The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

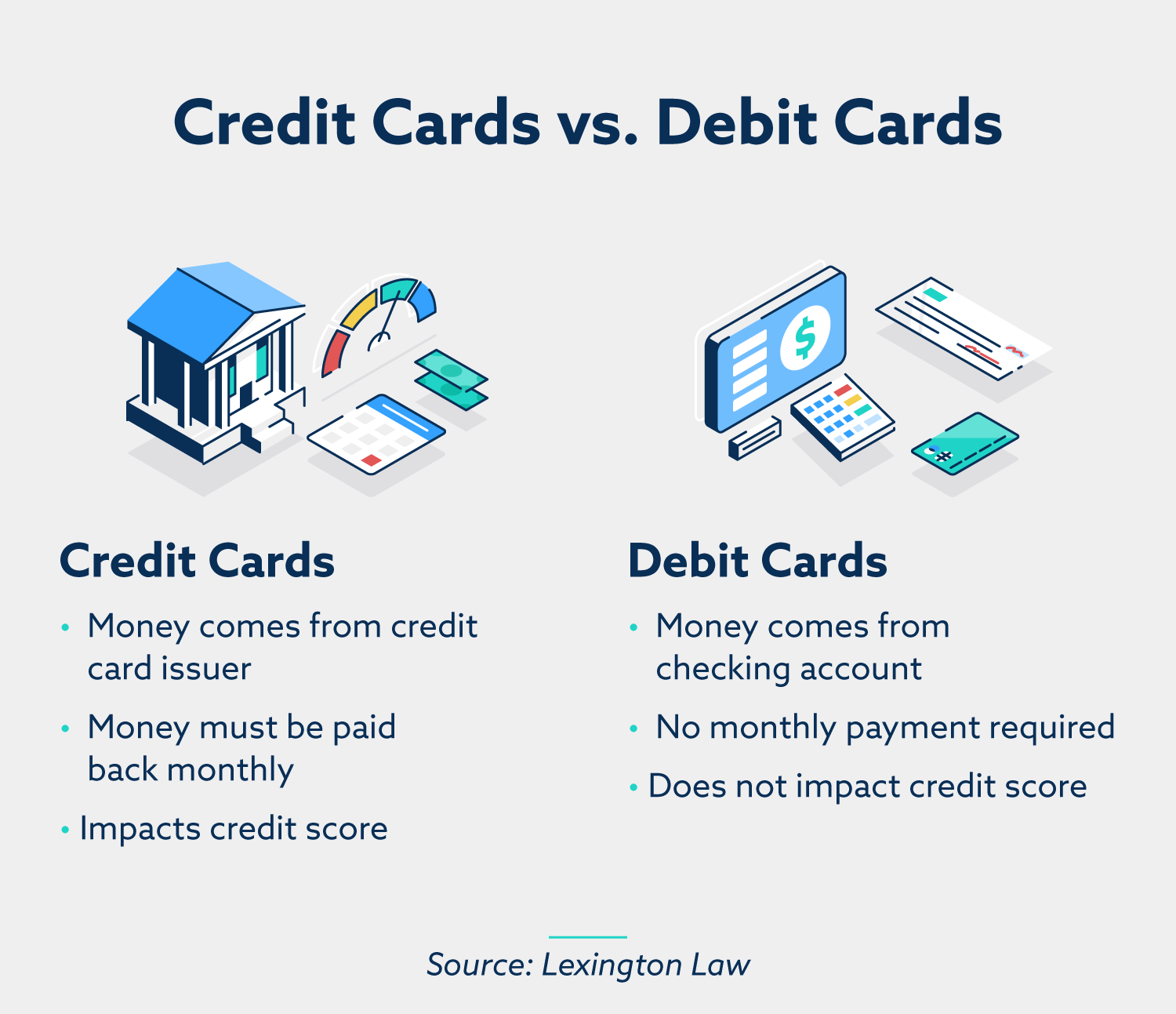

Debit cards use money from your checking account and have no monthly payment or impact on your credit score. Credit cards use money from a credit card issuer that must be paid back monthly and will impact your credit score.

On the surface, debit and credit cards are identical. Both have 16-digit card numbers, expiration dates and magnetic stripes. Both are convenient ways to make purchases online and in stores. But beyond these similarities, debit and credit cards are two very different things.

Understanding the difference between debit and credit is an important part of financial decision-making. With this knowledge, you’ll be well equipped to make the right choices for your spending needs. Here’s a quick guide to the differences between debit and credit.

What is a debit card?

A debit card is a type of payment card that’s linked to your checking account. When you make a purchase, money is deducted from the account in real time. Debit cards are a convenient way to make use of money from your checking account without having to carry cash.

Most debit cards come with low or no fees, but this depends on your bank’s policy. Occasionally, banks will charge a fee if the card is used infrequently, if the checking account is below the minimum balance or if your account has overdraft protection.

Debit cards also come with varying degrees of fraud protection. If your card is lost or stolen, most banks will cancel your card as soon as they’re notified. If money is stolen from your account, making a claim will prompt your bank to investigate the matter, but this process can be lengthy.

How to get a debit card

Debit cards are distributed directly through your bank. To obtain one, you’ll first need to sign up for a checking account. This usually requires you to share some personal information with the bank and deposit an initial balance.

