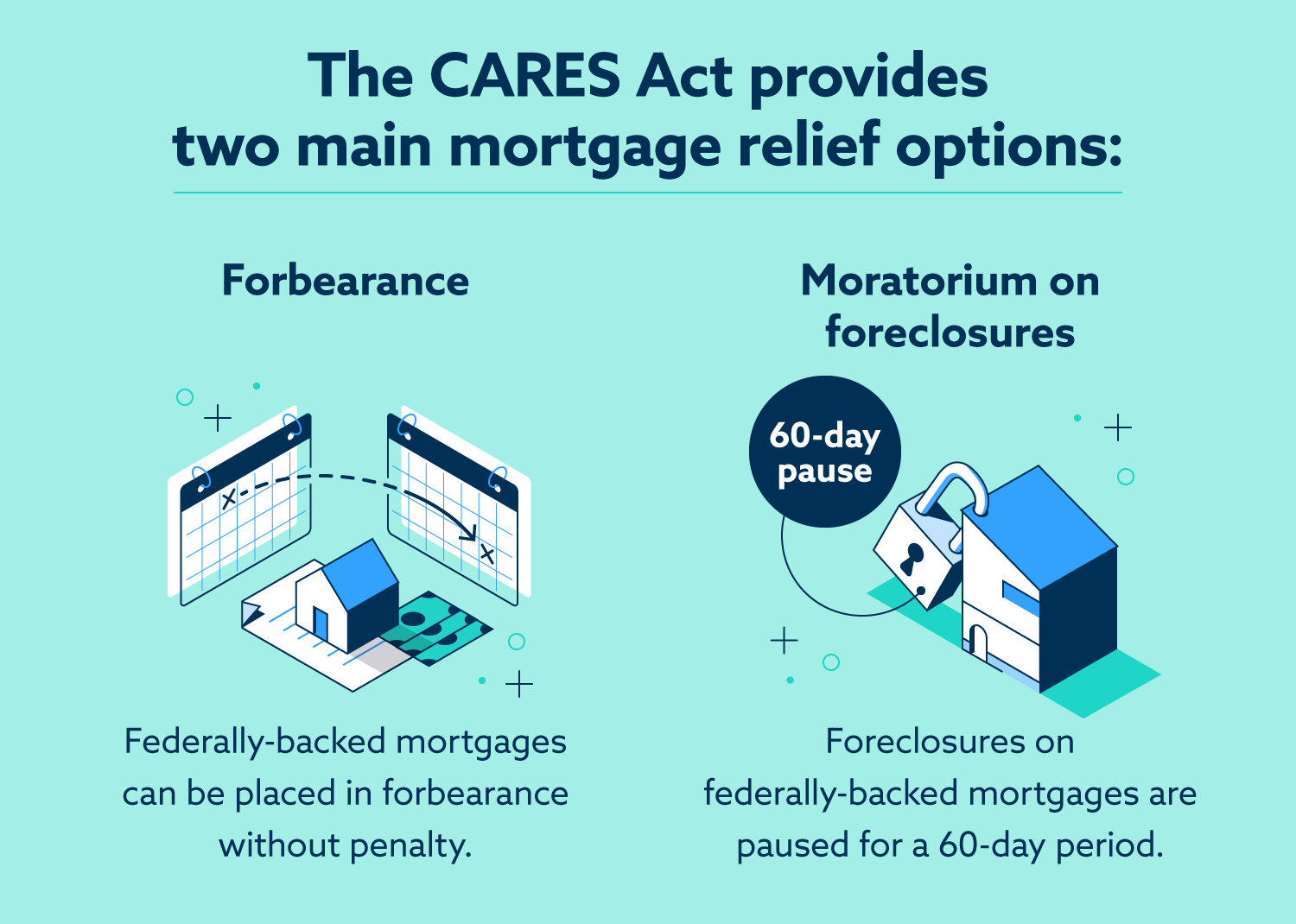

The CARES Act provides two main mortgage relief options: forbearance and moratorium on foreclosures.

