Being credit invisible means having no data on your credit report, which can stop you from accessing credit due to not having a credit score.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

When a person is considered credit invisible, it means they don’t have access to credit due to not having a credit score. According to this 2022 study on access to credit (which makes its estimates based on data from the 2015 CFPB report), there could be 28 million credit invisible Americans and another 21 million Americans who are unscorable. Let’s review what it means to be credit invisible and what you can do to fix the problem.

What is credit invisibility, and why does it matter?

Credit invisibility refers to when a person doesn’t have a credit score because they have no data on their credit report. Credit reporting bureaus use the information that’s available regarding your payment history, income, outstanding loans and other factors to create a score lenders can use to gauge your creditworthiness. If you don’t have a credit score, lenders don’t know how much risk they’re taking on by agreeing to lend to you.

Most people who are credit invisible have never had credit before. They’ve never been approved for a credit card, car loan, personal loan or mortgage. Due to their lack of credit history, lenders will receive a blank report when they check a credit invisible person’s credit.

Credit scores generally range from 300 to 850, and a FICO® score above 670 is considered good. As your credit score improves, you can gain more access to credit and have the opportunity to save thousands of dollars in interest on car loans or mortgages. With no credit score at all, many lenders will either turn you down for a loan or charge outrageous interest rates.

Being credit invisible vs. being unscorable

Someone who’s credit invisible has never applied or been approved for credit before. Most credit invisible people either are young, have immigrated to the United States or don’t have enough income to apply for credit. Being unscorable is similar to being credit invisible but means you have a very thin credit file rather than no file at all.

Someone who’s unscorable may have a couple of active accounts that are less than six months old, so the credit reporting agencies have little information to base a score off of. It’s also possible for people to become credit invisible or unscorable even if they once had a credit score. This can happen if they stop seeking credit and close all their accounts that report to the credit agencies and then seven or more years pass.

The unfortunate reality is that people who show up as credit invisible or unscorable have little or no access to credit even if they didn’t do anything wrong, such as missing payments or having something repossessed. A lot of people who are attempting to establish a credit profile get frustrated because it feels as though they need to obtain credit before they can qualify for credit.

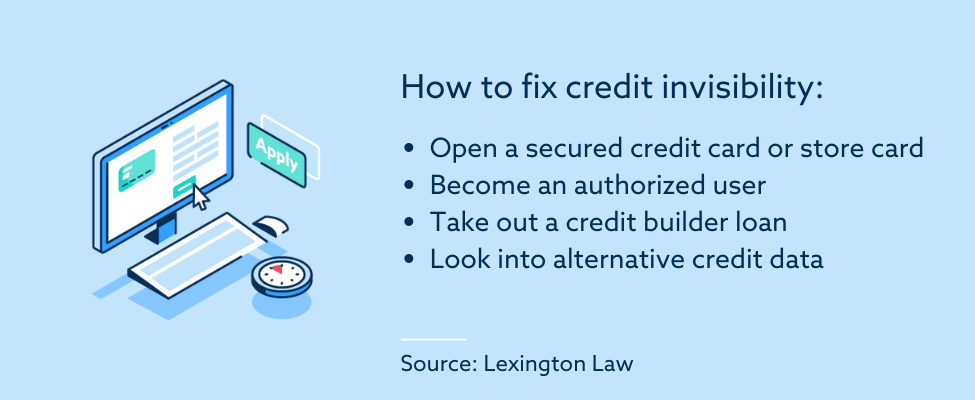

How to fix the problem of credit invisibility

If you’re trying to establish credit, the first thing you need is patience. It can take some time for the things you do to show up on your credit file, so even if you’re able to open accounts and begin making payments on them, your score might not be impacted immediately. Depending on the type of accounts you have, it can take up to six months for a new credit card or loan to show up on your credit report.

The traditional way to obtain credit when you’re credit invisible is to get someone to cosign on your first loan, but this isn’t an option for everyone. Cosigners take a risk because if you default on your payments, their credit could also suffer. Luckily, if you can’t find a cosigner or don’t feel right about asking someone to assume risk on your behalf, there are more options for building credit.

Open a secured credit card or store card

Secured credit cards work in the same way a secured loan would. When a loan is secured, it means there’s collateral that the lender can take if the borrower doesn’t make their payments. When you apply for a secured credit card, you’re almost guaranteed to be approved as long as you have a checking account and can put a security deposit down on the card.

Most secured credit cards ask for $200 to $300 down and offer you a credit line equal to your security deposit. If you’re trying to establish credit, you should open one or two secured credit accounts and use them for small purchases only. To avoid paying interest, pay off the entire balance each month.

One of the reasons you shouldn’t spend a lot of money on these cards is that your credit utilization impacts your overall score. It’s a general rule of thumb to try to keep your credit utilization at 30 percent, which means if your total credit limit is $300, you shouldn’t use more than $90 of your limit.

Store cards are another way to obtain credit and are credit cards that can only be used at specific stores. They may have different approval standards that allow credit invisible or unscorable applicants to open an account with a small limit. As you make on-time payments on secured or store credit cards, your limits will be raised over time.

Become an authorized user

An authorized user is someone who’s able to make purchases on a credit account that belongs to someone else, such as a credit card. If you’re able to become an authorized user on a friend or family member’s credit card, it can help your credit file, especially if the account has a long history and the account has good payment history.

One of the five credit scoring factors is the age of your accounts, so being an authorized user on an old account can potentially give you a boost, even if you never actually use the credit card yourself.

Take out a credit builder loan

Some banks have programs that are specifically for people who are looking to establish or rebuild their credit. The downside is that if you take out a credit builder loan, you’re going to pay much higher interest rates than someone with good or excellent credit. To limit the impact, try to only take out smaller loan amounts and then pay off the loan each month.

Your record of on-time payments will establish your credit and show you’re creditworthy in the eyes of other lenders. This is a good way to eventually get approved for a bigger loan.

Look into alternative credit data

One assumption a lot of people make is that utility companies and landlords report payments to the credit bureaus, but they don’t usually do this unless they’re asked to. There are several services your landlord or property management company can use to report your payment history, and it may give you a decent credit score boost. Investigate ways you can use alternative credit data to your advantage.

Understand how credit works and start building it

If you’re credit invisible or unscorable, make sure you understand the five credit scoring factors that determine your score so you can take action to build credit in these areas:

- Payment history

- Length of credit history

- New credit requests

- Total credit utilization

- Mix of credit types

It’ll take time to work on your length of credit history, but there’s plenty you can do in the meantime. The first step is to get a copy of your credit report to see if you have credit history and if you’re likely scorable or not, as well as to see what lenders see when you apply for credit. Educating yourself on how the credit-building process works can guide you on what to do next.

Lexington Law has resources available that can help by guiding you through the most effective strategies to build your credit. We can also help you determine if there’s inaccurate information on your credit reports and address errors that could be holding you back. Learn more about how we can help today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.