The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

At the end of every monthly credit card statement, you’ll find text that outlines the terms of your agreement. This section defines the APR (annual percentage rate) and VR (variable rate) as well as the terms and conditions for using your card and more. For such “fine” print, it’s hardly light reading.

Important information about your credit line may be buried in the details. Consumers now have protections that shield them from unfair practices. For one, Congress introduced the Credit Card Accountability Responsibility and Disclosure Act of 2009 (the “Credit CARD Act”) to control how and when companies collect credit card fees, apply interest rates, and more. Still, it’s possible for consumers to miss or misinterpret the agreement’s terms and rate information.

To better inform consumers, we pulled information from the Consumer Financial Protection Bureau’s semi-annual survey of credit card plans. Are you really getting a deal with that zero-interest card? Read on to find out.

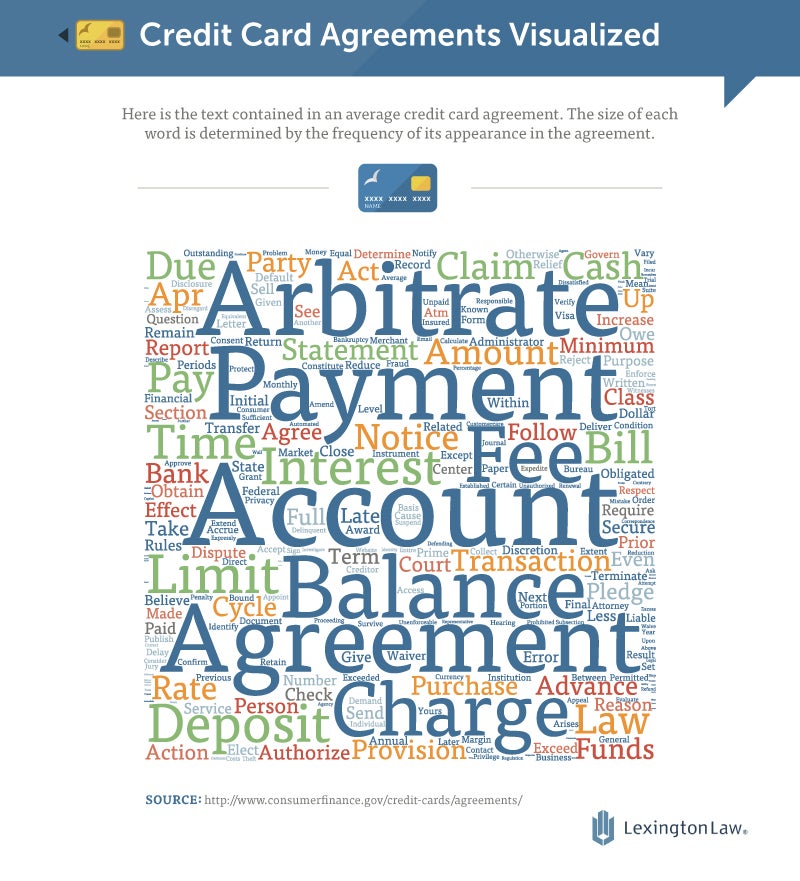

The Words in the Fine Print

The word cloud above represents the typical terms one might find in a credit card agreement. The larger the word, the higher its frequency. The standard conditions of any statement include BALANCE: the AMOUNT owed at the end of the billing period, including any past unpaid balance and any new PURCHASES; the FEES charged; the INTEREST charged for purchases and unpaid balances; as well as any CASH ADVANCES – the amount owed plus interest. (Cash advance annual interest rates are typically six percentage points higher than average credit card purchase interest rates.)

An annual membership fee anywhere from $9 to $99 may also apply. It’s important to note that credit card companies sometimes waive this fee initially, but it often resurfaces after a grace period.