If you’re a homeowner with a federally backed mortgage who is struggling financially during the coronavirus outbreak, you should know the Coronavirus Aid, Relief and Economic Security (CARES) Act offers mortgage relief in the form of a foreclosure moratorium as well as options for placing your mortgage in forbearance.

Following the outbreak, many people are unemployed or otherwise struggling financially. One of the most difficult monthly obligations to manage is a mortgage payment. Especially when mortgage terms include a high monthly payment, even one month of unemployment or financial hardship can put borrowers behind on their home loan.

Thankfully, the CARES Act includes protections for homeowners with qualified mortgages, who are enduring financial trouble due to the coronavirus outbreak. Here we’ve broken down the coronavirus mortgage relief options available and detailed how homeowners can take advantage of them.

What are the two mortgage relief options?

The two mortgage relief options included in the CARES Act are mortgage forbearance and a moratorium on house foreclosures. Specifically, the CARES Act states that:

- Homeowners with federally backed mortgages who are experiencing financial hardship due to COVID-19 can request a 180-day forbearance on their mortgage, which can be extended another 180 days at the borrower’s request.

- Federally backed mortgage servicers cannot initiate a foreclosure, conduct a foreclosure hearing or execute a foreclosure sale or foreclosure-related eviction until May 18, 2020.

How to find out if you qualify for CARES Act mortgage relief

To find out if you’re eligible for the mortgage relief protections in the CARES Act, you need to determine if your mortgage is backed by a federal entity. You can figure this out by looking up your mortgage online, calling your mortgage servicer or sending a request in writing to determine who owns your mortgage.

