The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Money is seen as a taboo subject amongst many Americans. Though money can be difficult and sensitive to discuss, having open conversations with your children can help them develop a healthy relationship with money—especially from a young age.

Research from behavior experts at the University of Cambridge found that children learn and develop money behaviors by seven years old. While they may learn simple money basics in school, the principles and relationships they develop around money start at home.

Though it’s a sensitive topic, more parents are starting to understand the importance of teaching their children financial literacy early on. According to a study from My Bank Tracker, 82 percent of parents plan to teach their children about personal finance at home.

In this guide, we’ll break down the impact poor credit and money habits can have on a child’s future, as well as tips on how parents can break generational habits and teach their children to have a healthy relationship with money from an early age.

How parents’ bad credit can impact a child’s future

A strong and healthy relationship with money can have a significant impact on how a child manages their finances over their lifetime. Unfortunately, many parents weren’t taught financial literacy at home, making them unaware of its importance in their children’s lives. A CreditCards.com survey revealed that one in four adults never learned any money lessons from their parents growing up.

Though parents may not notice, children pick up on how they handle money, which can lead to a child developing poor habits later in life. Factors like overspending on a child or never openly talking about finances can all inadvertently affect how your child grows up viewing money. Below are some unhealthy money and spending habits that can impact children:

Living beyond your means and accumulating credit card debt

The 2020 Parents, Kids and Money survey conducted by T. Rowe Price found that 53 percent of parents admitted to having a “keeping up with the Joneses” lifestyle. This is a term used to describe those who are always attempting to outdo their peers, which in terms of finances, often translates to spending beyond your means.

The study found that of those living this kind of lifestyle, 59 percent rely on credit cards to cover their monthly expenses. Abusing credit cards and living beyond what you can afford can give a child the false impression that you can spend as you please. If children see you abusing money, they can pick up on these habits and eventually fall victim to credit card debt.

Overspending on unnecessary things

One major factor in children developing poor money skills is seeing their parents overspend. Many parents want something different for their children than what they had in life. This could mean that since a parent grew up in poverty, they never want their child to face that hardship.

To combat this, they may spoil and overspend on their child. While their intentions are good, your child can grow up assuming that they will always be given what they want.

When a child reaches adulthood and goes off into the real world, they may quickly realize that the financial luxury they once had in their childhood might not be feasible as an adult. This could lead them to live beyond their means, which can ultimately lead them to accumulate large amounts of debt.

Speaking negatively about money or a job

From a young age, children develop the understanding that money is earned by having a job. The way a parent views and speaks about money and their job around their children has a direct impact on how they will grow up viewing money. Children are sponges and they pick up on what their parents say and feel, even if we don’t notice. This makes what we say and how we say it important, especially in a child’s early years.

