The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Sometimes, people get stuck underwater in various types of debt, and it can be difficult to stay afloat. Fortunately, Chapter 7 bankruptcy allows people to eliminate some of this debt so they can have a fresh start. Filing involves getting documentation of your finances, taking courses and getting the help of a legal professional, but it’s worth the effort.

If you’re considering filing bankruptcy under Chapter 7, you’ll need to understand exactly what it is as well as the pros and cons. Chapter 7 bankruptcy helps people eliminate overwhelming debt, and today we’ll discuss the details of filing and why you may want to talk with a bankruptcy attorney to see if it’s the right option for you. Many attorneys even offer free consultations to help you make your decision about bankruptcy.

Table of contents

- What is Chapter 7 bankruptcy?

- How does Chapter 7 bankruptcy work?

- Who qualifies for Chapter 7 bankruptcy?

- What do you lose when filing for Chapter 7 bankruptcy?

- What can you keep when filing for Chapter 7 bankruptcy?

- What’s the difference between Chapter 7, Chapter 11 and Chapter 13 bankruptcy?

- How to file for Chapter 7 bankruptcy

- How long does filing a Chapter 7 bankruptcy take?

- How much does it cost to file Chapter 7?

- Pros and cons of filing Chapter 7 bankruptcy

- How long does Chapter 7 stay on credit reports?

- What to expect after filing

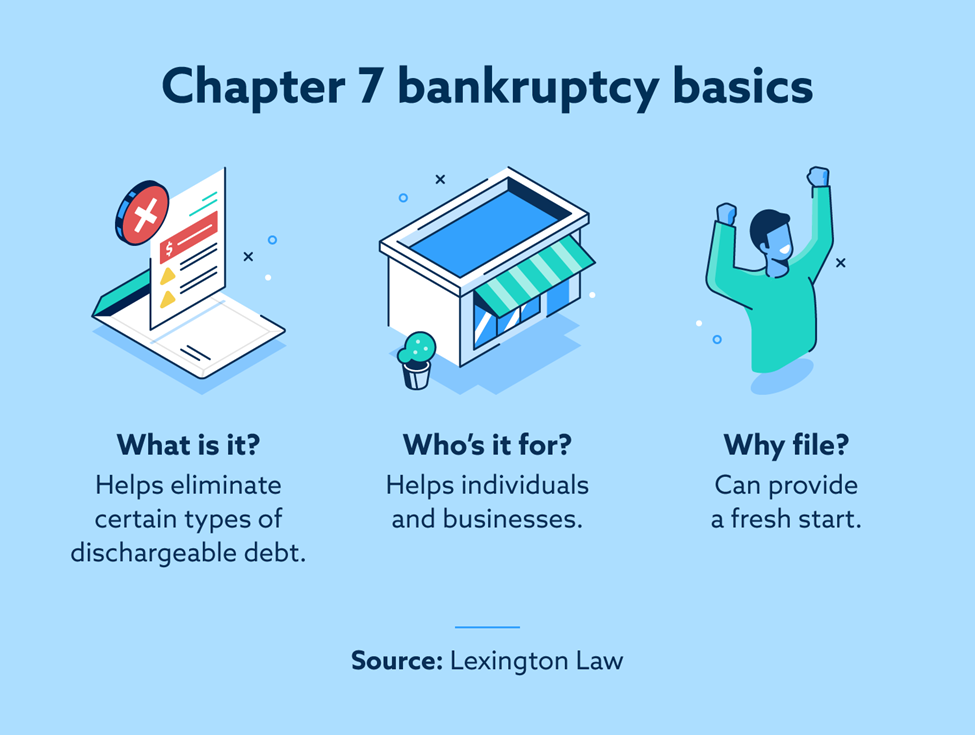

What is Chapter 7 bankruptcy?

Chapter 7 bankruptcy, sometimes also known as liquidation bankruptcy or fresh start bankruptcy, is for individuals who are unable to make their regular payments toward their debts. Under Chapter 7, your nonexempt belongings and property are liquidated to repay creditors, and all remaining dischargeable debt is discharged upon completion of the bankruptcy process.