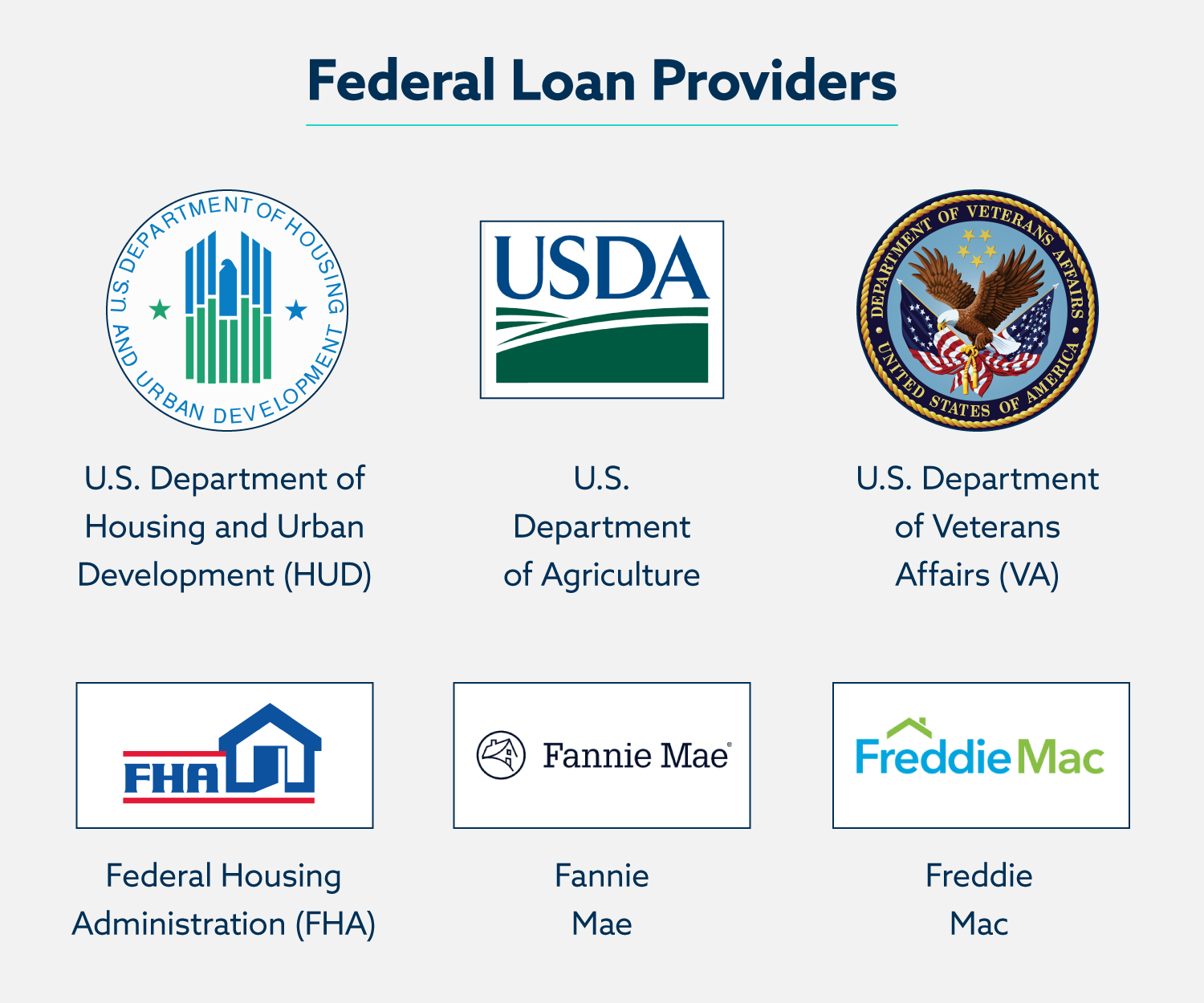

Nearly half of all mortgages in the United States are backed by Fannie Mae or Freddie Mac. You can use these look-up tools to determine if yours is one of them:

In addition to Fannie Mae and Freddie Mac, other federal agencies that back mortgages are:

- U.S. Department of Housing and Urban Development (HUD)

- U.S. Department of Agriculture (USDA)

- Federal Housing Administration (FHA)

- U.S. Department of Veterans Affairs (VA)

How to request a mortgage forbearance

The moratorium on foreclosure procedures is automatic for those with federally backed mortgage loans. If you have a federally backed mortgage and your home was in the process of or about to enter foreclosure, you can anticipate that those proceedings will be halted until May 18, 2020. During this time, you can contact your servicer to inquire about getting a forbearance, instead. It is important to contact your mortgage servicer to make sure your foreclosure proceedings have been halted.

If you decide you need to request a forbearance, these are the steps to take:

1. Gather the relevant information.

You’re going to need several pieces of information during the process of requesting mortgage relief, so it’s best to gather them ahead of time. Be prepared to provide:

- Your loan account number

- The cause of your financial hardship and its relationship to the Coronavirus (COVID-19) outbreak

- How long you expect the hardship to endure

- Personal financial details, like income, unemployment benefits, expenses and your current assets

These are the basic details you should have on hand, but individual loan servicers may have other recommended requirements. You should check your individual provider’s website to be certain.

If you’re in the military and currently on orders, you’ll want to let your servicer know that as well.

2. Call your mortgage servicer.

Keep in mind that your mortgage servicer is not the same as the entity that owns or backs your loan. Typically, a bank or mortgage broker will act as your loan provider, and (in the case of federally backed loans), the entity that owns the loan will be a federal organization like Freddie Mac or the United States Department of Agriculture.

To request mortgage relief, you need to contact your loan servicer. Their contact information should be included in your monthly mortgage statement.

During the Coronavirus (COVID-19) crisis, you should anticipate a long hold period when you call your servicer. Since mortgage relief requests are currently at a peak, it will likely take longer to reach your provider.

