The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Successful borrowing requires you to understand how your loan works, and interest is a huge part of any loan. Simple interest loans are one of the three most-common types of loans—the other type of loans are compound and precomputed interest loans. Discover more about simple interest loans, how they work and whether you might want one here.

What Is a Simple Interest Loan?

Simple interest loans follow an easy formula for calculating interest. The interest is only calculated on the principal amount you owe.

That’s in contrast to a compound interest loan. With that loan type, the interest is compounded into the principal and the entire amount is used to calculate interest going forward. That means if you’re not paying enough each month on the debt, your interest expenses could be getting higher and higher.

In a precomputed interest loan, the total interest is calculated one time at the beginning of the loan. The total balance—principal plus interest plus any fees—is added together and divided into the terms of the loan to find out how much you pay per month. For example, if you borrow $1,000, the interest is $150 and the fees are $25, then you would owe $1,175. If you took the loan out for a single year, that would be $97.92 per month.

Types of Loans That Use Simple Interest

Simple interest is used in a variety of loan products, including both vehicle and student loans. Personal loans and other short-term lending products might also use simple interest, and there are even simple interest mortgage loans that calculate interest daily.

It’s always important to make sure that you know what type of interest is being calculated on your loans because it impacts how much you might owe and how you might manage the loan in the future.