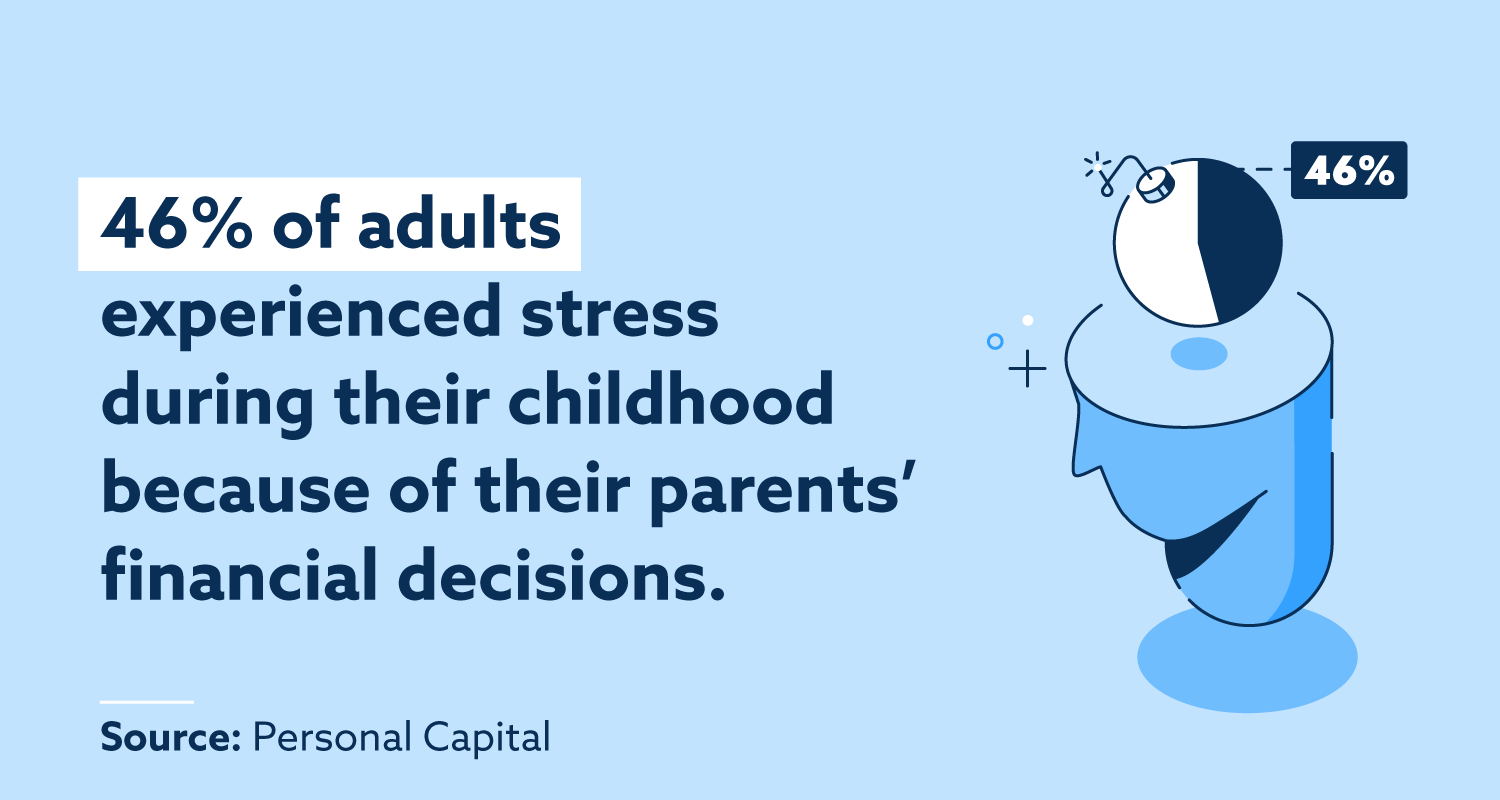

A study from Personal Capital found that about 46 percent of adults experienced stress during their childhood due to their parent’s financial decisions.

For example, if a parent is always openly expressing their frustrations around money and bills, a child can pick up on that, leading to them developing that same type of behavior.

Avoiding speaking with kids about money

There’s a common assumption that talking about money isn’t the polite thing to do, but that rule is one that can be put in the past. Though you may be reluctant, keeping your children in the dark can be misleading and cause more problems down the line.

If children bring up money and parents lie or avoid the conversation, it can lead to feelings of insecurity around the topic, which can fester into adulthood. On the other hand, some parents may think waiting until a child is at an appropriate age is the best strategy, but children will start developing their own view of wealth and money whether you’re the one to tell them or not.

Letting finances cause family conflict

Allowing finances to cause strain on your family can inflict fear on your children. Money is often at the root of a lot of family issues, which can only cause harm to children as they continue to grow up. If they observe a disconnect in their family dynamic caused by money, they will develop an understanding that money causes problems.

This, in turn, can lead to them developing poor money skills and a negative relationship with money and credit as they enter adulthood. Poor money management often leads to accumulating debt and careless spending.

8 tips for teaching your child about financial success

To teach children how to be financially independent and successful throughout life, it starts at home. Below we’ll break down strategies parents can take to help their child understand money and credit from early childhood to the start of adulthood.