Why is “Arbitrate” referenced so frequently? Credit card companies commonly seek protection from consumers. Binding arbitration ensures disputes regarding theft, fraudulent charges, and other issues can’t be the subject of a traditional lawsuit. Instead, these matters must be resolved through an equitable hearing, which could take up to two years (and countless legal fees) to resolve. Arbitration provisions generally appear at the end of credit card agreements, and they’re easy to overlook.

Consumer Card Debt vs. Credit Card Companies

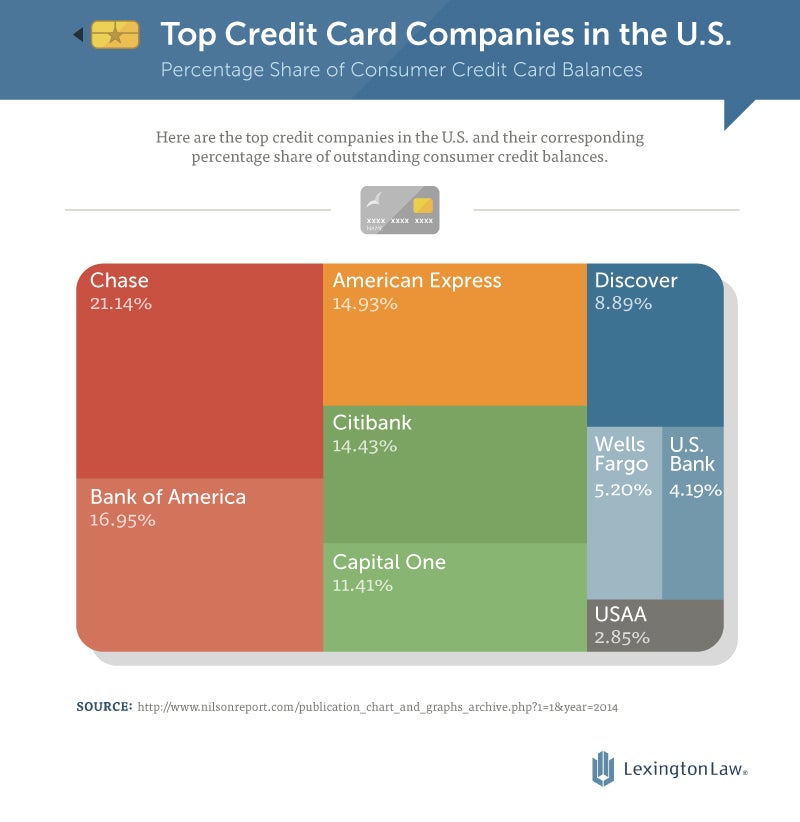

A small number of financial institutions dominate the credit card market. Some familiar names include Chase, American Express, Discover, and Capital One. Chase is one of the top credit card issuers in the U.S., and it owns the biggest share of consumer credit card debt. Back in 1955, Chase was known as Chase Manhattan Bank; it grew into one of the top lenders after a series of acquisitions and mergers. In 2000, J.P. Morgan & Co. merged with Chase.

American Express is another well-known and established lender. Amex is the foremost charge card issuer in the world, as well as the biggest travel company. Since its inception in the mid-1800s, it’s progressed into one of the most recognizable global financial brands. Special products like its invitation-only black card make it seem exclusive. And its numerous consumer products have made it the third-largest holder of outstanding credit balances.

Occasionally, even some of the top credit card companies have come under fire for engaging in deceptive practices. In 2015, lawmakers ordered Bank of America’s credit card division to pay out $727 million to around 1.4 million consumers for engaging in deceptive practices. Despite this, it still owns the second-largest share of outstanding balances today.