A common misconception about filing for this kind of bankruptcy is that it will wipe away all of your debts, but the Chapter 7 bankruptcy definition is a bit more nuanced. We’ll be discussing dischargeable vs. non-dischargeable debts so you have a better understanding of which debts are and aren’t eliminated.

How does bankruptcy (Chapter 7) work?

If you’re considering filing for Chapter 7 bankruptcy, a great first step may be to consult a professional to see if you qualify and if it’s the right option for you. Typically, the professional will be a lawyer who specializes in bankruptcy, and they can show you how to file for Chapter 7 bankruptcy. They’ll have you gather all of your financial information, which can include your income, your debts and a wide range of financial statements like bank statements.

The length of time from start to finish can vary by a few months, but some immediate actions are taken once you begin the process of filing for bankruptcy. The lawyer you’re working with will file the initial paperwork to the court stating that you’ll be filing for bankruptcy.

What happens when you file for bankruptcy?

Once your paperwork is processed, the court sends a document to every financial institution attempting to collect payment from you, telling them to stop. This is called an “automatic stay.” An automatic stay can be quite helpful if you were at risk of wage garnishments due to your debts.

What happens when you work with a bankruptcy attorney?

After the automatic stay is in place, you’ll continue to work with your lawyer to get all of your documentation together to complete the filing process. When you’re working with the lawyer, it’s extremely important that you’re as transparent as possible and give them all of your financial information so they can submit it to the court. This is very important because withholding information can be deemed a criminal offense by the bankruptcy court.

What happens in court when filing for Chapter 7 bankruptcy?

After providing your lawyer with all of your financial information, you’ll be required to go to court to meet with a trustee. This is typically a brief meeting, though it can vary by state. When meeting with the trustee, you’re verifying that the information you’re provided is correct. Then, your Chapter 7 bankruptcy requirements work their way through the courts, and you’ll eventually receive a discharge. A discharge is when the debtor is released from liability of certain types of debts, and this takes roughly four to five months.