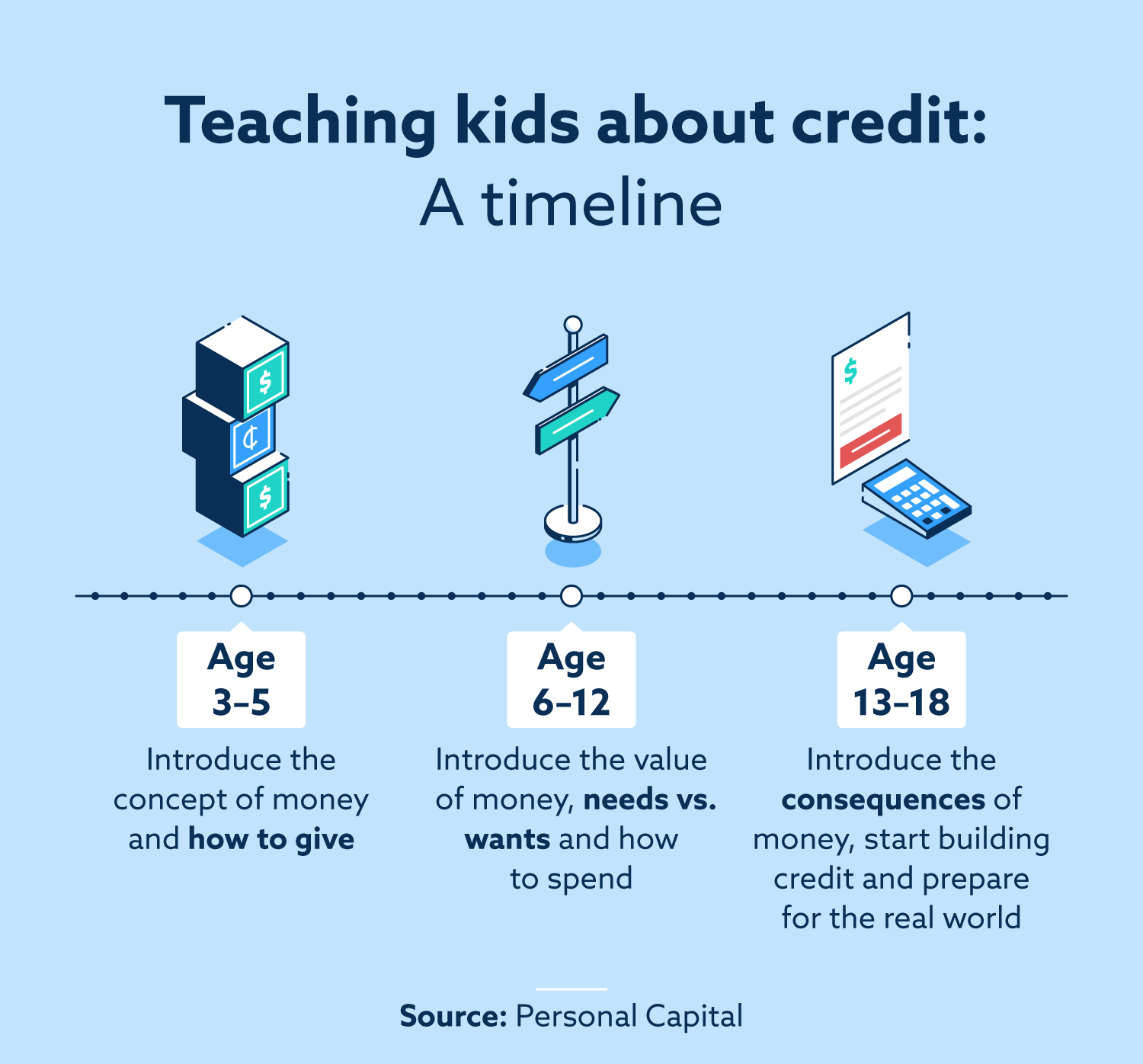

1. Teach them about credit early

Credit is one of the most crucial lessons a child can learn to prepare them for a financially successful future, and believe it or not, teaching your child about credit can start as early as preschool ages. From a young age, children start to develop an understanding of credit by observing their parents’ actions. For example, they see you swipe your credit card at the grocery store and develop the understanding that you can buy goods using that card.

It can be difficult to explain the concept of credit to a child at an early age, but you’d be surprised how much they catch on, even as early as three years old. To teach them about credit, you can start by having them exchange goods around the house with play money or credit cards. This can help them develop an understanding that goods can be traded for money.

Around age seven is when kids can really start to develop an understanding of credit basics and how money works, aside from just swiping a card. This is where you can teach them the difference between a debit card and a credit card—using a debit card is like using cash, while a credit card is using borrowed money that will have to be paid back.

As children grow and start to learn more credit basics, they can apply their learnings in the real world. If you want to help build your child’s credit early on, consider adding your child as an authorized user on a credit card.

