The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

If you plan on applying for a mortgage, building your credit to buy a house is an essential step toward loan approval and a lower interest rate.

Purchasing a home is huge milestone for most people—but it’s also a considerable investment requiring extensive planning, research and credit. For those that have yet to start building their credit to buy a house, being approved for a mortgage can be next to impossible.

A good credit history helps lenders decide whether to trust that you’ll make your loan payments on time. Your credit score reflects your credit history—the higher the score, the lower your loan interest rate will likely be. If you need a head start improving your credit to make your homeowner dreams a reality, here are a few tried and true methods to consider.

1. Monitor your credit

Credit monitoring allows you to stay on top of changes to your credit so you can track your progress, identify potential errors and address any suspicious activity. The last thing you want is a hacker stealing your identity and opening fraudulent accounts in your name.

If you just started your credit journey, it typically takes six months to generate your first credit report and credit score. You may be able to track changes to your credit score using your mobile banking app or our credit snapshot service, which provides a free credit report summary, credit score and personalized repair recommendations.

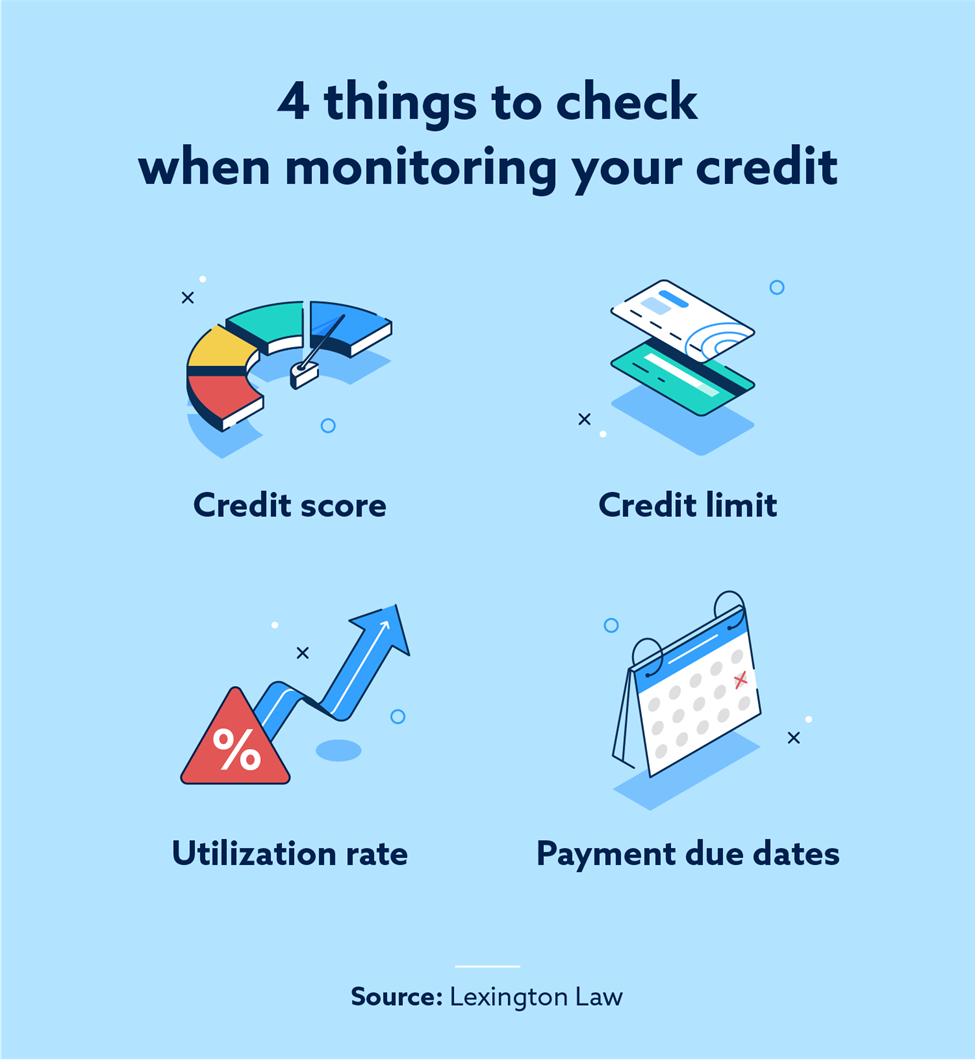

Credit building requires due diligence—don’t just track your credit score, but also learn the ins and outs of how credit works so you can stay on top of things. For example, you want to understand the following concepts:

- Your credit limit: A high credit limit can be good for your credit. If you’ve been making all the right money moves, you may be able to request an increase.