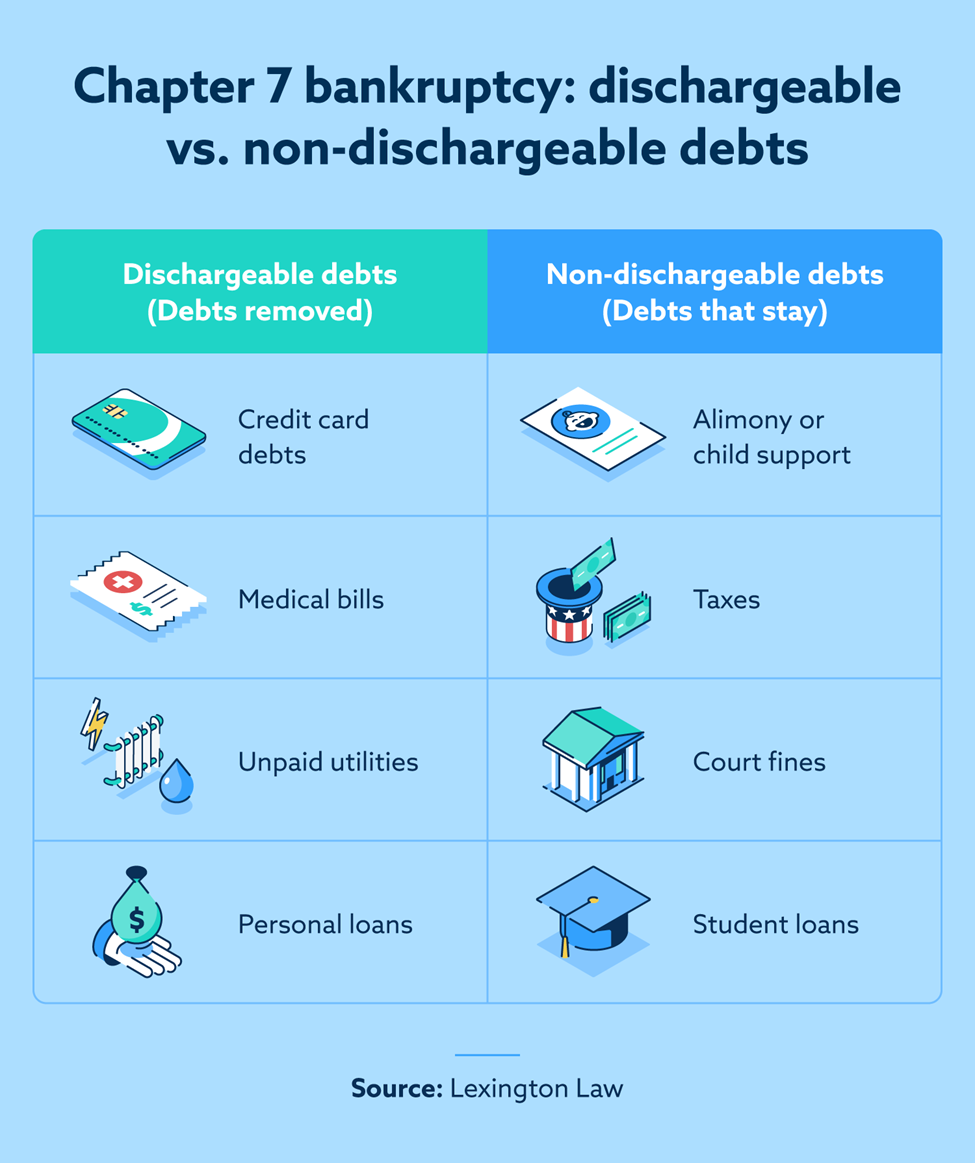

Dischargeable debts

So, what debts can be erased or forgiven by Chapter 7 bankruptcy? Dischargeable debts are debts that are typically erased by filing for Chapter 7 bankruptcy. These debts can be forgiven because there are no bankruptcy laws that prevent them from being discharged.

Dischargeable debts can include:

- Credit card debts

- Medical bills

- Unpaid utilities

- Personal loans

Non-dischargeable debts

What debts can’t be erased by filing for Chapter 7 bankruptcy? There are various debts that can’t be eliminated because you may be mandated to pay by the courts, or you may owe the money to the government.

Non-dischargeable debts can include:

- Alimony or child support

- Recent taxes

- Fines and penalties ordered by the court

- Most student loans, unless you can prove undue hardship

Who qualifies for Chapter 7 bankruptcy?

Your eligibility for Chapter 7 bankruptcy depends on both your income and the application of a means test. The Chapter 7 bankruptcy means test looks at your income from the last six months in combination with your household size and other parameters. With the means test, the court is looking at your financial situation in comparison to other same-sized households within your state to see if you qualify for bankruptcy.

One requirement to qualify and file for bankruptcy is to attend a credit counseling course. These courses can be done individually or in a group setting, and they’re often offered online. These counseling courses provide some tips and tools to hopefully help people avoid similar financial situations in the future.

Chapter 7 bankruptcy qualifications include:

- You cannot have filed Chapter 7 bankruptcy and received a bankruptcy discharge within the last eight years

- A means test must show a lower monthly income than the average household of the same size in your state

- You must wait 181 days before filing for bankruptcy if your previous filing was dismissed

- You cannot have filed Chapter 13 bankruptcy and received a discharge within the last six years

- You must complete credit and debt counseling courses

How much do you have to be in debt to file Chapter 7?

There’s no minimum debt amount required to file for Chapter 7. This means that your debt can be a few thousand dollars or $50,000. Either way, if you meet the other criteria for filing for Chapter 7 bankruptcy, you can proceed through the courts.

The primary reason why there is no minimum debt required to file for bankruptcy is that everyone’s financial situation is different. For example, the median household income in 2020 was $67,521. There are many individuals who had an income far above or below the median as well. Spending habits can vary regardless of your income, so having no minimum debt requirement helps maintain equality.