Some banks offer this as an option around age 16. Of course, as a parent, you’ll have to closely monitor their spending habits, but this can set them up to have great credit health as they enter adulthood.

Though this can come with risks, it can help teach your child how to use credit, how to make monthly credit card payments and how to be financially responsible with money. Fifty-three percent of parents who have given their child a credit card say they did so to help their child learn about money.

2. Start a conversation about finances

Gone are the days of thinking the topic of money is rude to discuss at the dinner table. You should be able to have open conversations with your children about important life decisions—and that includes money. Though it isn’t always easy, having discussions about finances, even when you’re in a bind, will help teach kids financial responsibility.

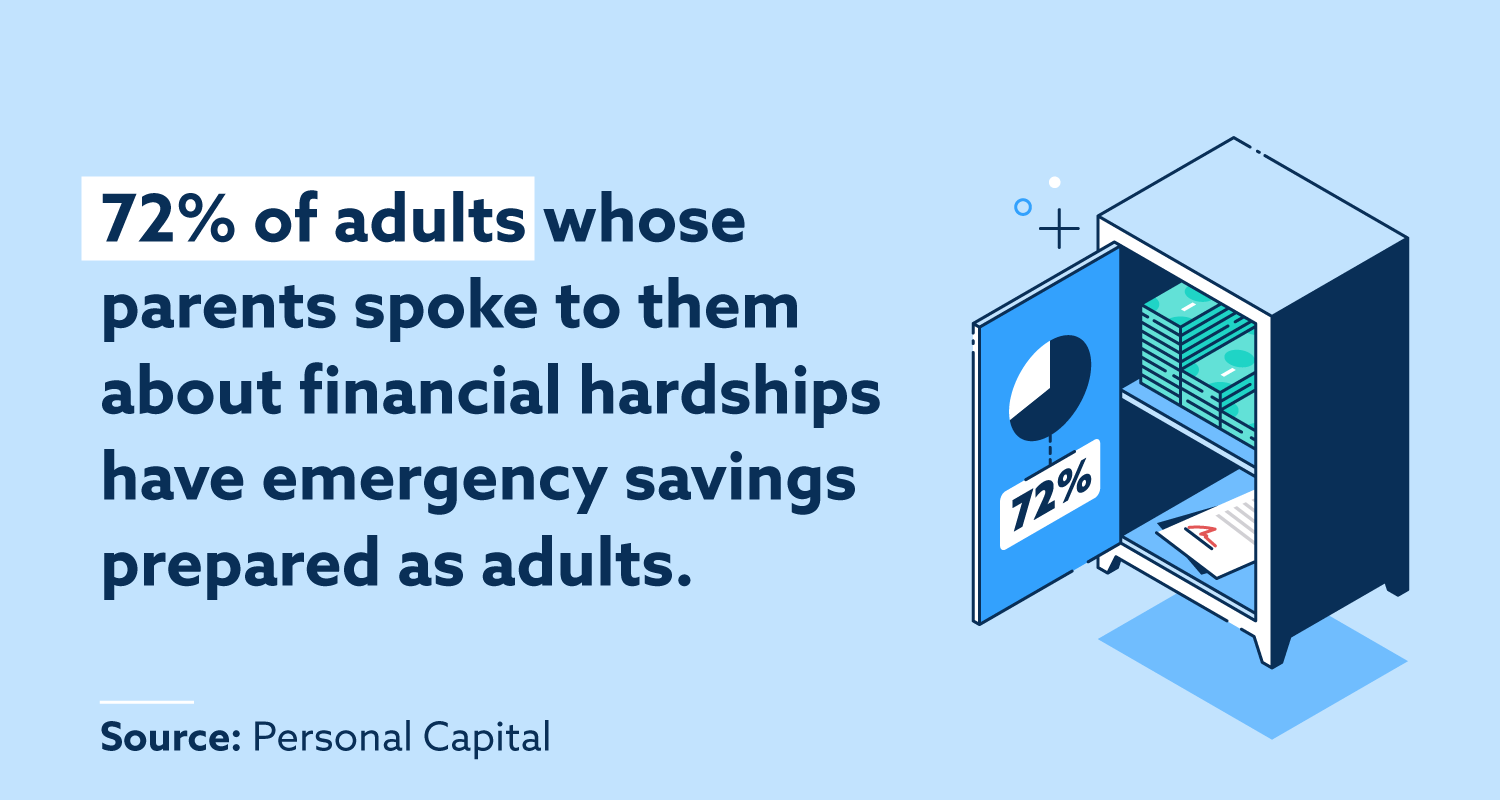

Personal Capital found that 72 percent of adults whose parents spoke to them about financial crises had emergency funds saved as an adult to better prepare for these hardships.