After setting up your checking account, your debit card should arrive in the mail. Once you’ve activated it, you can use it to make purchases in stores and online.

Debit card pros and cons

Debit cards are appealing to users in many ways—above all, their practicality. They don’t come with high interest rates or annual membership fees. And because they use the funds already stored in your checking account, there’s no need to open a line of credit. Plus, there’s the added benefit of accessing the funds in your account without withdrawing cash from an ATM.

However, relying on your own checking account can also be a hindrance. If you need to make a purchase but don’t have the funds ready and waiting, you may not be able to complete the transaction. And while many debit cards are equipped with some form of fraud protection, it’s typically your responsibility to alert the bank of any suspicious activity. Otherwise, you may have trouble restoring stolen funds.

What is a credit card?

A credit card is another form of payment card issued by a financial institution, most often a bank. It gives the user access to a line of credit they can borrow from. As a cardholder, you agree to pay the borrowed funds back plus interest, but the exact terms will vary according to the bank’s terms.

Credit cards often come with fees attached, both to ensure the institution profits from the deal and to charge the borrower for the card’s benefits. These fees are measured through your annual percentage rate (APR), which clarifies the price you pay each year to borrow money.

To illustrate this, let’s say you have an APR of 17.99 percent and an outstanding balance of $500. APR is calculated using a daily periodic rate, which can be found by dividing the rate by 365—in this case, 0.00049. Multiplying this number by your current balance brings your daily periodic rate to $0.25, which can add up to quite a bit if you consistently have an outstanding balance.

Credit cards also come with built-in card protection. Unusual activity may cause your card to freeze until you manually approve the transactions, a useful safety net against theft. As with debit cards, it’s up to you to alert the company if unfamiliar activity appears on your account.

How to get a credit card

Credit cards aren’t attached to your checking account and must be applied for. When you apply for a credit card, you’ll be asked to provide some personal information, along with details about your income and credit history. Lenders use this info to predict what kind of borrower you’ll be and assess the risk they’ll assume by lending to you.

A variety of factors will influence your chances of being approved for a credit card. These include:

- Credit history or lack thereof

- Credit score

- Payment history

- Income

- Outstanding loan balances

- Employment history

Because lenders want to ensure you’ll be able to repay what you borrow, anything that increases your risk as a cardholder can lower your chance of approval. This means a poor credit score, history of missed payments and low income can all influence the decision.

If your application is rejected, you can always apply for a different card. However, it’s a good idea to wait a bit before reapplying, as too many hard credit inquiries can damage your credit score. While you wait, consider addressing the factors that led to the rejection in the first place, either by paying your outstanding balance or finding a credit repair service.

Credit card pros and cons

Credit cards can come in handy as they eliminate the need to pay up front. This is especially useful for larger purchases that would take a significant portion of your checking account. Many credit cards also accumulate rewards and points as you spend. These can be redeemed for discounts, cash back or even travel perks. And credit cards are one of the easiest ways to build good credit. Making regular payments and keeping your credit utilization rate low can help your credit over time.

Because your credit card uses funds borrowed from the bank, the bank has a greater interest in the card’s protection than it would for a debit card, which uses money that belongs to you. Government regulations like the Fair Credit Billing Act mean you’ll be liable for few or no fraudulent transactions that occur in the event your card is stolen.

But credit cards can also be a double-edged sword. Just as they can improve your credit, they can also lower it through missed payments and high outstanding balances. This is especially true when you’re managing multiple cards, as it can be easy to spend too much without being able to quickly pay it back. And with interest rates and fees to keep track of, credit cards can be quite expensive to use.

Debit, credit and your credit score

Debit cards generally don’t have much effect on your credit score. Because the money in use already belongs to you, there’s no credit-related activity taking place. Exceptions can occur, such as in the case of unpaid overdraft fees. If these go unpaid for too long, they’ll be reported to credit bureaus.

Credit cards, on the other hand, can have a significant impact on your credit. Essentially, everything you do with your credit card can affect it, either positively or negatively.

One of the most common influencing factors is a history of making late payments—or skipping them altogether. Payment history affects an estimated 35 percent of your FICO® credit score, meaning even a few missed payments can cause a shift. This may also reduce your chance of being approved for any new cards, as lenders may see this history as a risk. A high credit utilization ratio can have a similar effect. A good rule of thumb is to keep this number below 30 percent of your spending limit.

It’s common for people to have a mix of debit and credit cards in their wallets, but the right blend will depend on your own needs and goals. If you’re looking to improve or establish your credit history, applying for a credit card might be a good idea. But if you already have a handful of cards and are having trouble managing them all, focusing on credit repair is likely a better option.

The difference between debit and credit, explained

Both debit and credit cards are useful tools to have in your financial repertoire. Knowing when to use each one can help you make smart spending decisions and build better money management habits. Here are a few key takeaways to keep in mind as you navigate your own debit and credit use:

- You can obtain a debit card through any bank where you have a checking account. Credit cards must be applied for, and approval is granted based on an assessment of your financial history.

- Debit cards are linked to your checking account, while credit cards utilize borrowed funds issued by a financial institution.

- Debit cards usually have no effect on your credit, while credit cards can affect it significantly.

Want to learn more about managing your credit? Our team at Lexington Law is here to help. Take our free credit assessment today to check your report and start achieving your credit goals.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.