America has a growing problem with auto loan debt, as the total reached $1.23 trillion in quarter one of 2018. This increase is not surprising as auto loans are used on 85 percent of new car purchases and 53 percent of used car purchases in America.

With auto loans being the third largest form of debt in the United States, many are concerned the rise in default rates will cause a market crash. Accounting for a quarter of all auto loans, subprime lending practices are cited as contributing to this large debt.

However, Americans are still accountable for the rise in auto loans as 95 percent of households own a car and 85 percent of Americans commute to work by automobile.

To determine why auto loan debt is on the rise, we polled over 6,000 Americans to find out how they purchase vehicles. Our study found that:

- 34 percent of Americans think it’s better to buy a new car with an auto loan, than a cheap car you can afford.

- 1 in 3 Americans pick an auto loan based off of monthly payment cost, a decision that can come at a high price when scaled with long-term payment plans.

- 1 in 4 Americans would finance a new vehicle with savings.

To determine Americans’ likelihood to use auto loans we asked if it is better to purchase a cheap car you can afford or a nice car using a loan.

A cheap car could be a way to save money but the value can diminish with the higher investments in upkeep, repairs and a shorter lifespan. Purchasing a nice car with a loan brings added debt, however the quality of the vehicle is better with a higher resale value and a lower investment in repairs.

66 percent of Americans say that purchasing a cheaper car you can afford is better than purchasing a nice car with a loan. Purchasing a car you can afford out of pocket still leaves a lot of options in the used car industry for many Americans.

A Consumer Reports study found that 71 percent of Americans will consider purchasing a late model used car as an alternative to a new car. Although purchasing a car used comes with the risks of not being covered by warranties, this choice can cut down on initial costs.

Additionally, as automobiles are valued by their quality, purchasing a cheap car could turn into a lot of mechanical work and a shorter lifespan, which is why the remaining 34 percent of Americans likely think it is better to buy a nice car with a loan.

Although financing options are available for people purchasing a new vehicle, the added price to the car through interest and fees can be steep, with the average annual percentage rate (APR) for car loans sitting at around 4.75 percent in the United States.

