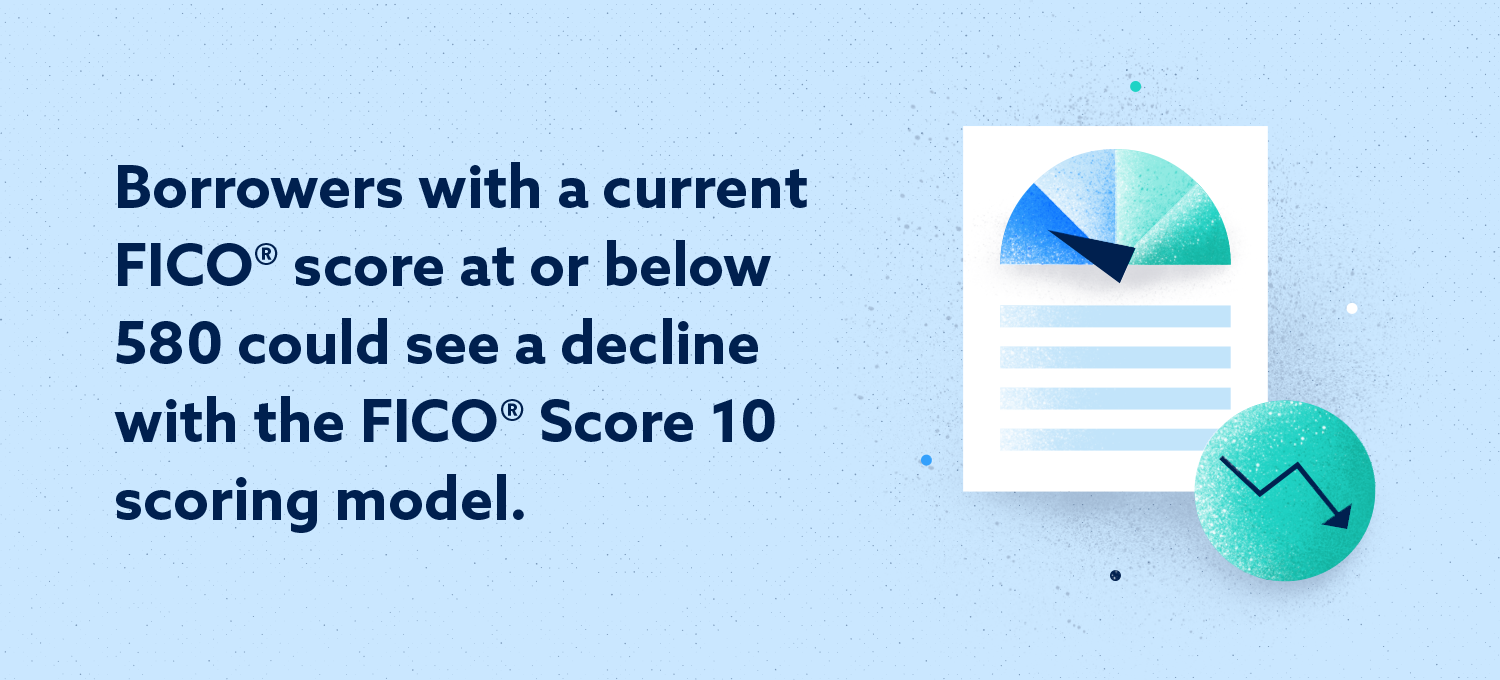

Borrowers will see their credit score improve if they currently have a good credit score, but will see a decline if they’re in a lower FICO® score range, about 580 and below.

The Fair Isaac Corporation (FICO®) recently announced that they will release the new FICO® Score 10 Suite in summer 2020. This scoring model update will include FICO® Score 10 and FICO® Score 10 T.

FICO® says the new suite will have stronger predictive power and use more comprehensive data than previous scoring models. This helps lenders make more precise lending decisions.

For example, FICO® says that lenders can reduce the defaults in their portfolio by 10 percent among newly originated bank cards and 9 percent among newly originated auto loans, compared to using FICO® Score 9.

For consumers, the new scoring model could impact scores and future credit and loan applications depending on both their current scores and credit history. Read through our guide below to learn about the changes with FICO® Score 10 and how they could potentially affect you.

Table of Contents

- What are The New FICO® Scores?

- What Are the Main Changes?

- When Will Lenders Adopt the FICO® Score 10 Suite?

- How Could the Changes Affect Me?

- What Should I Do if I Think My Score Will Be Negatively Affected?

- How Can I Maintain a Good Credit Score During Scoring Model Changes?

What are the New FICO® Scores?

FICO® Score 10 and FICO® Score 10 T are two scores included in the new score suite. We’ll briefly explain the differences between both before diving into the major changes the new suite brings.