The Rates and Fees for Major Credit Card Companies

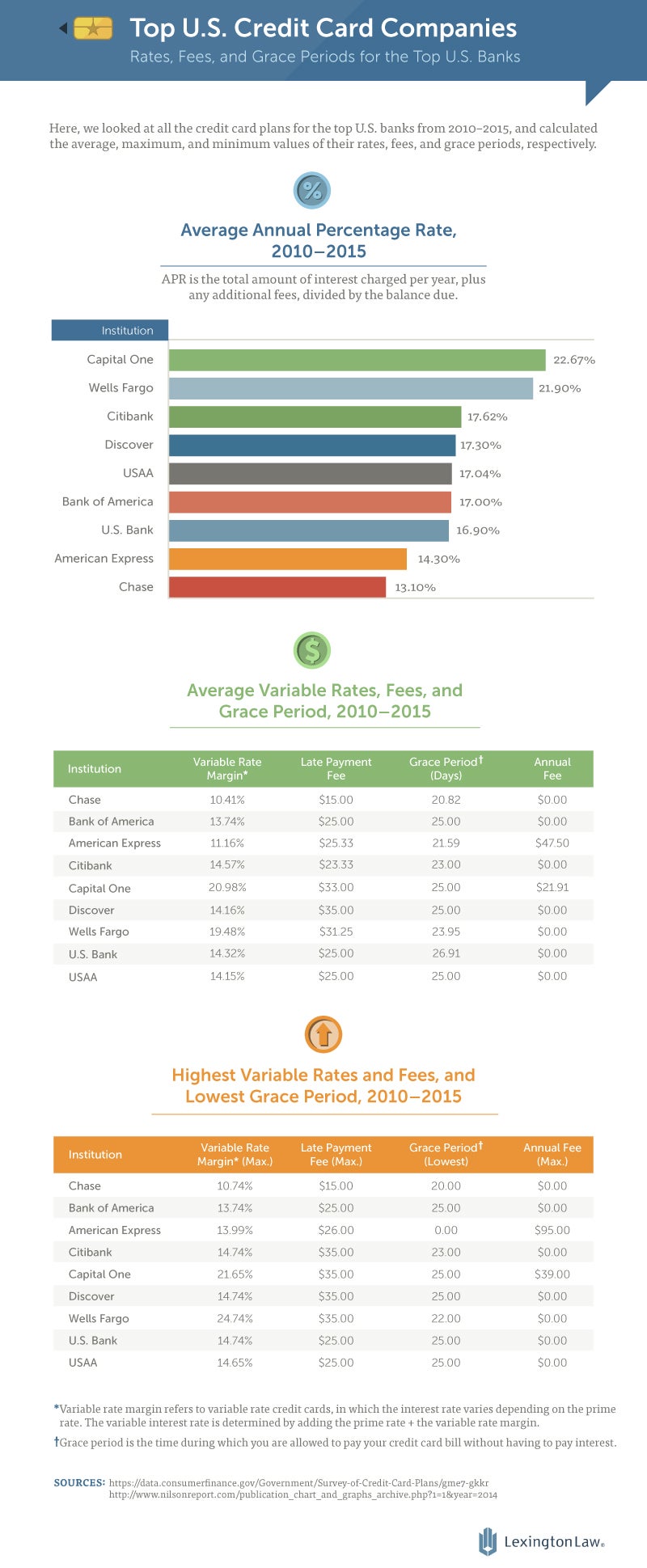

Each credit card plan, including its payment schedule and fees, is different. For example, a consumer could hypothetically be granted a Capital One credit line with a $3,500 limit. As part of a special offer, the person also may be subject to no annual fee and receive a six-month zero-interest grace period on purchases. However, once the interest rate increases, the consumer may pay as much as 22.67% interest (Capital One average annual rate from 2010 to 2015). Prior to the increase, if the consumer makes only a minimum payment, it could take years to pay down the remaining balance. This could theoretically result in years of payments with the total interest paid potentially being higher than the original balance.

The average APR for Chase’s credit card plans is 13.1% (far above an average mortgage interest rate), and it has an average grace period (or the number of days before before the interest is assessed) of about 21 days. About 17 percent of credit cards have annual fees. On the low end, plans may charge as low as $9; on the high end, American Express has annual fees as high as $95.