3. Ask for the help you need.

Once you’re connected with a representative from your loan provider, ask for the mortgage relief you need. Since different states and individual loan providers may offer additional relief options besides those explicitly included in the federal CARES Act, you should begin by simply asking what mortgage relief options are available to you.

In addition to forbearance, which is mandated for federally backed loans, your servicer may offer loan modification options or waive your late fees.

Your servicer will likely ask for information like what financial hardship you are experiencing, how long you expect to need relief, and the details of your current financial situation, which is why you should have this information readily available when you call.

In the process of this conversation, your servicer will let you know what your options are and what you need to do in order to activate them.

4. Follow up in writing.

Once you and your loan servicer have settled on a mortgage relief option that works for you, be sure to request a written document reflecting what you discussed and the details of your agreement’s terms. Be sure to clarify the end date of your forbearance period and what is required of you after the fact.

In some cases, you can resume monthly payments as usual, while some forbearance agreements require a lump sum payment at the end of the relief period. Be sure you’re prepared to satisfy the terms of your agreement exactly as they’re laid out.

What to do after receiving mortgage relief

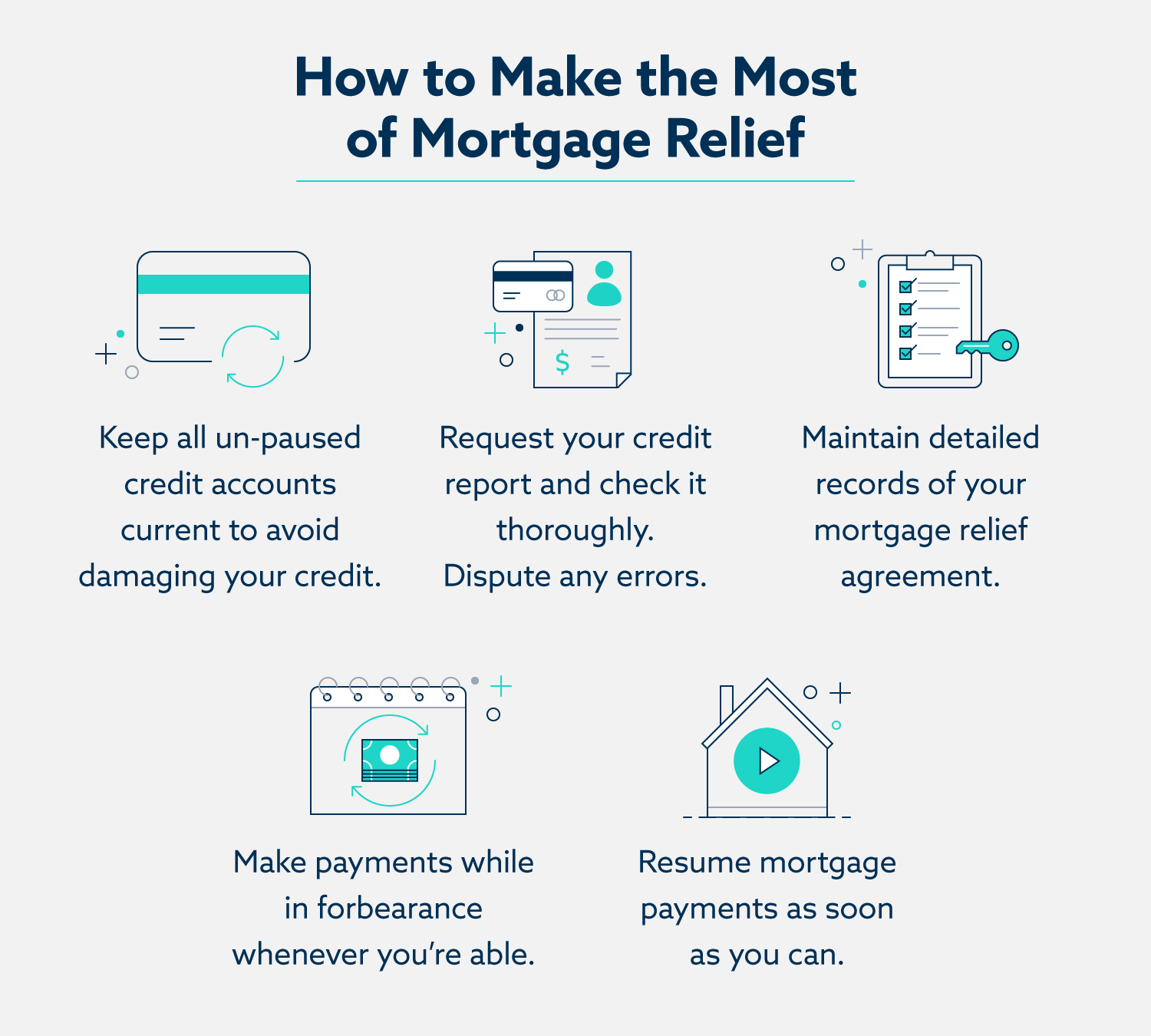

Even after being approved and receiving mortgage relief, it’s important to stay on top of your relief agreement and resume payments as soon as you’re able.

Here are best practices for moving forward after reaching a mortgage relief agreement:

- Work to protect your credit. Since missed mortgage payments without an approved forbearance will damage your credit, it’s important to ensure your servicer accurately recorded your forbearance agreement and your paused payments aren’t reflected on your credit. Now might be a good time to request one or more of your three free annual credit reports to check for and dispute errors.

- Keep paying other expenses. The CARES Act contains many options for putting off monthly payments without penalty, so it’s essential that you continue to stay on top of your other bills, if you’re able. Mortgage relief can protect your credit, but only if you’re not delinquent on your other accounts during this time.

- Keep an eye on your mortgage. Keep the paperwork from your forbearance agreement on record and continue to review your monthly statements as thoroughly as you would if you were making payments. If you spot an error, dispute it immediately.

