The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

There are various ways to build credit for your child, like adding them as an authorized user or cosigning on a loan with them. It’s also helpful to begin credit education early and to start building their credit as early as possible.

A 2022 report from Experian showed that Gen Z has the lowest average FICO credit score at 679, which is lower than the average score of every other generation. While it’s true that it takes time to build a great credit score, what if your child’s credit could be above average as they transition into adulthood?

Credit scores are a signal of financial health and stability, and they also impact how much money you’ll either save or have to spend in various aspects of life. For example, the average car loan interest rates are much higher for those with lower credit scores.

Here, you’ll learn at what age you can start building credit and how to start building credit for your kid. This will help set them up for financial success while also learning how to maintain a great credit score when they’re out on their own.

At what age can you start building credit?

There’s no legal minimum age to start building credit. Your child can start building credit in high school or even when they’re much younger. While your child can’t go out and sign up for credit cards on their own at such a young age, there are several ways for them to begin building credit. Below, we’ll go over a wide range of options for you to help your child begin building credit at any age.

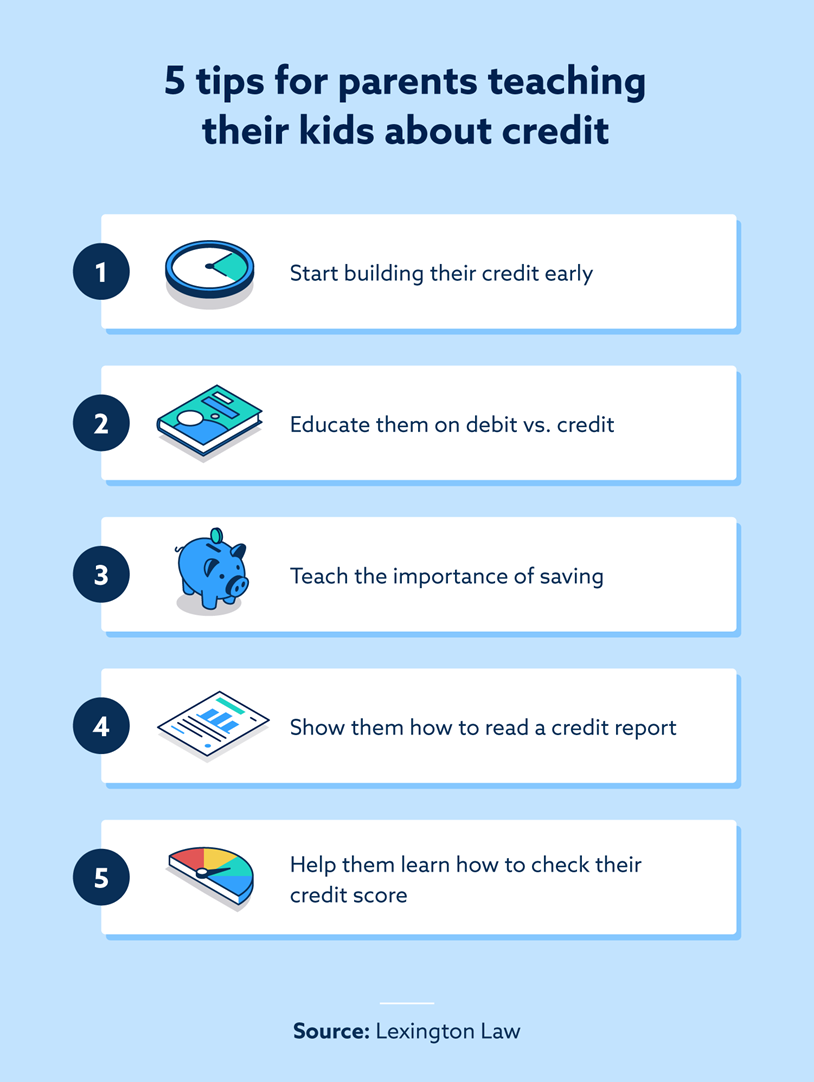

1. Build credit sooner rather than later

One of the best things any parent can do for their child is help them start building credit as early as possible. The FICO credit scoring model is what most lenders use when approving or denying applications, and the length of credit age accounts for 15 percent of a person’s overall credit score. Having older lines of credit can help people reach higher credit scores.

This also allows you to teach your child about credit early. Understanding and managing credit teaches young people the importance of financial literacy and responsibility, which are great skills that can be used throughout a person’s life.