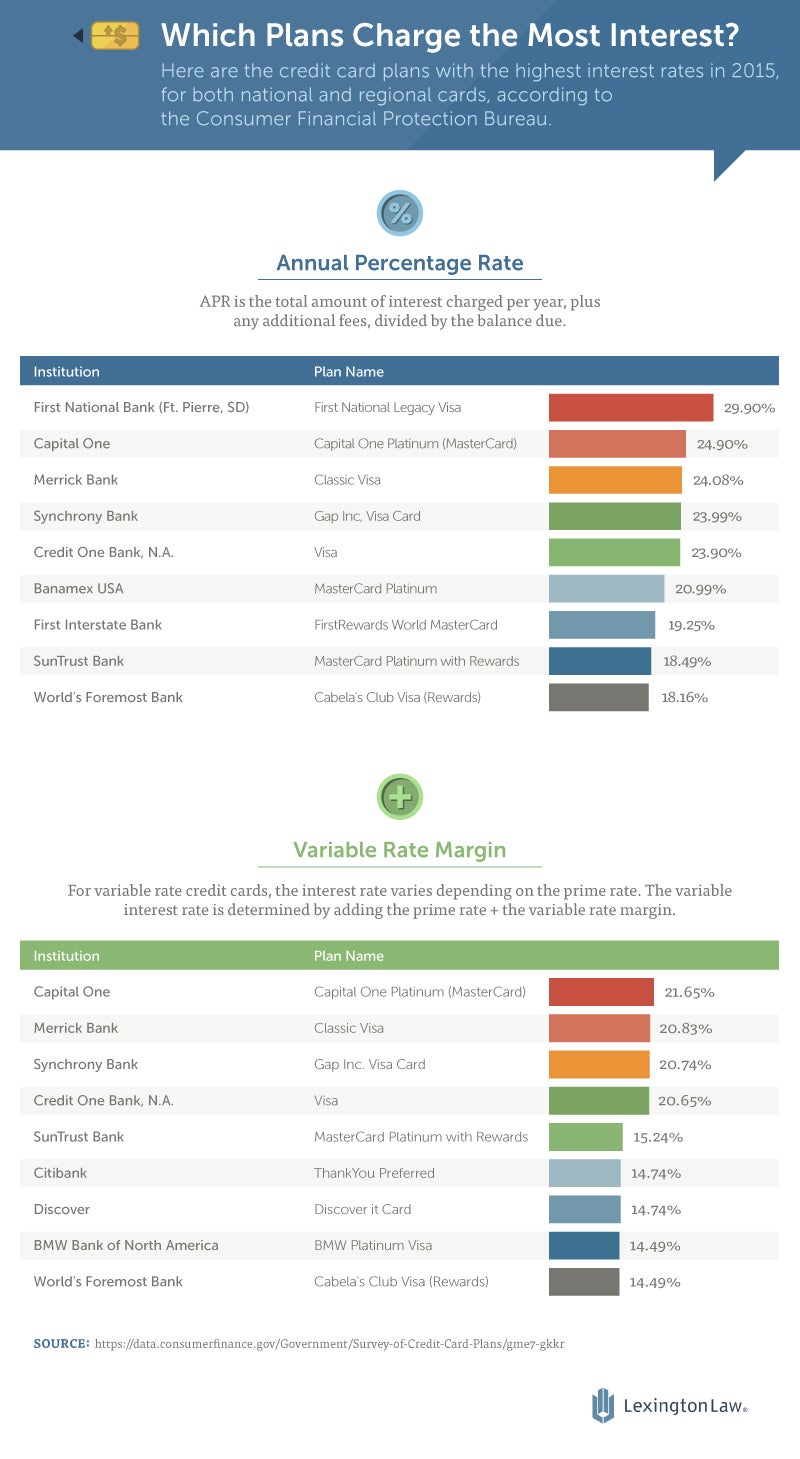

High Interest Rates

Today, there are significantly fewer fixed-rate credit cards. The Credit CARD Act of 2009 made it difficult for card issuers to raise their interest rates for fixed-rate credit cards; as a result, banks began issuing a higher number of variable-rate credit cards so that interest amounts could fluctuate based on the market. Most credit cards will have a variable APR, which is tied to the prime rate. The prime rate as reported by The Wall Street Journal’s bank survey is among the most widely used benchmarks for determining the prime rate for credit cards. The credit card company adds a percentage margin to the variable APR. So for variable credit cards, the total APR the consumer pays in interest is the variable rate margin plus the prime rate. If the prime rate index goes up, so does the rate; if the index goes down, so does the APR.

The graph above shows the highest APR and variable-rate margins charged for credit card plans in 2015. First National Bank of Fort Pierre, SD, for example, offers a Legacy Visa that charges 29.9% APR. How does a rate like this impact a consumer’s overall debt? If a person owes a credit card balance of $1,000 and makes a minimum payment of $35, it would take over eleven years (136 months) to pay off the balance. The consumer would also pay over $1,700 in interest.

