The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

According to PricewaterhouseCoopers, average revenues from 2018 to 2019 for businesses were up 10 percent, but many companies still struggled to convert those higher revenues to cash. When a business doesn’t have the cash flow to support daily or growth expenses for any reason, working capital loans might be an option. Find out more about working capital below to help you decide if this funding source is right for your company

What Is a Working Capital Loan?

Working capital loans are a type of funding that helps ensure businesses have the capital they need to continue operating during periods when it might be difficult to cover daily expenses while meeting new demands or growth. For example, if a business has tied up its cash flow in inventory for the holiday rush season, working capital funds can pay the bills—such as employee wages and rent—until holiday revenues are in.

It’s important to note that working capital isn’t meant to make investments or buy long-term assets such as equipment. If you need equipment, you may need to take out a secured loan for it. Working capital loans are meant to cover the standard operating expenses of the business such as regular debt payments, wages, rent and utilities.

Working Capital Financing Options

You can get working capital loans from a variety of sources. Some of the most common options are summarized below.

Short-Term Loan

What is it? You might be able to borrow money for a few months to help fund expenses until seasonal income comes in or a large invoice is paid.

Pros: It might be a good way to balance cash flow during seasonal upticks in expenses or downturns in income.

Cons: Because the terms of the loan are short, the lender may charge a relatively large fee to make money from the deal in lieu of interest paid out over a longer period of time.

Merchant Cash Advance

What is it? A cash advance offered by the bank or agency that handles your payment processes. For example, businesses that accept money through PayPal may be eligible for a Payment Working Capital loan.

Pros: These loans are typically easy to get if you have a solid history processing payments through that bank or agency. That’s because the loan isn’t based on your personal credit or the credit of your business. It’s typically based on how much average revenue you process through that payment method.

Cons: Typically, merchant cash advances are paid back as a percentage of your sales over time. That lowers your cash flow for the immediate future and can make it more difficult to budget for business expenses if you overcommit on the loan.

Bank Line of Credit

What is it? A revolving line of credit that you can draw from and pay back and then draw from again—similar to a credit card.

Pros: A line of credit is flexible and ongoing, which means it’s there when you need it, but you don’t have to draw on it if you don’t need to. It can also be a good way to balance cash flow if your revenue tends to fluctuate.

Cons: You may need decent personal or business credit to get approved for a line of credit. It can also be tempting to rely too heavily on it, temporarily masking serious financial problems until they might be too late to resolve.

SBA Loan

What is it? You can get certain types of loans through programs approved by the Small Business Administration. Some of these loans can be used for working capital.

Pros: While the terms and rates associated with SBA loans vary, they may be more favorable than those of traditional loans.

Cons: SBA loans can be easier to qualify for from a credit perspective, but they do have specific requirements, such as documentation. You may also be limited on what you can use the funds for.

Trade Credit

What is it? Trade credit occurs when you purchase goods on an account and pay for them later. Typically, if you pay within the agreed-upon period, you don’t pay interest on this debt.

Pros: Trade credit is low-cost and is generally a common business practice, which means it might be available to you from various vendors.

Cons: This isn’t a form of credit you can use to cover expenses other than goods purchased, but that might free up some cash for other uses.

Who Offers Working Capital Loans?

Working capital loans are offered by a variety of organizations. Banks, credit card companies and payment networks might all offer working capital loans. Some organizations specialize in this type of lending and work with businesses that can demonstrate a strong historic revenue to provide working capital loans or lines of credit.

Working Capital Loan Interest Rates and Fees

As with any type of lending, working capital loans do cost your business in the form of interest rates and fees. With a few exceptions, such as certain trade credit arrangements, working capital comes with varied rates and costs. If the lender makes money via interest, your own credit or the creditworthiness of the business may be used to determine how much interest is charged.

Some working capital loans don’t include interest. The lender instead charges a flat fee that is incorporated into the total amount paid back during the loan process.