This doesn’t mean you should burden your children with the financial hardships you’re facing, rather use it as a way to teach them how they can handle these life lessons as an adult.

3. Turn it into a game

Gamifying money basics is an easy and fun way for kids, and parents, to learn financial literacy that will stick. Kids catch on to concepts faster when they enjoy what they’re learning about. There are many board games and online apps and resources that can help you teach your kids how to budget, spend and be responsible with their money.

One fun way to help teach them how to spend is to take them to the store and let them make their own purchases. This will help them learn financial independence and help them be comfortable with making purchases in the real world.

As your children continue to grow, learn ways to explain complex money topics in a way that’s fun and easy for them to digest—like explaining the stock market using pizza.

4. Practice what you preach

If you’re committed to helping your child develop financial literacy, you need to put the same energy into your own financial health. As a parent, your money habits have a huge influence on your child. Aside from teaching them, you need to model these habits too.

That means making sure your credit card bills are paid on time and you’re not falling behind on payments, you’re open and honest about money in your family and you know how to prioritize your needs versus wants. Having your child see you implementing these healthy money habits will help demonstrate your positive attitude towards finances, which they will learn to develop themselves.

5. Teach them about work ethic

Work and money go hand in hand, and teaching your child a strong work ethic early on can help them develop good habits around earning and spending money. To do this, start small by having them do tasks and chores around the house to earn an allowance or reward.

Work ethic can also be taught during school. School can be treated as a child’s job, and to earn what they want, they need to push themselves to do well. As they get older, they’ll start to develop a strong work ethic, which can be helpful when they’re able to get their first job in the real world.

It’s important to teach them that work ethic isn’t just about working to earn money—it’s also about developing trustworthy and responsible characteristics that will help them succeed in all areas of their lives, including finances.