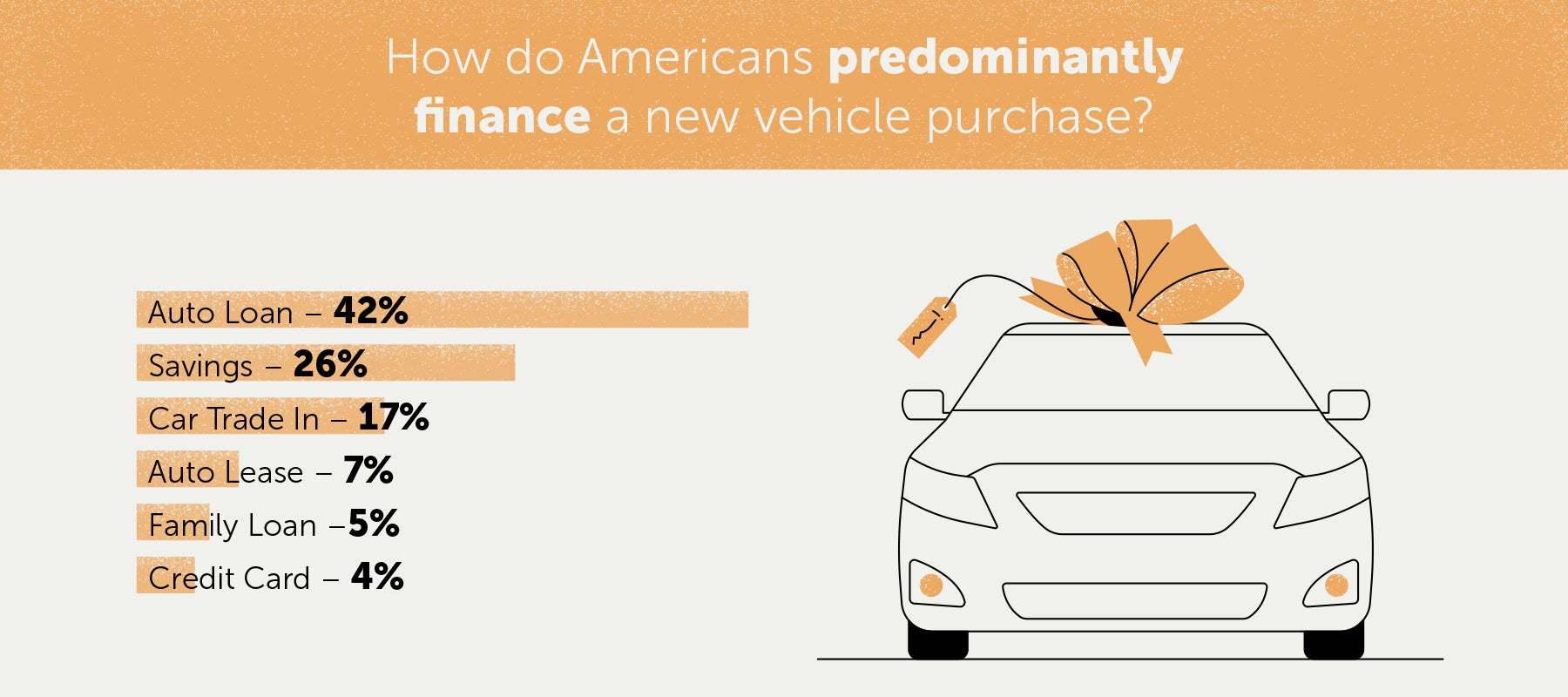

1 in 4 Americans say they would finance a new vehicle with savings.

Although taking out an auto loan is a steep investment, 42 percent of Americans say that it would be their main source of financing a new vehicle. A surprising 26 percent of Americans would predominantly use their savings to purchase a new vehicle, and 17 percent would use their car’s trade-in value.

Only 7 percent of Americans reported that they would predominantly turn to leasing options for financing a new car. Auto leases account for nearly 30 percent of all cars in America, and they do not lead to a full purchase of a vehicle. Auto leases are typically cheaper than auto loans, however, you do not eventually own the car. Instead, you are paying to borrow the car from a car dealership and cannot use the car later for trade-in.