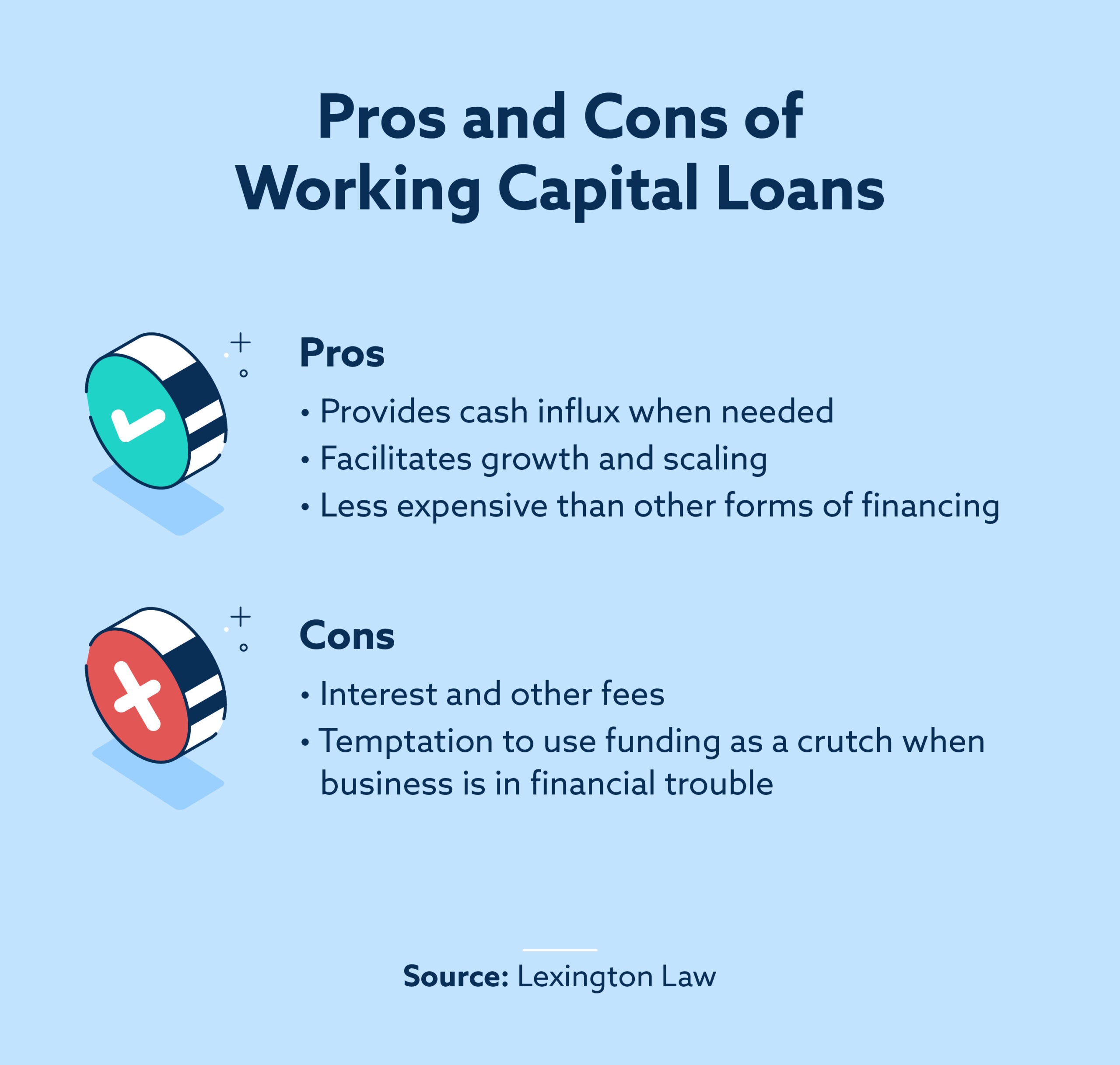

Is a Working Capital Loan Right for Your Business?

As with any form of debt, working capital loans have benefits and disadvantages. Understanding the common pros and cons can help you determine whether working capital loans are a good decision for your business.

Benefits

Working capital can provide the cash influx you need at just the right time. It’s a financial tool for helping businesses cover costs during various seasons or scale up for growth. If you’re careful about how you use the credit associated with working capital loans, they may not be as expensive as some other forms of financing.

Drawbacks

Working capital loans come with some of the same drawbacks of any debt, including interest or other costs. But a bigger potential disadvantage is the temptation to lean heavily on working capital even when you know that your business is in trouble financially. Working capital is meant to be a temporary bridge, not a crutch your business can lean on permanently.

Other Options for Increasing Your Work Capital

Working capital is a measurement of how well a company can use its current assets to pay its current liabilities. It’s an important statistic for you to be aware of as a business owner, because it indicates how financially healthy your company is. If you need to improve your working capital but don’t want to receive financing from a third party, consider these other ways to increase your working capital:

- Cutting business expenses, including unnecessary travel or acquisitions.

- Increasing income by hosting a sale or increasing prices if the market will support it.

- Collecting past-due invoices.

- Selling valuable business assets that may not be required at this time.

As you weigh your different options for working capital financing, don’t forget to stay on top of your business credit score and your personal credit score, too. To learn more about the latter, check out Lexington Law’s guide to credit.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.