The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Have you ever wanted to send money in the mail without writing a check? Money orders are one way you can make a payment to someone else without involving your personal financial information. Find out more about this payment method and how it works below.

What Is a Money Order?

Money orders are pieces of paper that act as a form of payment. They look a little like checks, and they’re similar to checks in that they’re worth the value written on them.

But unlike checks, money orders don’t draw on funds in your checking account. You pay for them as if you’re buying a product. Here’s more on how they work.

How Do Money Orders Work?

Money orders let you provide a guaranteed form of payment to someone else. You prepay for the money order with cash or a debit card. In select cases, you may be able to pay with a credit card. You can’t buy a money order with a check.

When you buy a money order, you state how much you want it for. You pay for the face value of the money order plus the cost of the money order. The service you buy it from prints the money order with details, including the date and the amount the order is for.

Some services print who the money order is made out to. Others leave that blank, and you complete that information. You must also sign the money order and add pertinent information, which can include the account number for the payment and your own address.

You can then transfer the money order to the other person or business as a form of payment. You can hand it to them personally or mail it. Once they receive the money order, they can treat it like a check, depositing it into their bank account or cashing it at various locations that provide such services.

Where Can I Get Money Orders?

Money orders can be purchased at the post office. They can also be purchased at various grocery stores, convenience stores, drug stores and department stores, as well as locations that deal in check cashing and money order issuing as a primary line of business. If you want to know whether your local retail store offers money orders, check with the customer service desk.