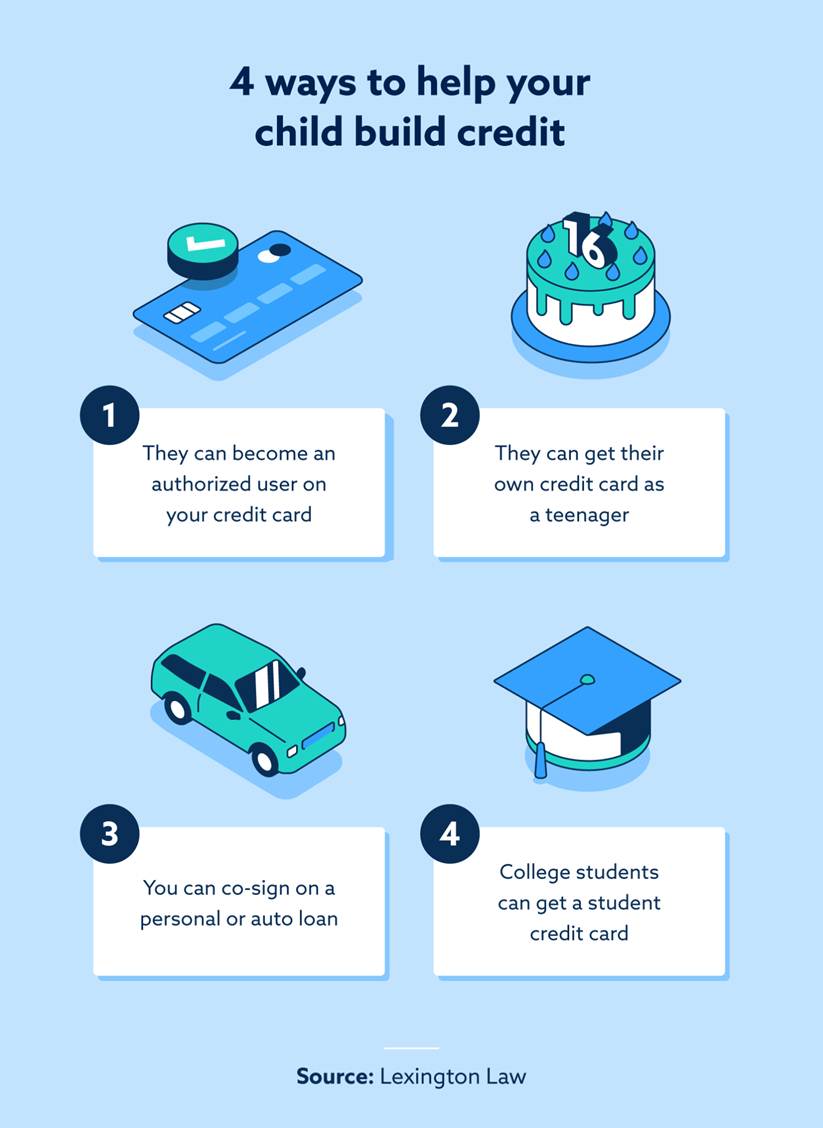

2. Add your child as an authorized user

The most common way to build credit for kids is to add them as an authorized user on your credit card. Whether they’re a young child or a teenager, you can add them to your account so they can begin building credit. Basically, becoming an authorized user allows them to “piggyback” on your credit. Making on-time payments with low credit utilization builds your credit and also benefits your child’s credit.

Some banks and financial institutions let you open a credit card account for kids, but depending on the bank, they may need to be a teenager first. If you start teaching your child about credit early, they’ll be better prepared to manage a credit card once they’re ready to have their own.

3. Teach the importance of saving

It’s difficult to pay your credit card bill if your bank account is empty when the bill is due, which is why understanding the importance of saving at a young age is beneficial as well. Budgeting and saving money together can help your child develop positive habits for managing their finances.

If your child does chores, you can find ways to incentivize saving money. Children often want to spend money as soon as they get it, so one way to incentivize saving is to mimic a 401(k) employee match program. For example, you can tell them that you’ll match 50 percent of what they save up to 5 percent of their monthly allowance. Show them on paper how it would look for them to save money and how much additional money they’ll make by simply saving some.