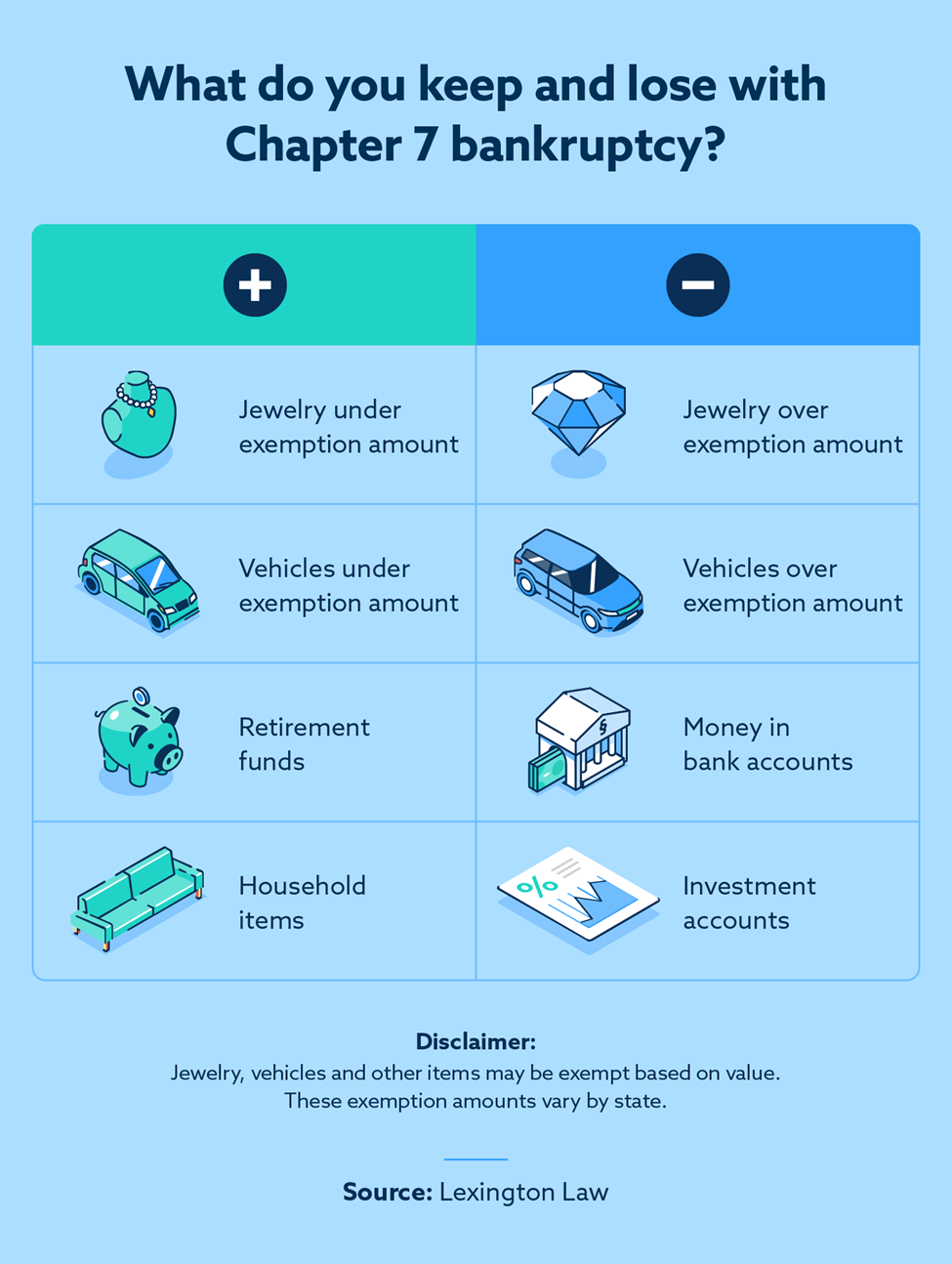

What do you lose when filing for Chapter 7 bankruptcy?