- If you have extra cash flow, consider making partial payments. If you’re working part-time or receiving unemployment benefits, you may find you have some extra income despite not being ready to resume regular mortgage payments. In this case, consider making partial mortgage payments even while your loan is in forbearance. You’re still going to owe the entirety of the loan later, so putting down extra now will lighten your financial load later on.

- Resume payments as soon as you’re able. If you resume work while your mortgage is in forbearance, be sure to contact your servicer to resume your mortgage payments right away. It can be tempting to let your payments remain paused, but a shorter forbearance period means less financial burden for the remainder of the loan.

How to find state-level mortgage relief options

Many states have passed coronavirus relief laws that expand on the protections included in the federal CARES Act. When investigating your financial relief options, be sure to look up protections offered at the federal, state and local levels. Individual mortgage servicers are also opting to offer their own accommodations, so you should inquire with your loan officer directly as well.

How to decide if you should ask for mortgage relief

Mortgage forbearance is available to anyone with a federally backed mortgage who has experienced a coronavirus-related financial hardship. If you fit these qualifications but are capable of paying your mortgage—whether through cash reserves or other personal resources—the best course of action is to continue making mortgage payments.

From a strictly ethical perspective, relief aid should be reserved for those who absolutely need it most. Mortgage servicers can only accommodate a certain number of relief requests at once, so it’s important that their resources be allocated to those who are most in need.

Beyond ethics, it’s also smartest strategically to continue paying your mortgage whenever possible. Pausing mortgage payments unnecessarily can make payments more difficult down the line, and you may not have the same mortgage relief options available in the future. When it comes to home loans, paying earlier is usually the better option when possible.

As you navigate the complicated world of financial relief during the coronavirus outbreak, keep in mind that many of the provisions in federal, state and local laws require the individual to proactively request relief. That means you need to know what benefits are available and how to access them rather than anticipating that relief will come to you. In fact, any relief options that do come to you directly may be scams, so be sure to vet all relief offers diligently before entering into an agreement.