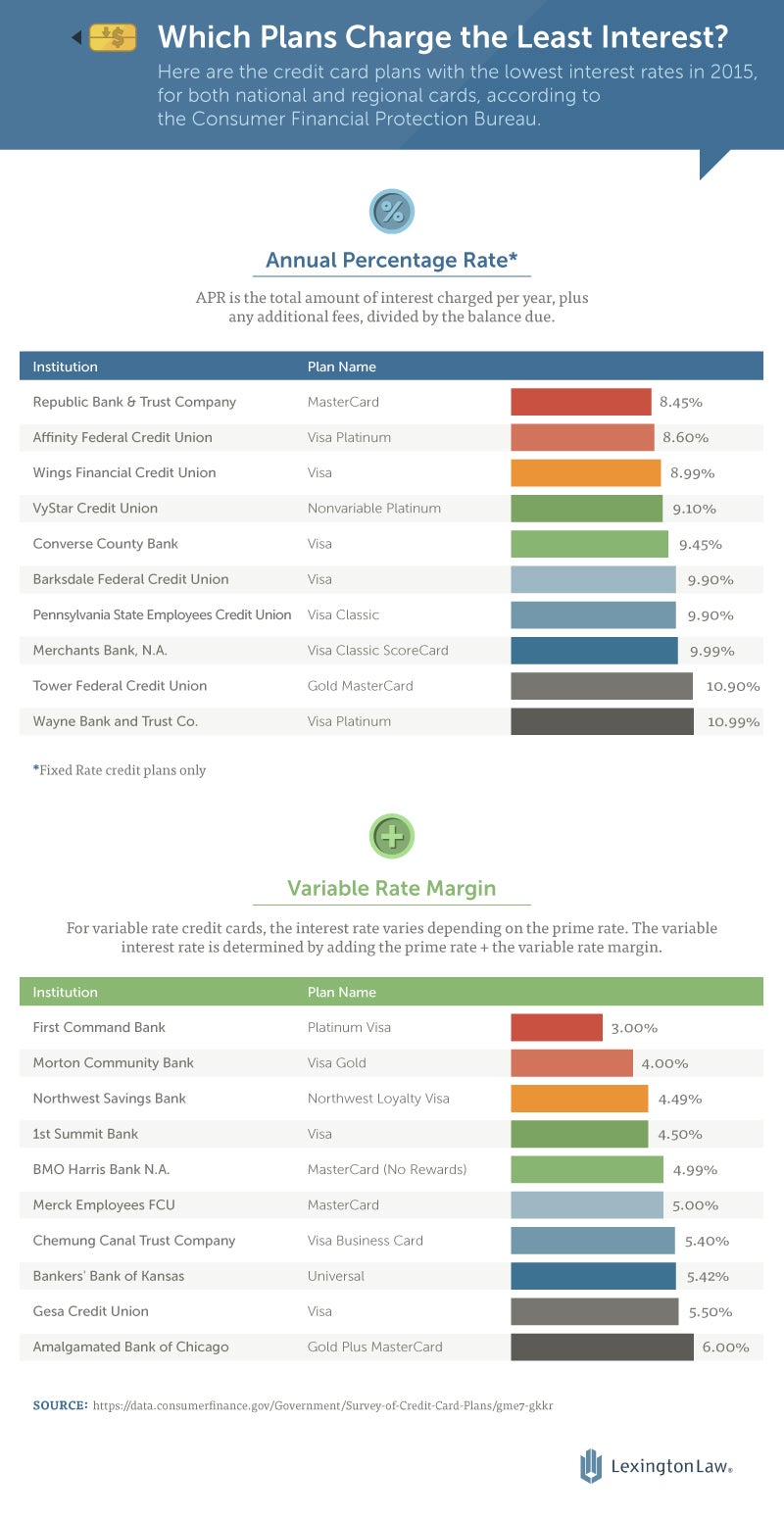

Low Interest Rates

VyStar Credit Union, located in Jacksonville, FL, is one of the largest credit unions in the U.S. It offers a range of plans, but its platinum card guarantees a fixed-rate APR of 9.1%. The advantages of dealing with a credit union are increased customer support, fewer hidden fees, and typically a lower interest rate. First Command Bank, located in Fort Worth, TX, offers an attractive Platinum Visa card with no annual fee, over-limit fee, balance-transfer fee, or online account access fee. It also has a variable margin rate of 3%. Plans like these are diamonds in the rough – but if you search diligently, you can find a card that’s affordable over time.

VyStar Credit Union, located in Jacksonville, FL, is one of the largest credit unions in the U.S. It offers a range of plans, but its platinum card guarantees a fixed-rate APR of 9.1%. The advantages of dealing with a credit union are increased customer support, fewer hidden fees, and typically a lower interest rate. First Command Bank, located in Fort Worth, TX, offers an attractive Platinum Visa card with no annual fee, over-limit fee, balance-transfer fee, or online account access fee. It also has a variable margin rate of 3%. Plans like these are diamonds in the rough – but if you search diligently, you can find a card that’s affordable over time.

Credit Cards Create Equality

