The statute of limitations on debt typically ranges 3 – 6 years, depending on the debt type and the state you live in.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Is there a statute of limitations on debt? It depends on the type of debt and which state’s law governs it. Find out more about the statute of limitations on suing to collect a debt by state below.

Table of contents:

- What is a statute of limitations on debt?

- The four types of debt

- Statutes of limitations by state

- When does the statute of limitations clock start?

- Delinquent debt and your credit report

- FAQ

What is a statute of limitations on debt?

A statute of limitations on debt limits how long creditors or collection agencies can only take legal action against you to collect a debt. The length of that period depends on the statute of limitations in the state where the debt originated.

Statutes of limitations are laws that govern the deadlines for certain legal actions. But don’t be mistaken—you aren’t off the hook for a debt just because the statute of limitations has passed. The debt might still show up on your credit report, and if you don’t pay it, you could face trouble getting future credit, especially a mortgage.

The statute of limitations does prevent you from being successfully sued for time-barred debts. That means the creditor won’t be able to get a judgment against you that allows them to garnish wages or levy your accounts.

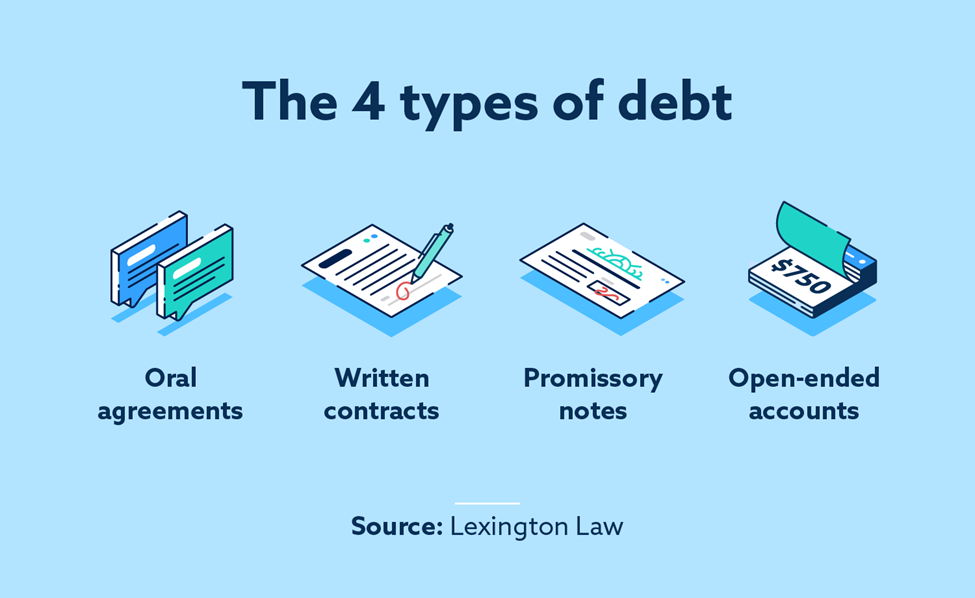

The four types of debt

The type of debt you are dealing with determines which statute of limitations might be relevant. Read on to learn about the four different types of debt.

Oral agreements

Oral agreements occur when you borrow money from someone and agree to pay it back according to specific terms, but the agreement isn’t in writing.

This is the proverbial handshake agreement, and it’s not extremely common between traditional lending organizations and borrowers today. This is mainly because they’re difficult to prove. Oral contracts are more likely to exist between family members or friends.

Written contracts

Written contracts record the details of a lending agreement, including the borrow amount and date, the purpose of the loan, interest amount, when and how to make payments and other terms. Both parties involved in the contract—the borrower and the lender—sign the document to validate it.

Written contracts are easier to prove than oral contracts. Vehicle loans are written contracts. Medical debt or payments for services you agreed to in writing are also written contracts.

Promissory notes

Promissory notes are similar to written contracts but with less detail. In addition, they only need to be signed by the borrower to be enforceable. You generally sign a promissory note when you take out a mortgage or student loan.

Open-ended accounts

Typically, these are revolving accounts such as credit cards or lines of credit. Open-ended accounts remain open for an undetermined length of time as long as you are making regular and agreed-upon payments. You can also carry a balance on these accounts as long as you make regular minimum payments.

Statutes of limitations by state

This guide to statutes of limitations on debt collection by state is for informational purposes only. Debt laws change from time to time, and you should always check with a legal professional or your state Attorney General’s office for current information.

