The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

The IRS will not report the taxes you owe to the credit bureaus. They work with private collection agencies, but this does not show up on your credit report. However, it can harm your finances in other ways.

Americans owed over $114 billion in back taxes, penalties and interest in 2020, according to the IRS. This means that a lot of people are at risk of having their tax debt go into collections. As America recovers from the pandemic, many people are still struggling to pay their taxes, so if you have a large tax debt, you’re not alone. Unfortunately, if you don’t pay your taxes, your debt is at risk of going to collections.

The main concern you may have is that IRS collections may damage your credit score, but this isn’t necessarily the case. Here, you’ll learn how the private IRS collection agency actually works and what happens to your credit if you don’t pay your taxes. With this understanding, you can better manage your financial life and work to maintain a healthy credit score.

Do IRS collections go on a credit report?

If you haven’t been up to date on paying your taxes, you don’t have to worry about it showing up on your credit report. Not only does the IRS not report collections to the three major credit bureaus, but they also don’t report missed or late payments either. This is good news because late and missed payments can hurt your credit score when they’re reported.

The Taxpayer Bill of Rights states that all American taxpayers have the right to privacy and confidentiality, which is why your outstanding debt isn’t reported. This is beneficial because your credit report is run when you apply for loans, housing and other services. Regardless of what you owe, those who check your credit won’t see your outstanding tax debt.

Do IRS tax liens show up on your credit report?

Tax liens used to show up on your credit reports, but this changed as of April 2018. A tax lien is when the IRS files a legal claim against you for the taxes that you owe. If the IRS files a tax lien, you are obligated to pay your tax debt, or they have the right to seize your assets and sell them as a way to pay off your debt.

The halting of reporting tax liens was part of the National Consumer Assistance Plan (NCAP), which removed public records from credit reports. Although the IRS can still pursue a seizure of your assets, this does not show up on your credit report, unlike Chapter 7 bankruptcy, which also seizes property and does show up on your credit report.

What happens if the IRS sends you to collections?

Much like other forms of debt, your IRS debt can go to a collection agency due to nonpayment. Congress passed a law that became effective as of September 2021 that requires the IRS to work with private collection agencies. These debt collectors will attempt to contact you, and if you still can’t pay off your debt, you can work with them to arrange a payment plan that works for you.

There are a few reasons the IRS may send your debt to a private collection agency:

- They couldn’t locate you

- You have not interacted with the IRS in over a year

- It’s been over two years since the assessment of your account

The IRS works with three specific agencies who may contact you:

How tax debt can hurt your credit score

While tax debt can’t directly affect your credit score, the situation can affect your credit in other ways. When looking at your financial situation, it’s helpful to look at everything as a whole. Each debt affects something else in your financial life because you only have a finite amount of money.

Here are some ways tax debt can indirectly affect your credit score:

- Paying the IRS instead of other debts: If you have other debts, such as an auto loan or credit card debts, prioritizing your IRS debt can lead to missing your other payments.

- Paying IRS interest and fees: Relatedly, the IRS charges interest and fees like other debts, and this extra money could go toward paying off debts affecting your credit.

- Using credit cards to pay debt: You can pay the IRS with a credit card, but this is just moving the debt to your credit card.

- Taking out loans to pay debt: If you’re low on funds, you may turn to personal or payday loans, which can affect your credit if you don’t pay them back.