Back in the 1990s and earlier, credit cards were a luxury. Financial institutions assessed annual fees based on the exclusivity of owning a card, and the associated APRs were steep as well. Today’s credit cards have leveled the playing field. Anyone can get a credit card. But much like the subprime mortgage crisis of 2008, where anyone could obtain a mortgage regardless of his or her ability to pay, credit cards can drive down one’s credit score and saddle them with unnecessary debt.

Conclusion

Companies may offer 0% APR, a generous grace period, and cash-back incentives, rewards, airline miles, and more, but just below those promises is fine print that can add up to costs potentially exceeding one’s original debt. The bottom line: buyer beware.

To get the most out of a credit card, it’s a good idea to follow these tips: Compare a credit card offer to additional offers, and pay careful attention to the fine print of each; if possible, don’t carry a balance, and always pay off the balance every month. If all else fails, remember, mounting debt can lead to a poor credit score. Help is available.

Methodology

We analyzed all the credit card agreements contained in the Consumer Financial Protection Bureau’s “Survey of Credit Card Plans” since 1990. For the list of top credit card companies in the U.S., we utilized The Nilson Report’s research on the top U.S. credit companies, parsing it by highest outstanding consumer balance. For the word cloud, we chose the top plans from each of the top credit institutions, and combined all the text to create the list of words depicted.

Fair Use

We grant permission to share the images found on this page freely. When doing so, please attribute the authors by providing a link back to this page so your readers can learn more about this project and the related research.