While a successful dispute with one credit bureau may eventually lead to the information being removed by the others, it’s recommended to file a dispute with each bureau that has inaccurate information on your report.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

If you find inaccurate information on your credit report, you’ll want to file a dispute as soon as possible. Each of the three credit bureaus—TransUnion®, Experian® and Equifax®—provides its own credit report, so it’s best to check which of the bureaus is reporting the inaccurate information.

While a successful dispute with one credit bureau may eventually lead to the information being removed by the others, it’s recommended to file a dispute with each bureau that has inaccurate information on your report.

By checking your credit reports regularly, you’ll be able to quickly spot inaccurate information—like a credit card you never opened or a closed loan that’s listed as open. Initiating a credit dispute is the most effective way to get those inaccurate items removed, which may lead to an increase in your credit score.

Keep reading to find out more about why you may want to file a dispute with the credit bureaus, as well as an overview of the dispute process.

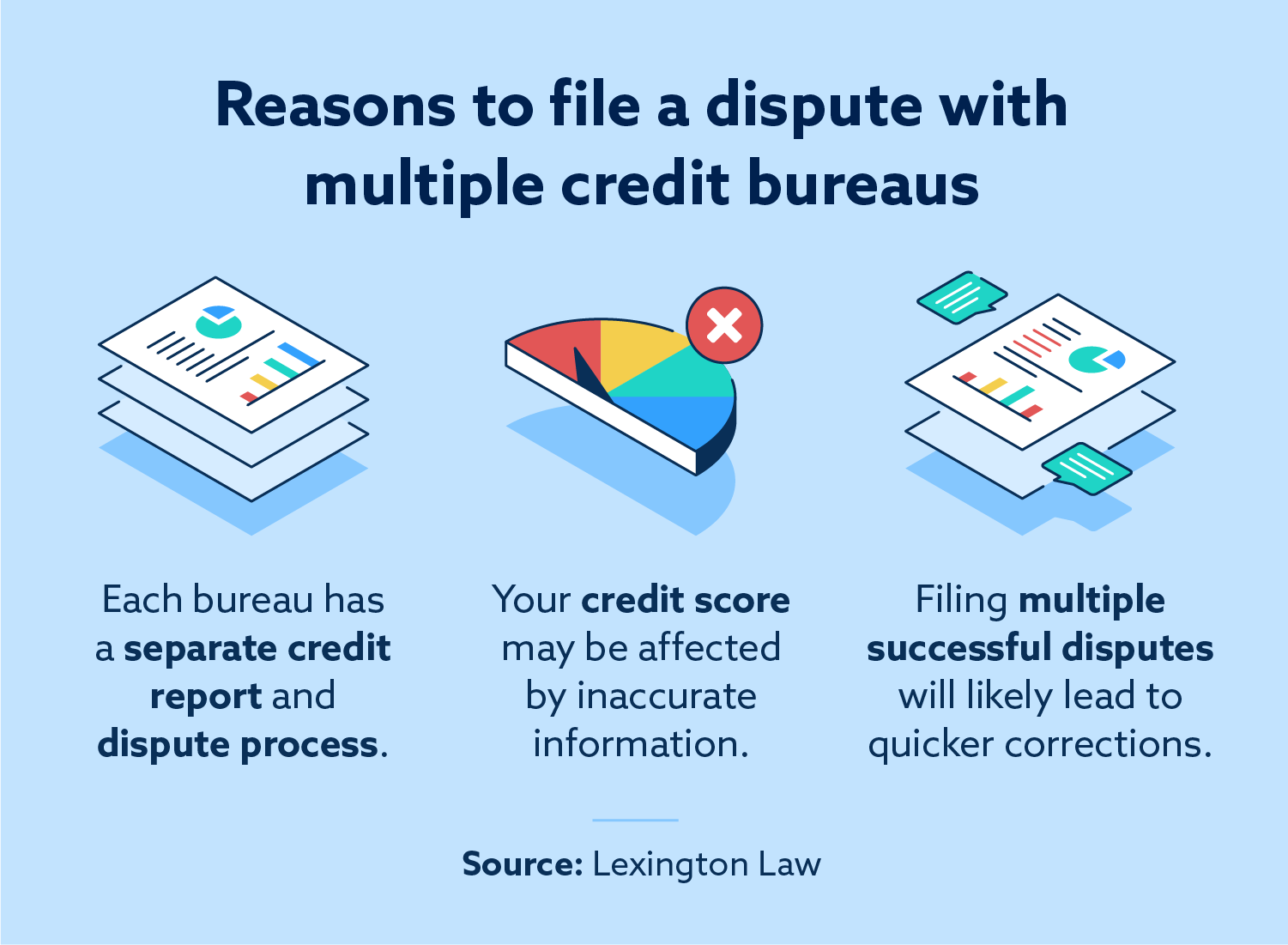

Reasons to file multiple credit disputes

Each of the three credit bureaus—TransUnion, Experian and Equifax—keeps a credit report with information about you. However, not all creditors report to all three bureaus, and the credit bureaus do not share all of their information. As a result, any inaccurate information you find on one credit report may or may not be on the others—you’ll need to check each report individually.

Fortunately, you are able to request a free credit report every 12 months from each of the credit bureaus.

If you find inaccurate information on more than one of the credit reports, you’ll want to file a dispute with each credit bureau that is reporting the inaccuracy.

Although the credit bureaus have stated that a successful dispute with one bureau is likely to eventually lead to a correction elsewhere, there are several good reasons to file multiple disputes.

Get your score fixed more quickly

When multiple credit bureaus are reporting inaccurate information about you, your credit score may be negatively impacted. Even if the information is removed from one report, it may remain on another.

Since each credit bureau has its own dispute process, you’ll have the best chance of getting your score fixed quickly if you file a dispute with each bureau that is reporting the incorrect information.

Start multiple inquiries with the original creditor

When you file a dispute with a credit bureau, they’ll start an inquiry with the original creditor, who must provide evidence of the information they reported. If you file multiple disputes, each credit bureau will reach out to the original creditor.

With multiple credit bureaus contacting the creditor, they’ll need to provide thorough and timely evidence for the negative item they’ve reported. In the best case, the evidence that you provide could be more substantial than theirs.

Use the same evidence for multiple disputes

The process for filing a dispute is relatively similar with all three credit bureaus, so once you’ve collected your evidence, filing another dispute is usually not difficult.

In other words, if multiple bureaus are reporting inaccurate information that you can disprove with clear documentation, it’s in your best interest to file multiple disputes to get your report corrected.