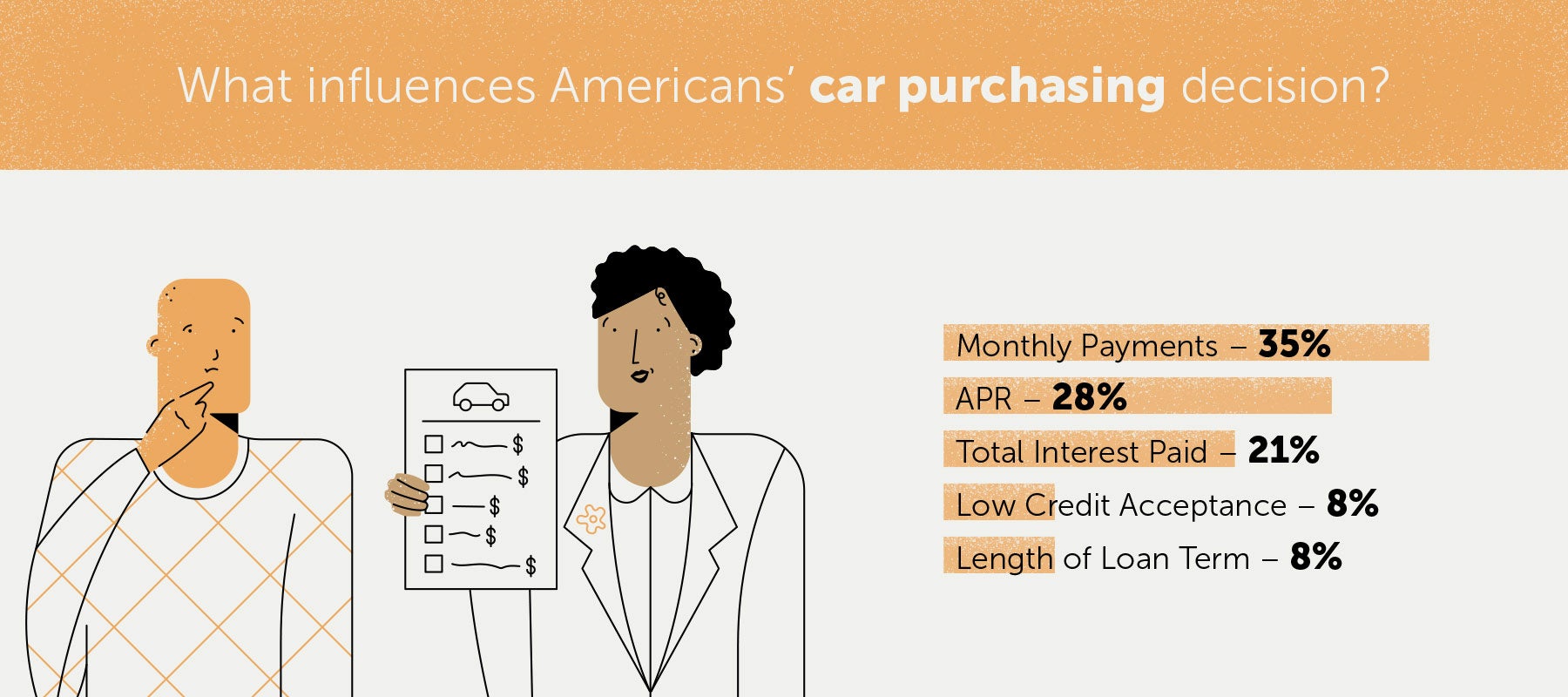

When it comes to finding an auto loan, Americans should shop around to find the lenders who offer the best deal on total interest paid. Total interest paid should arguably be the most important factor when it comes to picking out an auto loan as it is the total amount of money you will pay on top of the price of the car. When we polled over 2,000 Americans on how they shop for cars and look at auto loans, only 21 percent responded that total interest paid is their top priority.

Although the most important metric when shopping for a car loan is the total interest paid, 35 percent of Americans report that monthly payments are a top priority. This priority comes a cost though, given that a salesperson will often calculate your monthly payment using the longest term available.

Only 8 percent of Americans think about length of term when shopping for auto loans.

A study by Edmonds found that the two areas where new car advertisements are the most misleading are with the monthly payments and the annual percentage rates on their car financing. With tendencies to advertise a low monthly payment or annual percentage rate over a longer term, these aspects of auto loans are often misleading. As the average auto loan payoff term rises, more Americans are accepting loans with payoff terms of 84 months or longer, making monthly payments a costly prioritization that can last over seven years.

You may also end up paying out-of-pocket fees if your car is totaled or stolen during this extensive payment period. Standard auto insurance policies generally cover the car’s market value at the time of the claim. This means you can end up with an out-of-pocket expense depending on how old your car is and how far along you were with your payments. Taking out gap insurance is an option to consider since it pays for the difference between the car’s value and reamining balance of the loan or lease.

Is picking a car based on the monthly payment bad?

Picking an auto loan based off of monthly payments can be convenient when factoring it into your current budget, but it leaves out a lot of important long-term factors. Monthly payments can get out of hand, and if any unexpected emergencies come up that disrupt your monthly budget, it can become difficult to make payments. With a record 6.3 million Americans 90 days late on auto loan payments, there is a problem with advertising car financing based on monthly payments, as falling behind can lead to long term debt.

