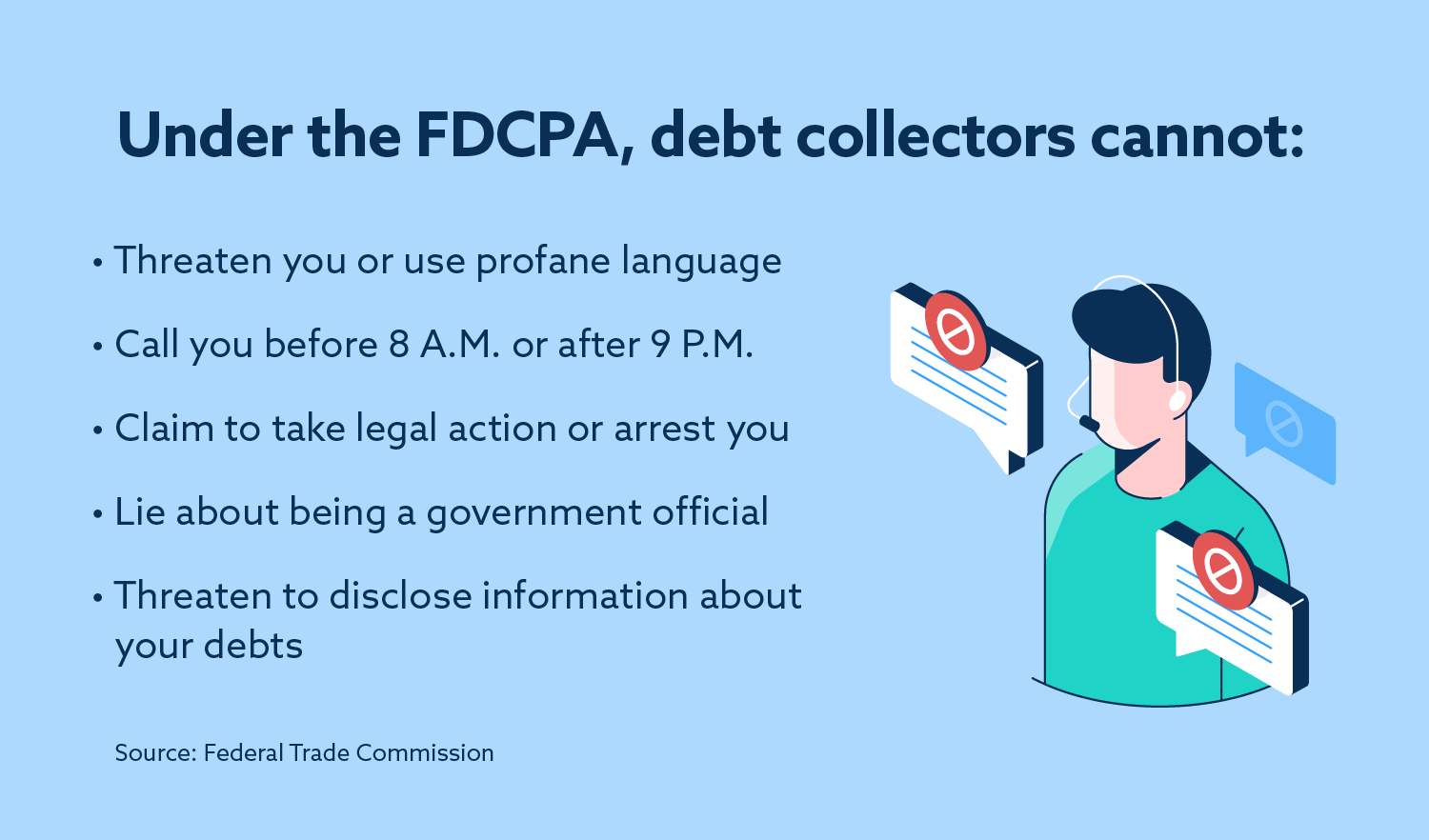

To stop these actions from occurring, the Financial Trade Commission issued the Fair Debt Collection Practices Act (FDCPA), which makes it illegal for debt collectors to use these unfair collection practices.

To avoid falling for these debt collection scams, it’s important to know your rights under the Fair Credit Reporting Act (FCRA) and FDCPA. Below we address common illegal debt collection practices as well as tips for protecting and understanding your rights.

1. Debt parking

Passive debt collection, also referred to as “debt parking,” is a common tactic used by debt collection agencies where they place false or questionable debts onto a consumer’s credit report without contacting the consumer. These debts often go unnoticed by the consumer until they apply for a loan or a job.

These debts will show up when their credit report is evaluated, and to avoid interfering with the approval process, the consumer may choose to pay off the debts rather than file a dispute.