| State | Oral Agreements | Written Contracts | Promissory Notes | Open-Ended Accounts |

| Alabama | 6 years | 6 years | 6 years | 3 years |

| Alaska | 3 years | 3 years | 3 years | 3 years |

| Arizona | 3 years | 6 years | 6 years | 6 years |

| Arkansas | 3 years | 5 years | 5 years | 5 years |

| California | 2 years | 4 years | 4 years | 4 years |

| Colorado | 6 years | 6 years | 6 years | 6 years |

| Connecticut | 3 years | 6 years | 6 years | 6 years |

| Delaware | 3 years | 3 years | 3 years | 3 years |

| Florida | 4 years | 5 years | 5 years | 5 years |

| Georgia | 4 years | 6 years | 6 years | 6 years |

| Hawaii | 6 years | 6 years | 6 years | 6 years |

| Idaho | 4 years | 5 years | 5 years | 4 years |

| Illinois | 5 years | 10 years | 10 years | 5 years |

| Indiana | 6 years | 6 years | 10 years | 6 years |

| Iowa | 5 years | 10 years | 10 years | 5 years |

| Kansas | 3 years | 5 years | 5 years | 5 years |

| Kentucky | 5 years | 10 years | 15 years | 10 years |

| Louisiana | 10 years | 10 years | 10 years | 3 years |

| Maine | 6 years | 6 years | 20 years | 6 years |

| Maryland | 3 years | 3 years | 6 years | 3 years |

| Massachusetts | 6 years | 6 years | 6 years | 6 years |

| Michigan | 6 years | 6 years | 6 years | 6 years |

| Minnesota | 6 years | 6 years | 6 years | 6 years |

| Mississippi | 3 years | 3 years | 3 years | 3 years |

| Missouri | 5 years | 10 years | 10 years | 5 years |

| Montana | 5 years | 8 years | 5 years | 5 years |

| Nebraska | 4 years | 5 years | 5 years | 4 years |

| Nevada | 4 years | 6 years | 3 years | 4 years |

| New Hampshire | 3 years | 3 years | 6 years | 3 years |

| New Jersey | 6 years | 6 years | 6 years | 6 years |

| New Mexico | 4 years | 6 years | 6 years | 4 years |

| New York | 6 years | 6 years | 6 years | 6 years |

| North Carolina | 3 years | 3 years | 3 years | 3 years |

| North Dakota | 6 years | 6 years | 6 years | 6 years |

| Ohio | 6 years | 6 years | 6 years | 6 years |

| Oklahoma | 3 years | 5 years | 6 years | 3 years |

| Oregon | 6 years | 6 years | 6 years | 6 years |

| Pennsylvania | 4 years | 4 years | 4 years | 4 years |

| Rhode Island | 10 years | 10 years | 10 years | 10 years |

| South Carolina | 3 years | 3 years | 3 years | 3 years |

| South Dakota | 6 years | 6 years | 6 years | 6 years |

| Tennessee | 6 years | 6 years | 6 years | 6 years |

| Texas | 4 years | 4 years | 4 years | 4 years |

| Utah | 4 years | 6 years | 6 years | 4 years |

| Vermont | 6 years | 6 years | 6 years | 6 years |

| Virginia | 3 years | 5 years | 6 years | 3 years |

| Washington | 3 years | 6 years | 6 years | 6 years |

| West Virginia | 5 years | 10 years | 6 years | 5 years |

| Wisconsin | 6 years | 6 years | 10 years | 6 years |

| Wyoming | 8 years | 10 years | 10 years | 8 years |

Source: The Balance

When does the statute of limitations clock start?

According to the Federal Trade Commission, the statute of limitations clock starts when you fail to make an agreed-upon payment. However, you can reset the statute of limitations clock in some cases by making a payment on the debt or agreeing to make such payments in response to a debt collector contacting you.

Before you make any promises or make a payment on old debt, ensure you understand your rights under the Fair Debt Collection Practices Act and the statute of limitations on your debt.

Delinquent debt and your credit report

In most cases, negative items such as delinquent accounts or unpaid collections will fall off your credit report after seven years. That’s seven years from the date that the account first became delinquent.

As you can see from the table above, many states’ statutes of limitations are below seven years. That means that your credit could reflect an account that is past the date for legal collection methods. If you legitimately owe the debt in question, your choices include:

- Pay the debt off to have it show up as paid—which can be better in the eyes of potential creditors;

- Try to negotiate with the creditor, potentially for a pay for delete or a settlement that lets you pay less than you owe to have the account marked paid in full; or

- Wait for the item to fall off your credit report.

FAQ

Below are a few common questions about the statute of limitations on debt.

What can restart the debt statute of limitations clock?

Making a payment on a debt in some states will restart the statute of limitations clock. In addition, promising to pay a debt also revives the old debt, and a new statute of limitations will begin.

Why are there statutes of limitations on debt?

Statutes of limitations set a time limit for when debt collectors and creditors can take legal action against a borrower who defaulted on their debt. After the statute of limitations time limit has expired, creditors and debt collectors can no longer file a lawsuit to collect on the debt. These limitations help protect borrowers from being liable for old debts.

What happens after 10 years of not paying debt?

Typically, after 10 years of not paying debt, the statute of limitations will have passed. This means that while you technically still owe the debt, debt collectors may try to collect it, but they typically cannot pursue legal action against you.

The statute of limitations varies by state, so be sure to reference your state’s specific statute of limitations to determine what legal action a creditor can take against you.

Talk to a professional if you have questions

If a collection agency contacts you about a debt after the statute of limitations has passed, they typically have no legal standing to sue to collect the debt. That doesn’t mean they may not try to collect, and if you’re dealing with an aggressive creditor or aren’t sure how the law impacts your debt, you may want to contact a professional. Additionally, if a collection agency is reporting very old debts to the credit bureaus, you might be able to dispute the information to improve your credit profile. Work with Lexington Law Firm to learn more about credit repair and how to ensure the accuracy of your credit report.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.