When filing for bankruptcy, it’s important to remember that lenders are also involved in this situation, and they’re hoping to recoup their money. The courts understand this, which is why they may seize certain assets during the bankruptcy process.

The trustee you meet with is who ultimately determines what’s seized when you file for bankruptcy. Due to movies and television, you may envision a big moving truck coming to take everything you own, but that’s not the case. The trustee is looking for valuable assets. Sometimes, they will send appraisers to your home to see what is worth seizing and selling.

Some of the most common losses when filing for Chapter 7 bankruptcy include:

- Jewelry worth more than your state’s exemption limit

- Vehicles worth more than your state’s exemption limit

- Investment accounts

What can you keep when filing for Chapter 7 bankruptcy?

Exemptions for property differ by state, but in most states you can keep vehicles, retirement savings and jewelry up to a certain value. For example, in the state of Utah, exempt items include most furniture, vehicles not used primarily for recreational purposes and heirlooms with sentimental value.

Since these exemptions are different in each state, you want to make sure you contact a professional when you’re ready to file. They can help set your mind at ease by letting you know what the state will let you keep when you go through the bankruptcy process.

Some of the most common items you can keep when filing for Chapter 7 bankruptcy in most states include:

- Vehicles worth up to your state’s limit

- Funds in tax-exempt retirement accounts

- Jewelry up to your state’s limit

- Household items such as furniture, clothes, books and more

Can you keep your home when you file for Chapter 7 bankruptcy?

One of the most common questions people ask about bankruptcy is, “Will I lose my house if I file for Chapter 7 bankruptcy?” Fortunately, in many cases, you won’t have to worry about losing your home when filing for bankruptcy.

Most states have a “homestead exemption,” which protects your home if your equity is under a certain amount. If you do keep your home, you’ll have to continue to pay your mortgage on time because this is a secured debt.

If your home exceeds the exemption amount, you will need to sell it as part of the bankruptcy process. The exemption is typically based on the amount of equity in the home.

For example, let’s say you have $30,000 worth of equity. If the homestead exemption is higher than $30,000, you don’t have to worry about losing your home. If the equity is less than that, your home will be sold, and you’ll receive the exemption amount of $30,000.

Pros and cons of filing Chapter 7 bankruptcy

If you’re still on the fence about whether or not you should file for Chapter 7 bankruptcy, it can be helpful to create a pros and cons list. As with many major decisions in life, there are benefits as well as downsides of filing for bankruptcy. Each person’s situation is different, and you’ll need to take a look at your specific circumstances to make the decision that’s right for you.

For some people, filing for bankruptcy can be a massive weight lifted off of their shoulders. On the other hand, some people look back at their experience filing for bankruptcy and believe they should have taken a different approach to handling their debt.

Pros of Chapter 7

When you’re discharged from your bankruptcy, one of the biggest benefits is that you no longer have to worry about dischargeable debts. You’ll have peace of mind knowing that the debt collectors will stop calling and sending you letters in the mail. Here are some other pros of Chapter 7 bankruptcy:

- Debt relief

- No repayment plan for discharged debts

- Keeping many of your belongings

- A fresh start

- No worries about future wage garnishments

Cons of Chapter 7

Before filing for Chapter 7 bankruptcy, it’s good to take a step back and recognize some of the cons. There are certain losses that some people don’t want to have when figuring out how to manage their debt. This is personal to you and sometimes your family, so it’s good to take some time to think about the following consequences of Chapter 7:

- Damage to your credit

- Potential loss of some nonexempt properties

- Non-dischargeable debts are not included

- Fees for filing and attorney costs

- Loss of property such as jewelry, vehicles and other items

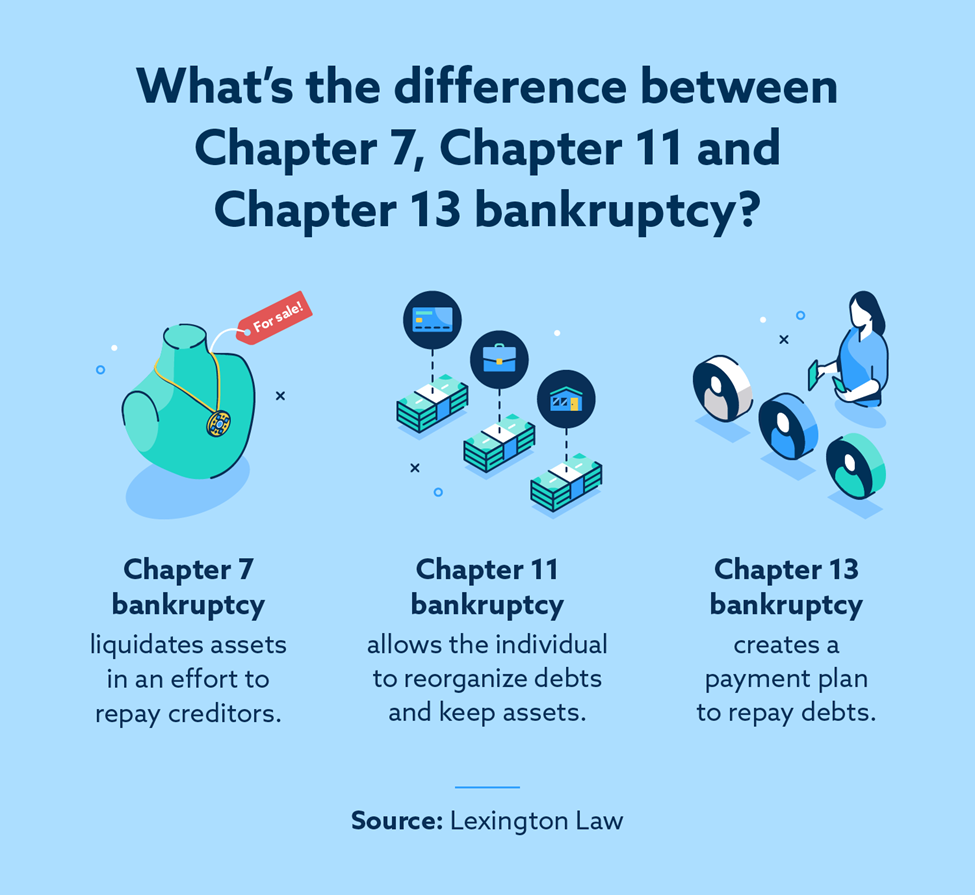

What’s the difference between Chapter 7, Chapter 11 and Chapter 13 bankruptcy?

When considering bankruptcy, it’s good to know the difference between Chapter 7, Chapter 11 and Chapter 13 bankruptcy, which are the most common types of bankruptcy. Most people will never encounter the other types of bankruptcy, so we’ll focus on these three.

Chapter 7 bankruptcy is available to both individuals and businesses. As you’ve read, in Chapter 7 bankruptcies, some items and property may be liquidated in order to pay the creditors. Once complete, the filer will receive a complete discharge from the dischargeable debts based on the court’s decision.

Chapter 11 bankruptcy is meant to allow an individual or business an opportunity to reorganize their debts. While reorganizing debts, you don’t lose any of your assets, which is why many businesses go with this option. So, if you’re a small business owner, this protects everything that you use to run and operate your business. If you’re a sole proprietor, chapter 11 bankruptcy affects your personal assets as well.

Chapter 13 bankruptcy is one of the common alternatives to those who are considering filing Chapter 7 bankruptcy. Chapter 13 bankruptcy, rather than eliminating your debts during the discharge, allows you to figure out a payment plan for the creditors. When filing Chapter 13 bankruptcy, the average time to repay your debts is usually between three and five years. It’s also important to note that while a Chapter 7 bankruptcy can remain on your credit reports for up to 10 years, Chapter 13 bankruptcies should fall off after eight years.