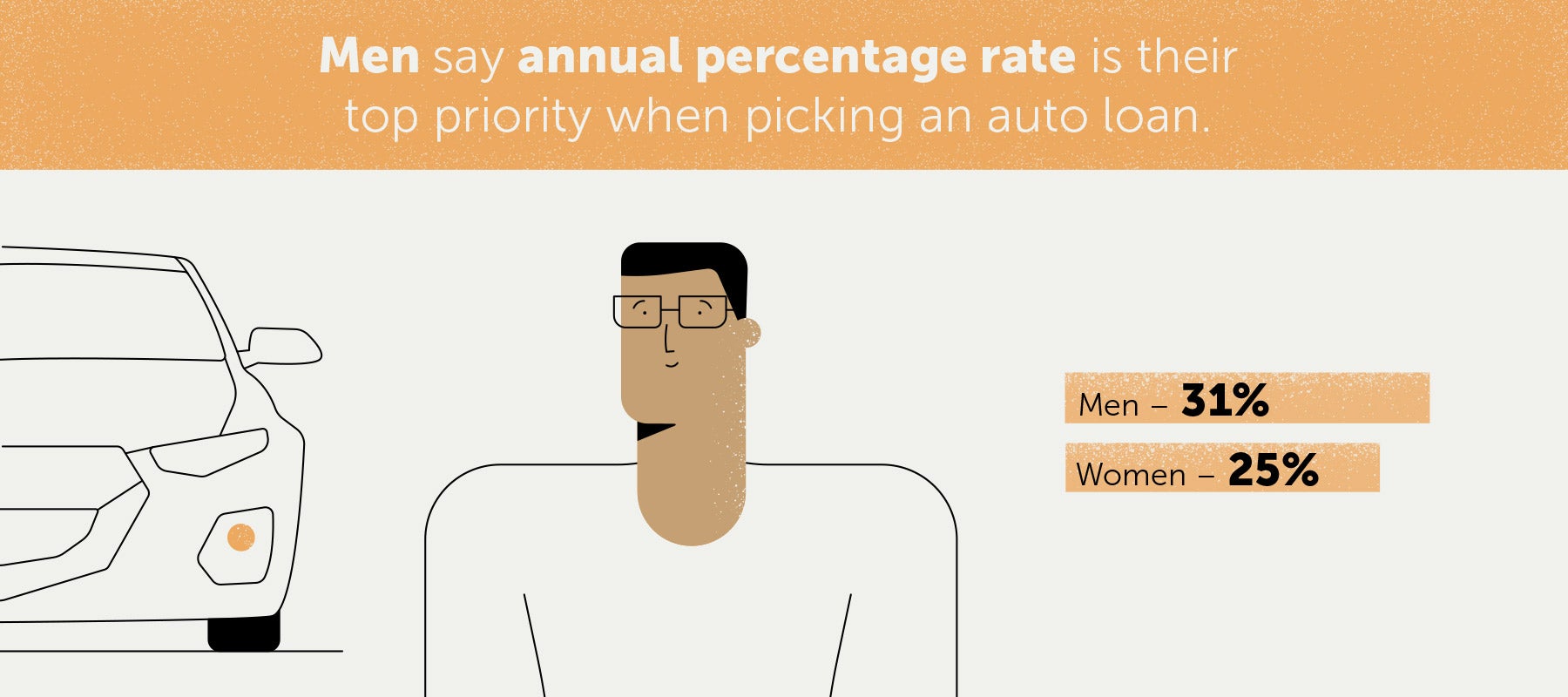

Our poll also found that men are more likely to pick an auto loan based off APR. 31 percent of men responded that APR was the most important factor of their choice, whereas only 25 percent of women responded the same way.

Annual percentage rate is a good measurement when comparing auto loans, but it still leaves out the important factor of length of term. A lower APR could come with a longer length of term, therefore it does not completely show you your total cost.

As auto loan debt climbs in America there is a growing need to promote proper lending education and best practices. For the 25 percent of Americans who take out subprime loans to finance a vehicle purchase, there are other options to lower your total interest paid.

Getting a loan with bad credit can lead to a higher annual percentage rate and a higher total interest paid. Anyone taking out an auto loan to finance a vehicle purchase must remember it’s important to take steps to research your credit options first. This will help you make the smartest financial decision when taking out an auto loan or making regular car payments to keep you out of debt.