6. Let them earn their own money

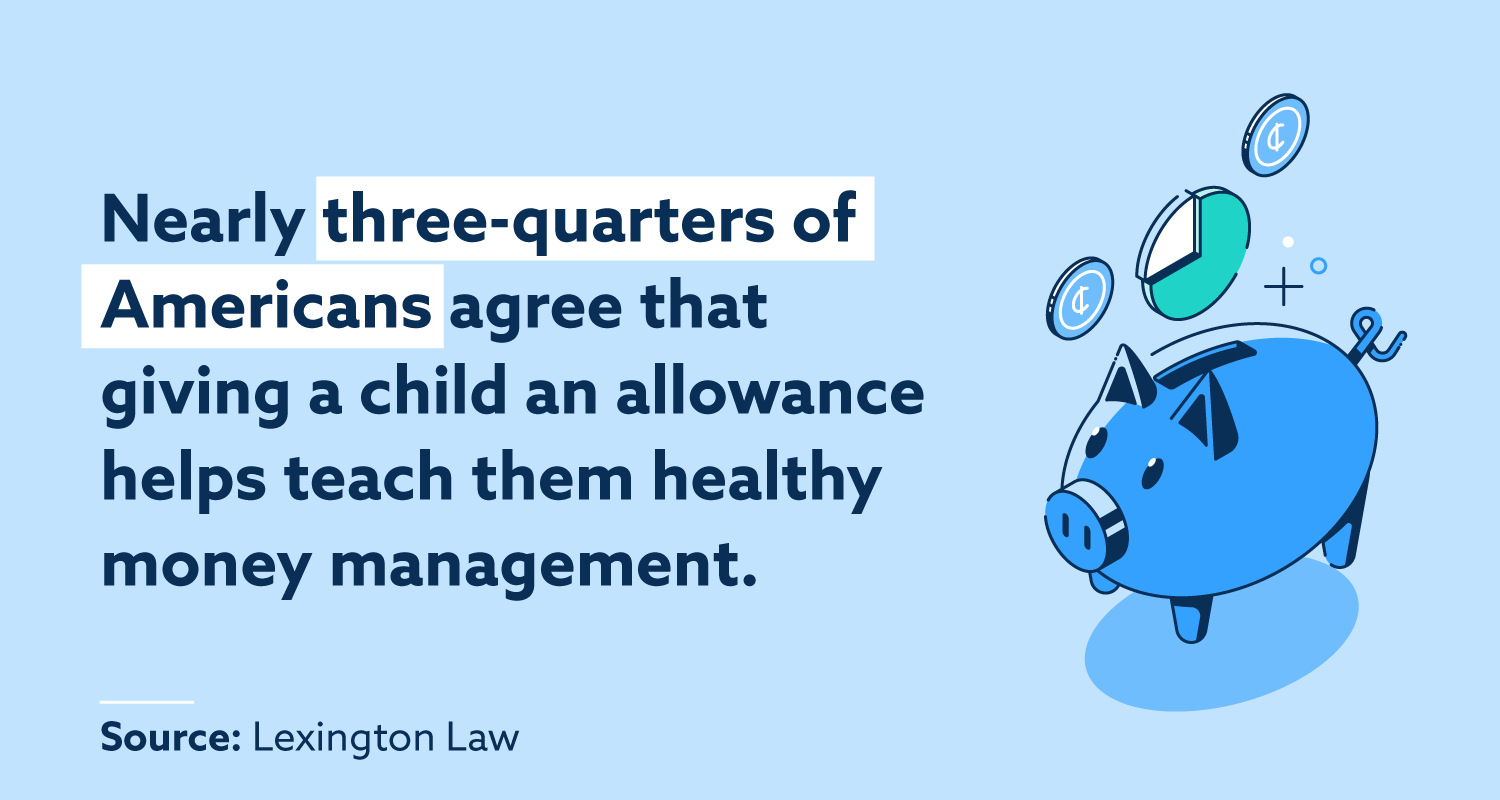

A survey we conducted found that three-quarters of Americans agree that giving children an allowance teaches them healthy money management.

Cleaning their room, doing the dishes and taking out the trash can all be simple chores they can do to earn their allowance. Having them do these tasks and earn money can teach them the general concept that money is earned, not given.

7. Help them budget and set savings goals

Saving habits take a while to build, even as an adult, but developing good saving habits early on can set your child up for success as they grow into adulthood. This is a good time to teach them about wants versus needs. Help them understand the necessities of life—food, clothing and shelter—versus the extra things we want but don’t need.

If there is something they want, let’s say a new toy or gaming system, help them set up a savings goal and budget to determine how they can reach their goal. Give them an example of how you budget your needs and wants so they know exactly how it works, then let them create their own budget.

Since they won’t have many expenses to account for, make their needs small, like having enough money saved to buy an after school snack. That way they can budget out necessary expenses and keep the rest of their earnings saved away.

Piggy banks are a tried and true method to start building your child’s saving habits early on. Have your child add to their piggy bank regularly, or as they get older, consider opening their own checking or savings account.

By teaching them the fundamentals of budgeting and saving, they’ll be better prepared to tackle handling their expenses in adulthood—like making their credit card payments on time.

8. Let them learn from their mistakes

As children get older they’re going to make mistakes, so let them. Though you may feel the need to control what they do, especially when it comes to money, letting them make mistakes can help them develop healthy habits so they don’t make those same mistakes again.

Maybe they wanted to save their money for a new toy but ended up wanting to spend it all on candy instead. In this case, allow them to do it. They may end up disappointed that they spent all of their money on something they didn’t need, but it’ll help them understand and appreciate the value of saving. When it comes to their own money, they’ll learn to change their spending habits.

Remember, the end goal is to prepare your kids to be financially independent and responsible. Just because you or your parents made some financial mistakes, it doesn’t mean your child has to follow in your footsteps. Ending the generational impacts of bad money habits and learning how to manage your credit can help you, and your child, have a successful financial future.

Additional resources for parents

Raising financially successful children involves teaching them important responsibilities around money. From budgeting and saving, to credit cards and bills, giving them knowledge on money from an early age will help them grow into financially responsible adults. Below are resources that can help you and your child learn more:

- CFBP: Money as You Grow

- Rooster Money: Allowance Tracking

- USMint.gov: H.I.P. Pocket Change

- Practical Money Skills

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.