How to file for Chapter 7 bankruptcy

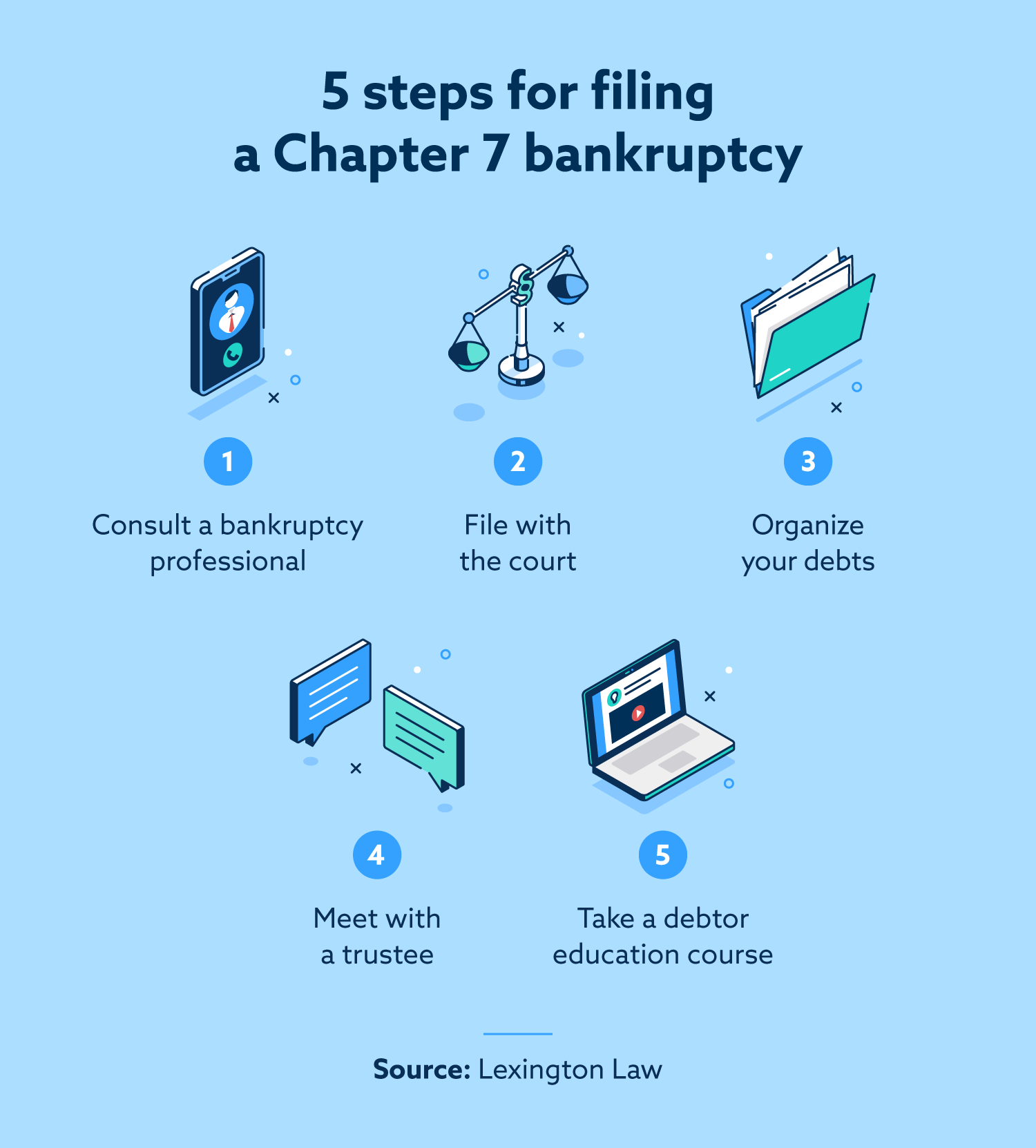

In order to have better chances of a discharge with a desirable outcome, there are some steps you need to take when filing for Chapter 7 bankruptcy. This can be a long, in-depth process, so you want to make sure you’re organized when you’re getting prepared to file. Some people choose to file Chapter 7 bankruptcy on their own, but it’s usually a good idea to work with a professional to ensure that nothing is missed during the filing process.