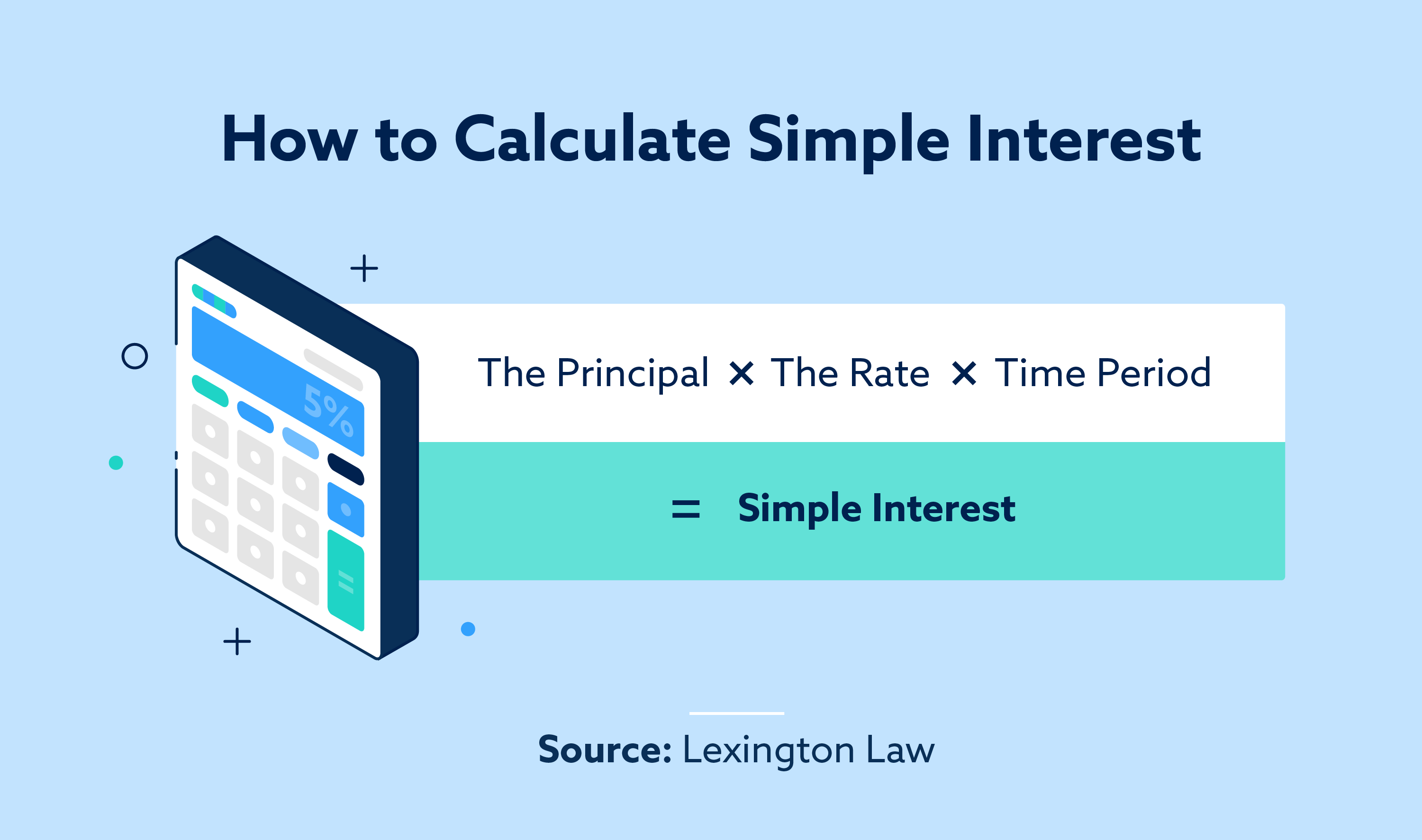

How to Calculate Simple Interest on a Loan

Simple interest is always calculated using the same formula:

Simple Interest = the principal * the rate * time period

For example, if you borrow $3,000 at a rate of nine percent interest for a period of three years, the math would look like this:

3,000 * 0.09 * 3 = $810

But you don’t pay that total interest right away. Your monthly payments would be around $105.83, and around $22.50 of your first payment would go toward interest. The rest—around $83.33—would be deducted from your principal amount due.

For your second payment, the formula would like this:

2,916.67 * 0.09 * 3 = $787.50

The principal has been reduced by your previous payment, so the total interest calculated is less. That means roughly $21.87 of the second payment would go toward interest, and $83.96 would go toward principal.

It’s a small change, but that change continues. By the time you make your twelfth payment, the principal is $2,048.11. Your monthly payment is still $105.83, but only roughly $15.36 of that goes toward interest and more than $90 goes toward principal.

Benefits of Simple Interest Loans

When the rates are the same, simple interest loans are typically less costly than compound interest loans. That’s because in a compound interest loan, your interest is compounded into the principal, so your rate is multiplied by a slightly larger number every month.

Simple interest loans also offer a potential savings option for those who can pay early. This works when interest is calculated on the loan daily, as is the case with many short-term loans and even some auto loans. Since interest is calculated daily, if you make your payment 15 days early every cycle, you get 15 days where your daily interest is calculated on a lower principal amount. Those savings can add up.

Are There Any Drawbacks to Simple Interest Loans?

The opposite is true, though. If you make late payments, you’re being charged interest on a larger-than-expected principal during the time when your payment is late. If you’re regularly late with your payments, that can add up to a month or more of extra payments on the end of your loan.

How to Pay Off a Simple Interest Loan Faster

The biggest benefit of a simple interest loan is that you can pay it off faster if you can put a little extra money on it. Here are three ways to pay off your simple interest loan before your scheduled terms.

Pay More Than the Minimum

Add a little more to your loan payment every month. If your payment is $235, pay a flat $250. Just make sure that you designate that the extra money is meant to go toward the principal.

Pay Earlier Rather Than Later

As previously discussed, paying earlier in a loan cycle can help reduce the total amount of interest you owe over time. This typically only works when interest is calculated daily.

Pay More Often Than Necessary

Make more than one payment a month. If your payment is $100 a month, make two $100 payments every month. Make sure you note that you’re not paying your regular payment early and that you want the full $100 of the second payment to go toward principal.

Always Double-Check Your Loan Terms

Before you try to pay down a loan early, make sure you understand your loan terms. You should make sure that you have a simple interest loan. If you find that you have a precomputed interest loan, paying early in the cycle does nothing to help you pay it off early. Additionally, some lenders include early payment penalties to ensure they don’t lose interest income if someone decides to pay a loan early. The bottom line for managing any type of loan is to understand your loan terms. Make sure you read them before you sign and pay attention to them during the life of the loan because they can help you save money or avoid extra expense.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.