4. Help them get a secured credit card

A secured credit card is a great way for young people to start building credit without needing to meet the higher qualifications needed for a regular credit card. Secured credit cards allow you to deposit money with a bank, and then that amount is used as your credit limit. As you use the credit card and pay the money back, it gets reported to the credit bureaus to help raise your credit. To open a secured credit card account, you often need to be 18, but this is an option for parents who prefer not to add their child as an authorized user or want to wait until the child is older. If you taught them the importance of saving, they should have plenty saved up to open one of these accounts when they’re 18.

5. Have them get a credit builder loan

A downside of being a young adult trying to build credit is that you don’t have any credit history, and this is why credit builder loans are helpful. Credit builder loans are specifically for people with no credit, and your child can get one of these loans once they’re 18.

One major benefit is that young people don’t need a cosigner for credit builder loans, but there are also some drawbacks. Credit builder loans often have higher fees and interest rates, but they can help young people build credit and receive lower rates once they have a good credit score.

6. Cosign on a personal loan

Personal loans have better interest rates and lower fees than credit builder loans. Still, without a good credit score, your child will most likely need a cosigner. Cosigning is similar to adding your child as an authorized user because they benefit from your established credit. They can take out a personal loan for a small amount, and as they make their monthly payments, it can help boost their credit.

7. Cosign on a car loan

Many young people dream of driving their own car as soon as possible, and you can help them accomplish that while building their credit score if you cosign on an auto loan. This is for young people 18 and older, allowing them to qualify for a loan based on their credit history. If they make their regular payments, they may be able to raise their credit enough that they can get their next vehicle without a cosigner.

8. Teach the difference between debit and credit

Teaching the difference between debit and credit is something you can do with children of any age. There are pros and cons to debit cards and credit cards, and your child can benefit from learning the situations where they need to choose between debit and credit. It can also help them understand when they may need to tap into their savings.

You can educate your child at a young age is if they ask to borrow money. You can treat the loan like a regular loan where your child will have to pay interest, much like a credit card. Many credit cards also offer perks like 0 percent interest if the loan is paid back in a certain amount of time, so you can help incentivize your child to pay you back as soon as possible. To practice using debit, you can have your child keep their spending money in one piggy bank and their savings in another.

9. Show them the benefits of additional credit reporting

As you educate your child about how credit and credit scores work, it’s helpful to teach them about what does and doesn’t get reported. For example, in most cases, paying your rent and utility bills on time doesn’t get reported to the credit bureaus. Many people don’t know that there are services that report rent and utilities to provide additional ways to build a person’s credit.

10. Encourage your young adult child to get a student credit card

Many banks and financial institutions offer student credit cards, which are great for kids starting or already in college. If you’re a student, these cards are much easier to qualify for because you don’t need a great credit score or long credit history. Some of these cards even offer perks like cashback offers while helping your child build their score.

Building credit for your child FAQ

Below, we’ve answered some of the most frequently asked questions about how to help kids start building credit.

Are there any downsides to adding my child as an authorized user or cosigning on a loan with them?

Yes, potentially. When you become a cosigner or add your child as an authorized user, your credit can be affected by the other person’s behavior. This means if there are late payments or other derogatory marks, both people’s credit can be affected.

How can I build my child’s credit?

You can start building credit for your child by adding them as an authorized user at a young age, opening a credit card in their account when they’re a teenager and cosigning on a loan for them.

How do you check your child’s credit report?

You can check your child’s credit report for free through AnnualCreditReport.com or request a copy from the major credit bureaus. It’s also helpful to note that the Federal Trade Commission (FTC) suggests checking your child’s credit report when they turn 16.

Also note that credit scores are based on the information in credit reports, but you won’t find a score on a credit report—you will have to look elsewhere to find the credit score itself.

At what age should a child start building credit?

A child can start building credit at any age, but they generally have to be 18 to open a credit card account on their own.

Can I add my child to my credit to build their credit?

Yes. You can add your child as an authorized user on your credit card account. This helps them build credit and allows you to start teaching them about credit at a young age.

Can I put a credit card in my child’s name?

Yes. Some banks allow parents to open credit accounts for their children once they’re roughly 15 years old.

The importance of monitoring your child’s credit

The FTC recommends that you check your child’s credit report before they turn 18, and this is due to credit card fraud and identity theft.

A 2021 report from the FTC shows almost 390,000 cases of identity theft involving credit card fraud, which typically means a person opened a credit card account with a stolen Social Security number. Often, these are the Social Security numbers of children.

By monitoring your child’s credit, you can help catch identity theft before there are negative consequences. You can also sign up for Lexington Law’s services to learn more about credit and get your own free credit assessment today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.