- Your utilization rate: Calculate your credit utilization rate by dividing the amount of money you owe by your credit limit. Try to keep your utilization rate below 30 percent.

- Payment due dates: Late payments can seriously ding your credit, so make sure you’re paying your bills on time.

Check your accounts daily to grasp your spending habits and identify areas that may need improvement.

2. Review your credit report for errors

A 2021 study found that one out of three volunteers had at least one error on one of their credit reports, so it’s important for you to regularly review your credit report. Once a year, consumers can receive a free credit report from each of the three major bureaus.

Not all lenders and creditors report to all three credit bureaus, so the information on your reports may vary from bureau to bureau. This means that your score may also vary across bureaus, as your score is based on the information in your report.

One thing to keep an eye out for are errors that could be bringing your score down, such as:

- Inaccurate missed payment dates

- Inaccurate dates of late payments

- Inaccurate balances

- Inaccurate dates an account was opened or closed

Addressing errors on your credit report is a must if you’re serious about improving your credit. If you discover any mistakes on your credit report, follow these steps to dispute your credit report:

- Fill out the credit bureau’s dispute form if they have one.

- Collect copies of documents that support your claim, and keep a record of everything you send.

- Draft a short letter detailing the error and the evidence you included to dispute it.

- Send your letter and supporting documents by certified mail to the bureau’s consumer dispute center. Pay for a “return receipt” so you have proof the bureau received it.

Once the credit bureau receives your dispute, they have 30 – 45 days to investigate it. If they deem the request “irrelevant,” they’ll have to contact you to explain why they stopped investigating. If the bureau acknowledges they made a mistake, they must:

- Send you the results in writing, as well as a free updated copy of your credit report

- Send notices of the corrections to anyone who may have accessed the report in the last six months, such as potential lenders, landlords or employers

3. Pay off any delinquent accounts

It’s easy to fall into the “out of sight, out of mind” habit when managing your credit payments, and a utility bill or car payment can occasionally slip through the cracks.

Your credit payment history makes up the greatest percentage of your FICO credit score (35 percent), so delinquent accounts—payments reported to one or more credit bureaus as 30+ days late—should be paid off as soon as you notice them.

Delinquent accounts reported on your credit indicate to lenders that you’ve broken the terms of your contract to pay the money back—it’s not a good look if you want to apply for a mortgage. Even a payment that’s only 30 days late can show up on your report for up to seven years.

If you’re serious about building your credit to buy a house, monitor your credit report and accounts regularly to spot and pay off delinquencies before they’re reported. You may be hit with a late fee, but late payments likely won’t be reported as delinquent if they’re less than 30 days overdue.

4. Choose the right credit cards

Securing a credit card and using it responsibly is a quick and effective way to start building your credit. However, not all credit cards are created equal. Some types of credit cards, such as secured cards or joint cards, are designed to help people with bad or limited credit boost and strengthen their scores over time.

| Type of Credit Card | |

|---|---|

| Secured Card | Requires an upfront payment to act as collateral if you can’t pay your balance |

| Student Card | Allows students with little to no credit history to begin building their profile, but usually with a lower credit limit. They may also offer incentives for good grades and cash back on everyday purchases |

| Starter Card | Helps people with little to no credit history build a credit profile, but they typically don’t offer great rewards programs or cash back incentives. They also come with high interest rates |

| Joint Card | Requires two parties to apply together to start credit, and they are both equally responsible for paying off the balance |

| 0% APR card | Doesn’t require the borrower to pay interest on new purchases for a set period, making it easier to pay off big purchases and save money on interest |

| Starter Card | Helps people with little to no credit history build a credit profile, but they typically don’t offer great rewards programs or cash back incentives. They also come with high interest rates |

| Balance transfer card | Offers temporarily low introductory rates—but specifically for balance transfers |