This tactic has unfortunately been used many times, with the Midwest Recovery Settlement being a prime example. According to Andrew Smith, director of the FTC’s Bureau of Consumer Financial Protection (CFPB), the defendants on this case “used this illegal ‘debt parking’ to coerce people to pay debts they didn’t owe or didn’t recognize.”

2. Phantom debt collection

According to the FDCPA, debt collectors are prohibited from misrepresenting the amount of debt you owe. Phantom debt collectors violate this act by reporting debts that have never existed, are already paid for or are past the statute of limitations, which they do not have legal rights to collect.

In 2019, 45 percent of consumer complaints that were filed were because of attempts to collect debts that were not owed. These debt collectors will often use aggressive, deceptive and threatening behavior in an attempt to collect funds from consumers.

3. Not providing sufficient communication of debt

The FDCPA requires debt collectors to provide consumers with a written notice within five days of contacting them.

In 2019, 65 percent of consumers said they did not receive enough information to confirm ownership of their debt, while 30 percent complained that their notice did not include information on their right to dispute.

By federal law, the collection agency must send you a written notice detailing:

- The amount of debt owed

- A statement explaining your rights to dispute the debt owed

- The name of the creditor you owe the debt to

4. Creditor harassment

Under the FDCPA, debt collectors are not allowed to harass you in any way. This includes threatening you with violence or harm, using profane language or repeatedly calling you.

In 2020, the Consumer Financial Protection Bureau issued the “Final Rule,” which restates consumer rights under the FDCPA. Under this new rule, debt collectors are prohibited from contacting you more than seven times in seven consecutive days or within seven days of engaging in a conversation with you.

5. Falsely identifying themselves

In 2019, 11 percent of complaints that were filed were related to false statements or representations. Many collectors will falsely represent themselves, claiming to be a government official, law enforcement official or legal attorney—all of which are claims that are in violation of the FDCPA.

6. Threatening legal action

In addition to falsely identifying themselves, collectors will go as far as to threaten to take legal action—with 12 percent of consumers filing complaints on this matter in 2019. The collector will use scare tactics to threaten the consumer, claiming that failure to pay the debts will result in imprisonment. Though debt collectors can sue you over debts, they cannot threaten to arrest you or claim to take legal action against you if the alleged debts are not accurate.

7. Contacting your family or place of work

Three percent of consumer complaints in 2019 involved a debt collector threatening to contact someone or share information improperly. Debt collectors are allowed to contact your spouse and credit reporting agencies about your debts, but they are not allowed to disclose information about your debts to family members or employers.

8. Charging interest or adding fees not previously authorized

Debt collectors are not allowed to collect interest or fees on top of the debt you already owe, unless the original contract or your state law allows it. Even small fees of a few dollars are unlawful unless authorized in the debt agreement.

How to protect yourself from illegal debt collection practices

In addition to understanding your rights under the FDCPA, it’s important to know the steps you can take to protect yourself from these illegal practices:

Collect information on your debt

If you have not received a written statement from the debt collector regarding the amount of debt you owe, request it. This will detail all of the information you need to know about the debt and how to proceed with a dispute.

You can have a credit agency validate your debt by sending a debt validation letter. Under the FDCPA, you have 30 days to request validation after a collector contacts you about a debt. If the creditor cannot verify the debt, ask them to remove the information from your credit report to avoid impacting your credit score.

Cease communication

Under the Final Rule, if you’re being contacted by collectors electronically, you are allowed to use this form of communication to say that you refuse to pay the debts and tell the debt collectors to stop contacting you.

This provides clear rights for consumers, and according to CFPB Director Kathleen L. Kraininger, “with this modernized debt collection rule, consumers will have greater control when communicating with debt collectors.”

Dispute your debt

You have 30 days after receiving a notice to send a dispute letter to a collector. You should also file a credit dispute with all three of the major credit bureaus and ask that the inaccurate information be removed or corrected. Failure to comply is a violation of the Fair Credit Reporting Act.

Get an attorney

If you want to take legal action against a debt collector and are unsure about certain debts, consider hiring a consumer law attorney to represent you. Once you are represented by an attorney, the debt collector must only communicate with that attorney moving forward.

File a complaint

If you’ve been targeted by collectors using illegal practices, you can file a report with one of the following:

- The Federal Trade Commission

- The Consumer Financial Protection Bureau

- Your state attorney general’s office

Protecting your credit

As a consumer, it’s important to monitor your credit report for any inaccuracies, especially when dealing with these illegal debt collection practices. Errors on your credit report can cause serious harm to your finances and your credit. If you need help finding inaccurate items on your credit report, validating debt claims or improving your credit score, explore our credit repair options today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.