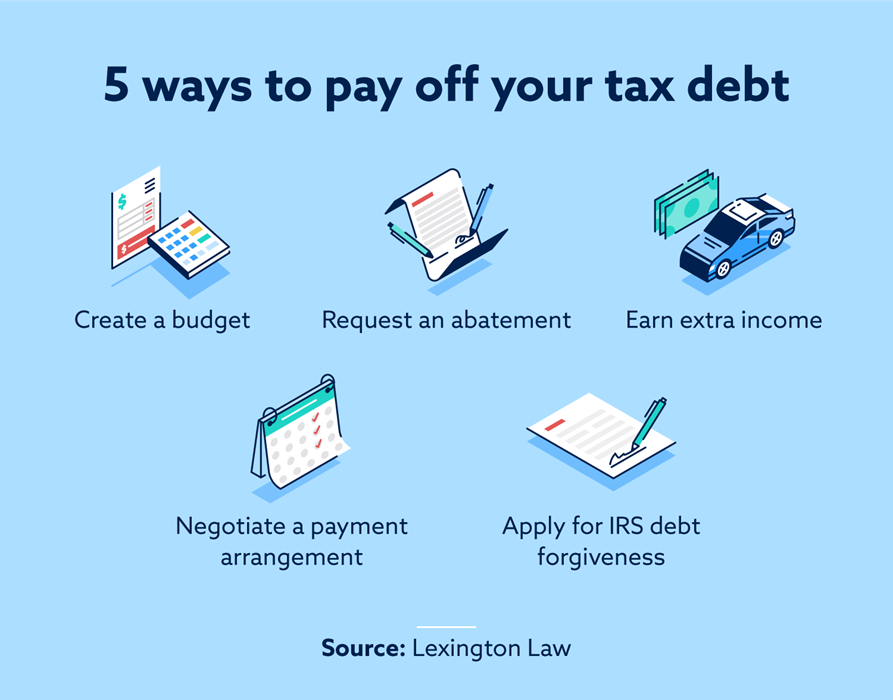

How to pay off your IRS tax debt

One way to avoid having your IRS tax debt go to collections is to have a plan. When you have a plan to pay off your debt, or at least make it manageable, you can ensure you’re able to pay your other debts as well.

Create a budget

This should be the go-to strategy whenever you’re dealing with any debt. If you want to eliminate your debt as quickly as possible, you can sit down and take a look at where you can cut costs. As you find places to reduce your expenses, you’ll see you have more money to pay off your tax debt.

Here are some simple ways to start budgeting:

- Downgrade services: You may be able to save money by eliminating some streaming services or downgrading your phone or internet plan.

- Be smart at the grocery store: Start taking advantage of coupons. Making a list before shopping can also help reduce the amount of unnecessary purchases.

- Give yourself an allowance: You can still treat yourself by going out with friends, but give yourself a set amount and monitor spending.

Apply for IRS debt forgiveness

If you meet certain criteria, you may qualify for some IRS tax debt relief. The IRS has something called an offer in compromise (OIC), which allows you to settle your tax debt for less than what you owe. You’ll need to apply for this forgiveness, and some of the factors they look at include:

- Ability to pay

- Income

- Expenses

- Asset equity

Negotiate a payment arrangement

If you don’t qualify for an OIC, you may still be able to work out a payment arrangement. You don’t need to pay your tax debt all at once, and the IRS will work with you to see what you’re able to pay each month based on your income. This process also involves an application that you can fill out on the IRS website.

Request an abatement of penalties and fees

As mentioned, the IRS charges interest and fees on late taxes. Under certain circumstances, you can request first time abatement relief. This is helpful if you’re late on your taxes from the previous year because it will remove your late penalties if approved.

Sell some assets or earn extra income

Rather than getting to the point of a potential tax lien, if you need to get caught up on your tax debt, consider selling some assets. This way, you have control over what you sell. If that’s not an option, you can look into making extra income by finding a side job or working additional hours to pay off your debt.

What to do if tax debt is affecting your credit and finances

Being burdened with tax debt can hurt your finances and your ability to pay off other debts that are affecting your credit. Sometimes, it takes some outside help to get your financial life in order so you’re able to pay off your debts while still being able to live comfortably. Lexington Law has a team of legal consultants who can help with financial education and to help you work on your credit.

Lexington Law has over 15 years of experience helping people repair and improve their credit while also providing tools to help them learn more about financial planning. We offer a wide range of services, including financial education to teach you about credit and much more. To learn more about how we can help you, contact us today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.