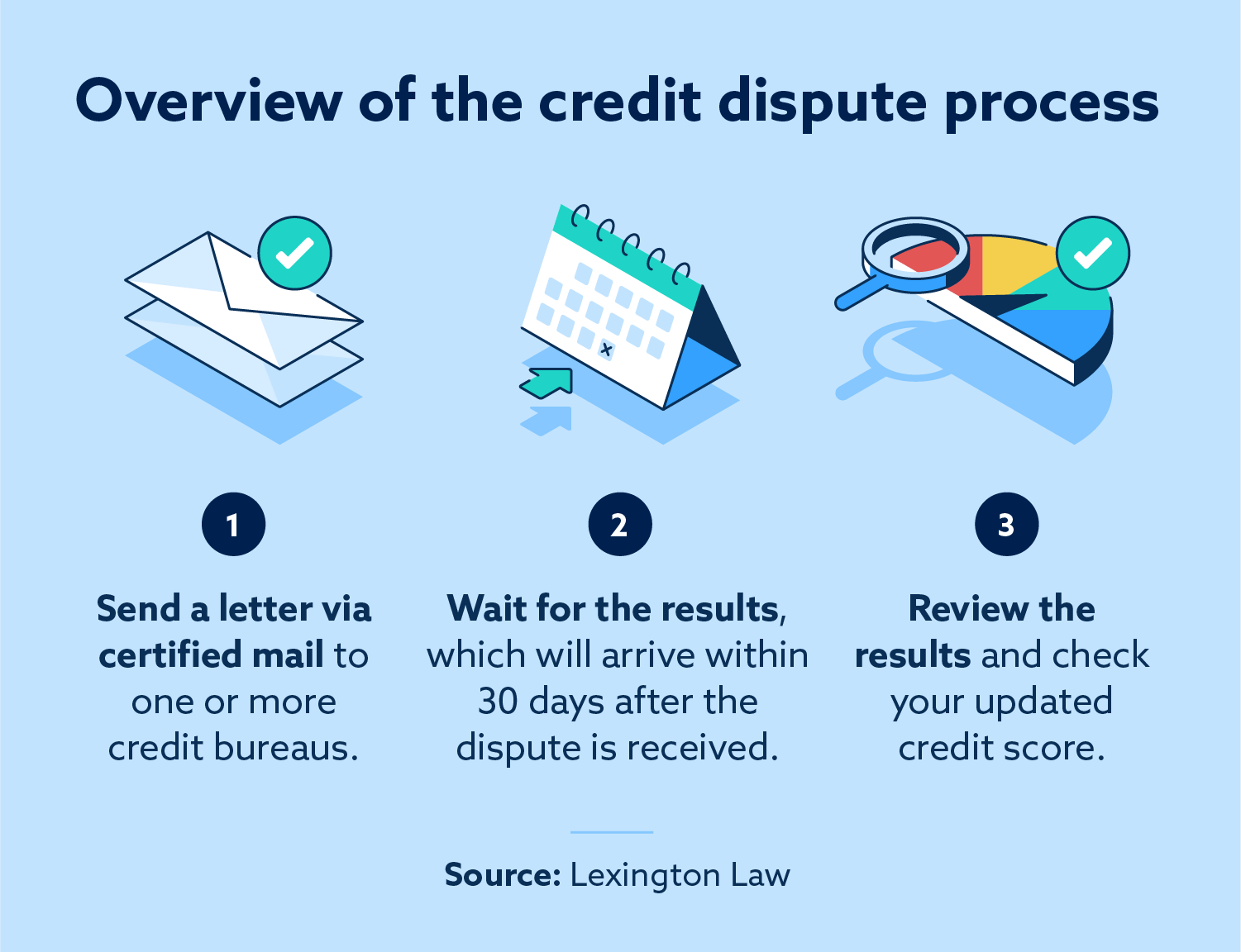

How to file a dispute

Below, we’ve provided a short overview of the credit dispute process. If you’re ready to start a dispute and need a more detailed overview, we’ve written an in-depth guide to initiating a credit dispute that will provide everything you need to get started.

Here are the most important steps when filing a credit dispute:

1. Send a letter via certified mail to one or more credit bureaus

Although it’s possible to start a credit dispute online, the best way to initiate a credit dispute is by sending a letter with certified mail. This approach creates a paper trail, and you’ll know exactly when the credit bureau receives your letter.

The Federal Trade Commission offers a sample letter to help you get started with filing a dispute.

You’ll need to contact each credit bureau separately if you’re filing multiple disputes, and you can use the information below—or visit each bureau’s website for contact information.

| Equifax | TransUnion | Experian | |

|---|---|---|---|

| Online | File a dispute | File a dispute | File a dispute |

| Equifax PO Box 740256 Atlanta, GA 30374-0256 |

TransUnion LLC Consumer Dispute Center PO Box 2000 Chester, PA 19016 |

Experian PO Box 4500 Allen, TX 75013 |

After the credit bureau receives your dispute, they have up to 30 days to investigate, according to the Fair Credit Reporting Act. During this time, you can choose to also file a dispute with the original creditor.

2. Wait for a response

After the credit bureau receives your dispute, they will begin an investigation by contacting the original creditor to request information. However, if the credit bureau determines that you have not provided sufficient evidence for your claim, they may determine that your dispute is “frivolous” and choose not to investigate.

If they do conduct an investigation, they’ll report the results back to you within five days of its completion.

3. Review the results and check your credit score

You’ll receive a letter in the mail that details the results of the investigation. Additionally, you’ll receive a copy of your credit report, which will show either that the disputed item has been verified or that it is now removed after review.

No matter what, you’ll want to check your credit score to see how the dispute has affected your score.

If one credit bureau removes something from your credit report, do the others have to also?

Should you file a dispute with a credit bureau and have an error removed, the other bureaus are not obligated to remove the error as well. Each of the bureaus are separate entities, so you’ll need to file disputes independently and go through the process with the individual organizations.

Each of the companies have different policies and methods when it comes to receiving disputes, so you’ll need to follow up with each one and go through the process. If one or two of the other bureaus don’t agree with the dispute, it may be time to work with a credit repair company that offers legal professionals who will challenge these errors on your behalf. Sometimes, this carries more weight with the bureaus than individuals filing disputes on their own.

If you are unsatisfied with the dispute process or unsure how to get started, contact Lexington Law Firm. We are able to help you assess your credit report for accuracy and file disputes to potentially get inaccurate items removed. This process often has positive effects on your credit score, especially if invalid negative items are successfully challenged.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.