Keeping track of your finances can be difficult, especially when you have several payments going in several different directions. If that sounds familiar, a debt consolidation loan could help.

Our guide will break down what you need to know about debt consolidation loans and help you decide whether or not they’re the best option for you.

What Are Debt Consolidation Loans?

Debt consolidation loans are used to combine multiple debts, such as credit cards, high-interest loans and medical bills, into an account with one monthly payment and lender. Debt consolidation loans are a type of personal loan.

Applying for and receiving a debt consolidation loan is a multi-step process that requires you to choose your loan terms, finalize your application and repay the loan.

Here are the steps you should take when applying for a debt consolidation loan:

- Meet preapproval terms. Preapproval terms will differ between lenders, but typically they request that you have at least a 580 credit score and no bankruptcies. A lender will perform a soft inquiry on your credit to see if you meet their requirements before quoting you a rate.

- Decide which credit card debts to pay off. Before choosing your loan terms, prioritize which of your credit cards you want to pay off first. This will dictate how much you borrow and the length of the loan.

- Finalize your application. Finalizing your application requires a hard inquiry on your credit report.

- Go through a closing process. If you’re approved, loans are disbursed either directly to your creditors or sent to you by check.

- Start paying off your debt.

There are two types of debt consolidation loans: secured and unsecured. Secured debt consolidation loans use collateral, such as home equity. While secured loans typically have better interest rates, they can be risky. You could face foreclosure if you can’t pay your debt.

Unsecured loans are more common and don’t require any collateral, but they typically have higher interest rates and are more expensive to pay down.

How Do I Qualify for a Consolidation Loan?

To qualify for a debt consolidation loan, you must meet lender requirements.

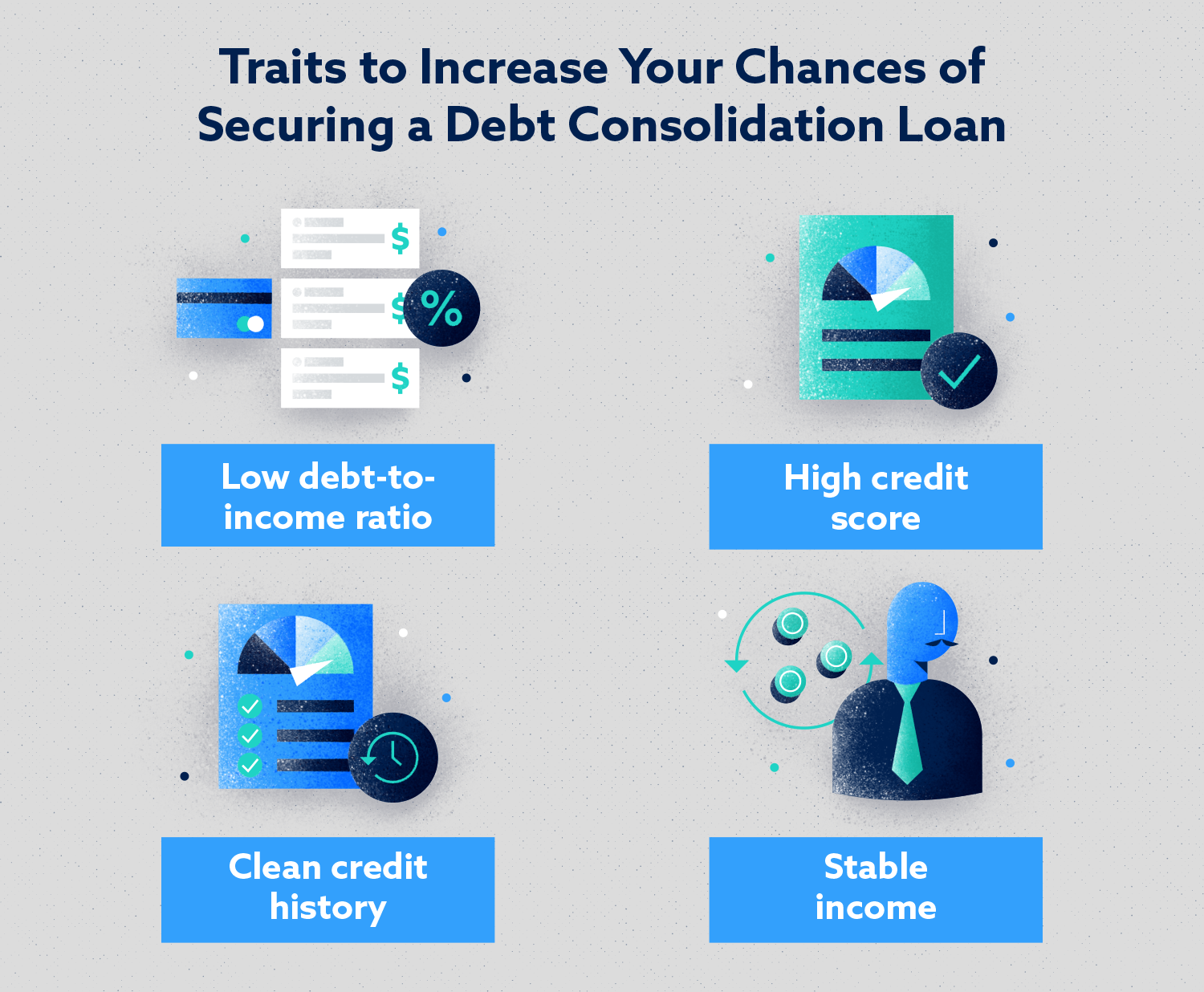

Lenders often use your credit score to determine your interest rate. Having a high credit score, a lower debt-to-income ratio and a stable income will increase your chances of securing a loan.