Step 1: Consult a bankruptcy professional

It’s highly recommended that you consult a bankruptcy professional when you’re getting ready to file. You can find a lawyer who specializes in bankruptcy law and will help you from the beginning of the process until the discharge. During this consultation, your attorney may recommend you preemptively take a credit counseling course, which is required as part of the process.

Step 2: File with the court

When you’re ready to begin the process, you and your lawyer should contact the court as soon as possible. By initiating the bankruptcy process, letters will be sent out to creditors to halt collection calls and any acts of wage garnishment.

Step 3: Organize your debts

You may have already started to gather some of your financial information, but now it’s time to organize your debts. One great way to do this is to categorize your debts into “secured” and “unsecured” debts. And don’t forget to be open, honest and transparent with your lawyer. The courts do an in-depth investigation during this process, so be sure to disclose everything.

Step 4: Meet with a trustee

Once you’ve started the filing process, you’ll receive a date to go to court and meet with a trustee. Meeting with the trustee involves stating that everything you’ve presented is accurate, and they may ask you some questions about your assets.

Step 5: Take a debtor education course

That’s right—there’s another course that you’ll need to take before your bankruptcy is complete and you receive a discharge. In this course, you’ll learn additional skills for financial management that can assist you in avoiding another bankruptcy in the future.

How long does filing for Chapter 7 bankruptcy take?

On average, from start to finish, filing for Chapter 7 bankruptcy can take four to five months. This may seem like a long time, but during this period, your wages will be safe, and you don’t have to worry about calls from collection agencies. There will also be a complete review of your documents and an investigation to ensure everything is accurate.

When you file for bankruptcy, you start to see why it will take months to complete. The paperwork alone can be upward of 100 pages, which takes time for the court to process. There’s a lot to go through during this process, and you’ll also be taking courses and meeting with a trustee. If all goes well, you’ll soon receive a discharge that releases you from many of your debts.

How much does it cost to file Chapter 7?

On average, Americans pay between $400 and $4,000 for an attorney as well as the filing fees. Depending on the state you’re in, the filing fee, trustee surcharge and administrative fee can be upward of $400.

Attorney costs can vary, but how much you pay often depends on the complexity of your case. If the case is more complex, it can take much more time to resolve as they go through your documents and figure out how to help you in the best way possible. According to a study conducted by the University of Maine, the average attorney fees are between $968 and $1,072.

How long does Chapter 7 stay on credit reports?

When you file for Chapter 7 bankruptcy, it can stay on your report for up to 10 years, and this can affect your future financial decisions.

If you’re considering filing for this kind of bankruptcy, it’s helpful to take a look at what you want to do or accomplish over the next 10 years. Do you plan on buying a vehicle or a home? Most purchases that involve a lender can become more difficult when you have a bankruptcy on your credit report. In some cases, this can also affect your ability to get a student loan if you plan on going back to school.

What to expect after filing

Now that you know the ins and outs of bankruptcy, you may want to know what happens after you file for Chapter 7 bankruptcy. As mentioned, this process can take anywhere from four to six months on average, but by the end of it, you may have quite a bit of financial relief. If the courts go through your documents and you meet all of the requirements, you have a better chance of receiving a discharge. Once you receive the discharge, you’re no longer required to pay for the dischargeable debts that you owed to lenders.

Once your bankruptcy is over, you can have a fresh start. For some people, money management can be a major issue, but due to the required courses and overall bankruptcy filing experience, they may gain a new perspective about money. Sometimes, filing for Chapter 7 bankruptcy can help a person get their financial life in order and create a better future for themselves.

As you move through the bankruptcy process, it’s a good idea to work with professionals who can also help you with your credit after you receive your discharge. Find out more about Lexington Law credit repair services and how our professional consultants can help you move past your bankruptcy.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.