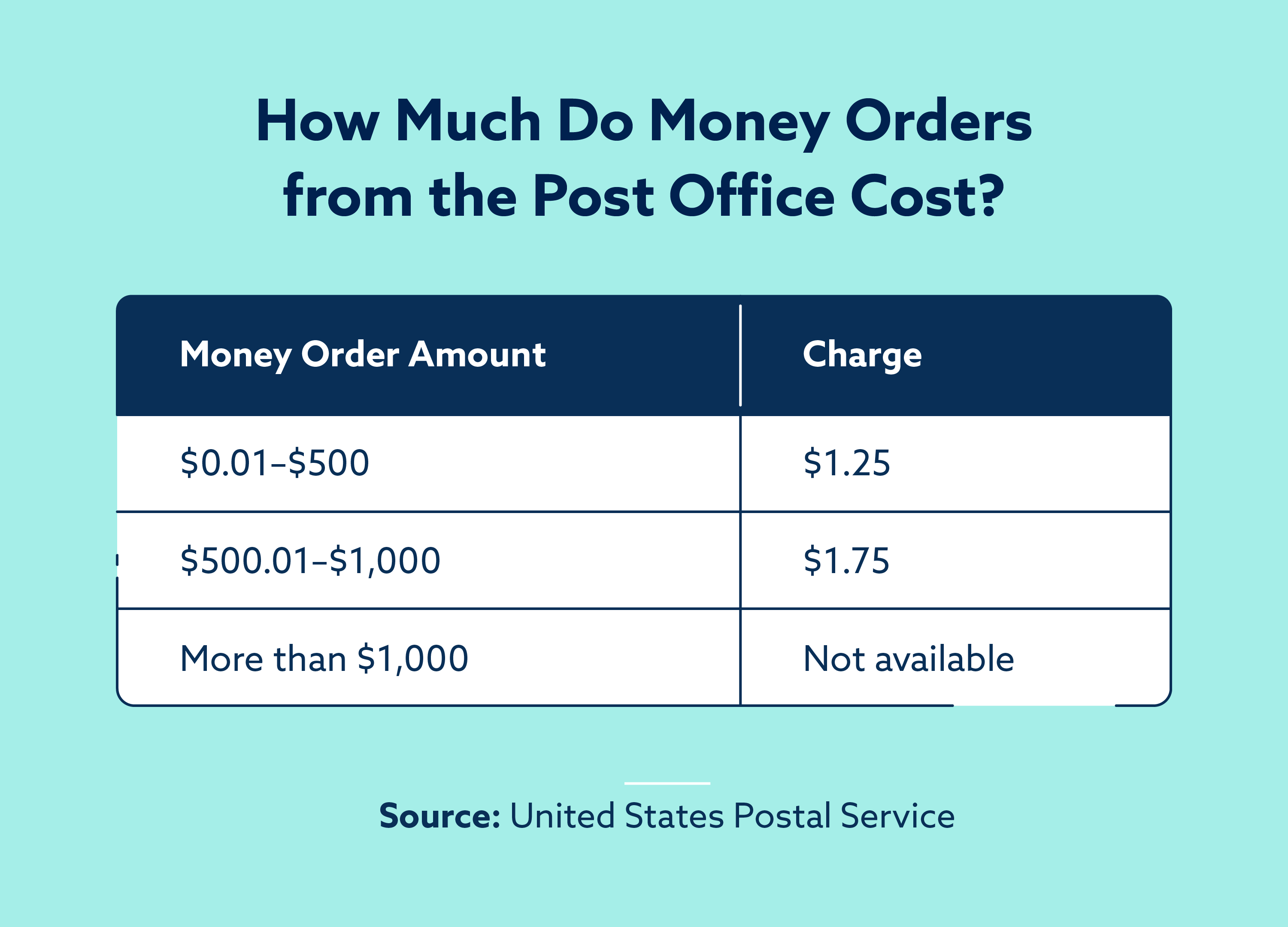

How Much Do Money Orders Cost?

When you buy a money order, you must cover the amount you want the order for as well as a fee for the service provider. Fees often depend on how much the money order is for. For example, the United States Postal Service charges $1.25 for a money order between $0.01 and $500. It charges $1.75 for a money order between $500.01 and $1,000. You can’t buy a money order for more than $1,000 from the USPS.

Retailers may charge more or less than the USPS for money orders. Walmart, for example, charges a maximum fee of $0.88. Banks tend to be the most expensive location for purchasing a money order, charging up to $5 or more.

Where Can I Cash Money Orders?

You can cash a money order made out to you at a number of locations. Often the first choice for many people is to cash the money order at their own bank or they deposit the money order into their checking or savings account. The funds are securely deposited, and you don’t have to pay a fee becausethe bank treats it much like you’re depositing someone else’s check.

You might also be able to cash a money order at any location that offers money orders, including the post office. Check-cashing locations, grocery store customer service counters and money transfer businesses such as Western Union might also let you cash a money order. However, in these instances, you might have to pay a small fee as you would when cashing a personal check.

How Long Do Money Orders Last?

Money orders don’t expire, but if you wait too long, you might end up paying a fee when you get around to cashing or depositing one. It depends on where the money order came from, and you should be able to discover these details in the fine print on the back of the money order.

The USPS says that its domestic money orders never expire or accrue interest. It says USPS money orders can be cashed at a post office location for the face value without any fee. In contrast, Western Union notes that its money orders don’t expire, but after one to three years, a service charge will be deducted from the principal amount.

Are Money Orders Secure?

Money orders are more secure than cash—that’s why people use them They are more secure because they are written to a specific entity. That entity must sign the money order and show ID when depositing or cashing it. While it’s not impossible that a money order could be stolen and cashed fraudulently, cash is still much easier to steal.

How Is a Money Order Different From a Cashier’s Check?

A cashier’s check is an official check that comes from a bank, and you typically must have a bank account with the bank in question. Money is moved from your personal account into an account owned by the bank. The bank then creates a check drawn on that account for the amount in question.

Cashier’s checks are a bit more secure than money orders. And since the bank has already verified you have the money and pulled it into a special account for this purpose, the payment is guaranteed to the other party.

When Should I Use a Money Order?

You can use a money order when you want to make a secure payment without including your personal account information. For example, if you’re paying a debt collector and you don’t want them to have access to your checking account information for potential future garnishment, you might pay with a money order.

You might also use a money order if you want to pay bills via mail without opening a checking account or if the person or business you’re paying has requested a guaranteed form of payment. Not everyone takes a check, and if you have previously bounced a check to a business, they might not be willing to accept a check from you again. The bottom line is this: If you’re looking for other ways to securely make payments, money orders might be a good option for you to consider.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.