Can I get a Debt Consolidation Loan with Poor Credit?

Lenders view people with low credit scores as high risk, so it might be difficult to get approved for a debt consolidation loan if you have poor credit. Those with poor credit who are approved will end up paying higher interest rates.

If you have a low credit score, be cautious about taking out a debt consolidation loan. The interest rate on a debt consolidation loan could be higher than your existing debt, making it more expensive to pay down.

How to Choose the Right Loan

When choosing a debt consolidation company, compare loan terms and interest rates to see how much interest and how many fees you’ll pay overall. This can help you pick the loan option that saves you the most money.

Here’s what you should consider when evaluating a debt consolidation loan:

- Interest rates: Most lenders offer a fixed-rate loan, while some offer both fixed- and variable-rate loans.

- Loan terms and restrictions: Review the loan period length and loan amounts to see whether the amount and repayment timeline meet your needs.

- Fees and penalties: Look at the origination, prepayment and late fees, which can significantly increase the cost of your loan. Some lenders place restrictions on how you use the loan, such as prohibiting consolidations on student loan debt.

Is it a Good Idea to Get a Debt Consolidation Loan?

There are benefits to using a debt consolidation loan, but there are also potential disadvantages. Ultimately, it depends on your personal situation.

If you qualify for a new loan with favorable terms and a lower interest rate than your current debt, it could be a good idea. However, you need to consider your credit scores, income and ability to repay the loan.

Pros

- Debt consolidation loans can have lower interest rates than credit cards and other types of debt, depending on your credit range. If you qualify for a low-interest loan, you can reduce your current interest rate and save money on repayment.

- You can lock in a low rate with a fixed-rate debt consolidation loan instead of owing money at variable rates.

- A debt consolidation loan gives you a debt repayment timeline specified in your loan agreement, so you’ll know exactly when you’ll pay off the loan.

- You’ll have payments that are easier to handle if the loan lowers your monthly payments. This means that you’re less likely to be subject to additional fees and higher interest rates that come with missing a payment.

Cons

- People with low credit scores may only be given loans with a higher APR than their existing debt.

- You could wind up paying a lot more interest overall, depending on your loan’s interest rate. Although your monthly payment might be lower, your repayment term could be longer.

- A low-interest rate for a debt consolidation loan could just be a “teaser rate” that only lasts for a certain time. After that, your lender may increase the rate you have to pay.

- The loan may also include fees such as application fees, origination fees or prepayment penalties that you would not have to pay if you continued to pay back your current lenders.

- You put your house, car, retirement fund or other assets at risk when you use collateral to secure your loan. If you’re not able to pay your loan, you could face losing those assets.

- You could end up in more debt if you get a consolidation loan and keep making more purchases with credit.

What are Alternatives to Debt Consolidation?

If debt consolidation isn’t your best option, there are other ways to manage your debt.

- Credit cards with an introductory 0 percent APR balance transfer allow you to consolidate your debt on one credit card. Be aware: if you are more than 60 days late on a payment, you face a penalty APR on all balances, including the transferred balance. There’s also usually a balance transfer fee, either as a fixed amount or a percentage of the amount you transfer.

- Creating a budget can help you understand how much you can afford to pay each month toward existing debt.

- Responsible credit card usage can ensure you aren’t allowing your balances to get too high. If you’re spending more than you’re earning, consider adjusting the way you spend to pay off your existing debt.

- Bankruptcy may be an option if you are overwhelmed with debt and see no way to pay it off. However, a bankruptcy can remain on your credit report for up to ten years.

Do Consolidation Loans Hurt Your Credit Score?

A debt consolidation loan could actually help your credit score. If you have a high credit balance, consolidating could lower your utilization rate. Additionally, a lower payment each month could mean more on-time payments.

That being said, how your debt consolidation loan affects your credit score really depends on your ability to make your payments. Having monthly payments due on a loan, in addition to credit cards, could put you in an even more difficult situation.

Managing Multiple Payments, Debt Consolidation Loans and Your Credit Report

Many consumers turn to a debt consolidation loan because of the challenges they face keeping track of multiple accounts.

Mistakes can happen, but if payments are applied to the wrong account or your accounts are reported more than once, it could make you appear risky to lenders. Mistakes on your credit report can be costly and unfairly affect your credit score if they go unfixed.

Credit repair can be a hassle, especially if you are unfamiliar with the process. At Lexington Law, we do the heavy lifting to make the dispute process easier, by identifying and challenging questionable negative items on your behalf. Although we don’t manage debt consolidation loans directly, our team of credit report consultants can help you navigate the credit repair process.