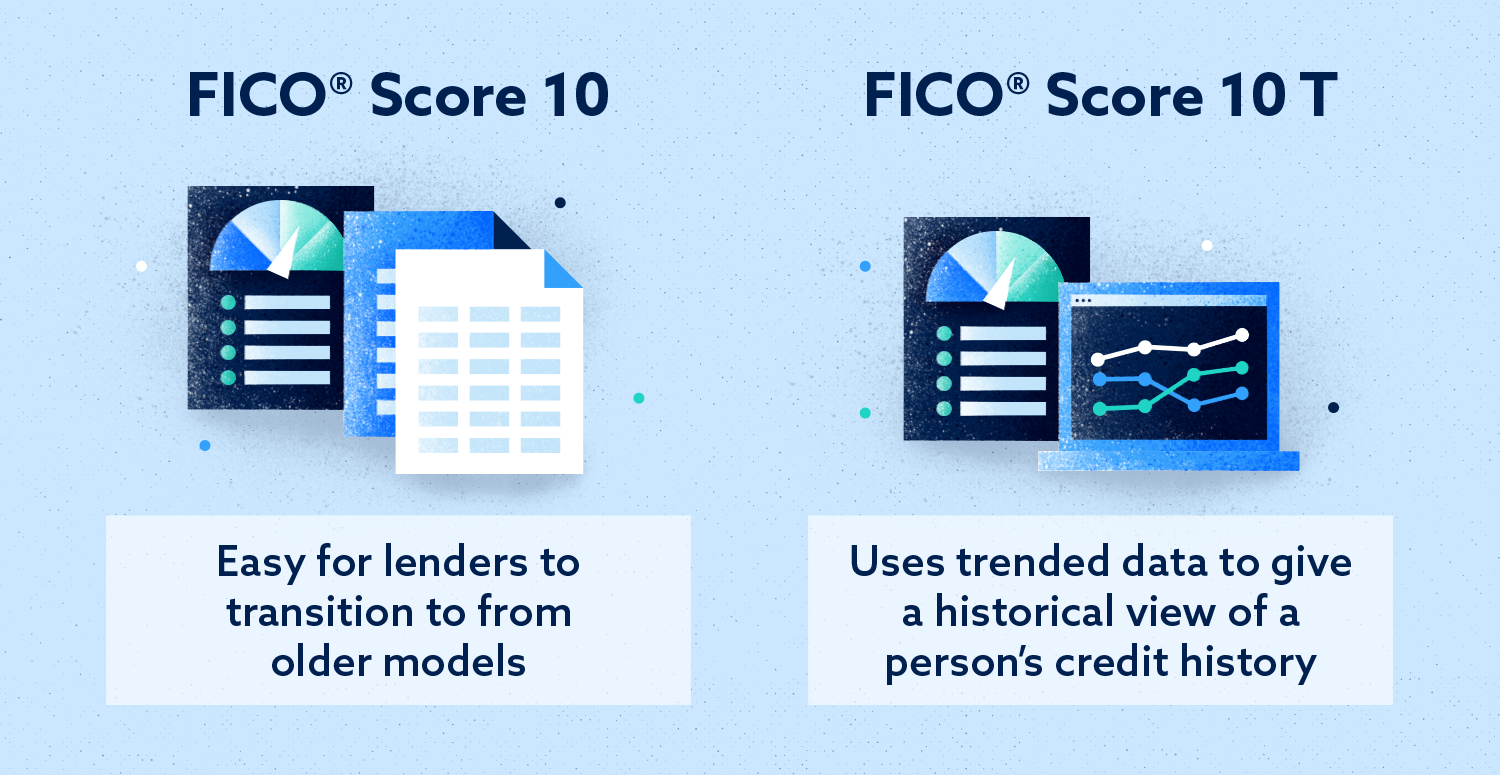

FICO® Score 10

Specifically, for FICO® Score 10, many things have stayed similar to make it easy for lenders to transition from old models. This means the scoring model uses the same reason codes and consistent scoring ranges from previous models.

FICO® Score 10 does not use trended data like past models to give lenders the flexibility of using the model they prefer to use.

FICO® Score 10 T

FICO® Score 10 T, on the other hand, uses trended data (also known as time-series data). Trended data will give lenders a historical view of a person’s credit history from the previous 24 months.

This is the first time FICO® will use trended data in their scoring model. Previous models only gave lenders a small window into a person’s credit history, but trended data allows lenders to see behaviors and patterns based on a longer snapshot of a user’s credit history. For example, lenders can see if you tend to run up high balances on your credit card during the month, even if you’re never late on payments.

What Are the Main Changes?

The main changes with the FICO® Score 10 Suite are that FICO® Score 10 T uses trended data, personal loans are treated differently than before, and high balances, revolving debt and late payments are more heavily scrutinized.

Additionally, data for the entire suite is more comprehensive than before and algorithms have been updated to better predict risk for today’s consumer.

Trended Data

The use of trended data is the main source of the other major changes. Since lenders can take a historical look into a borrower’s behavior, they can make more informed decisions.

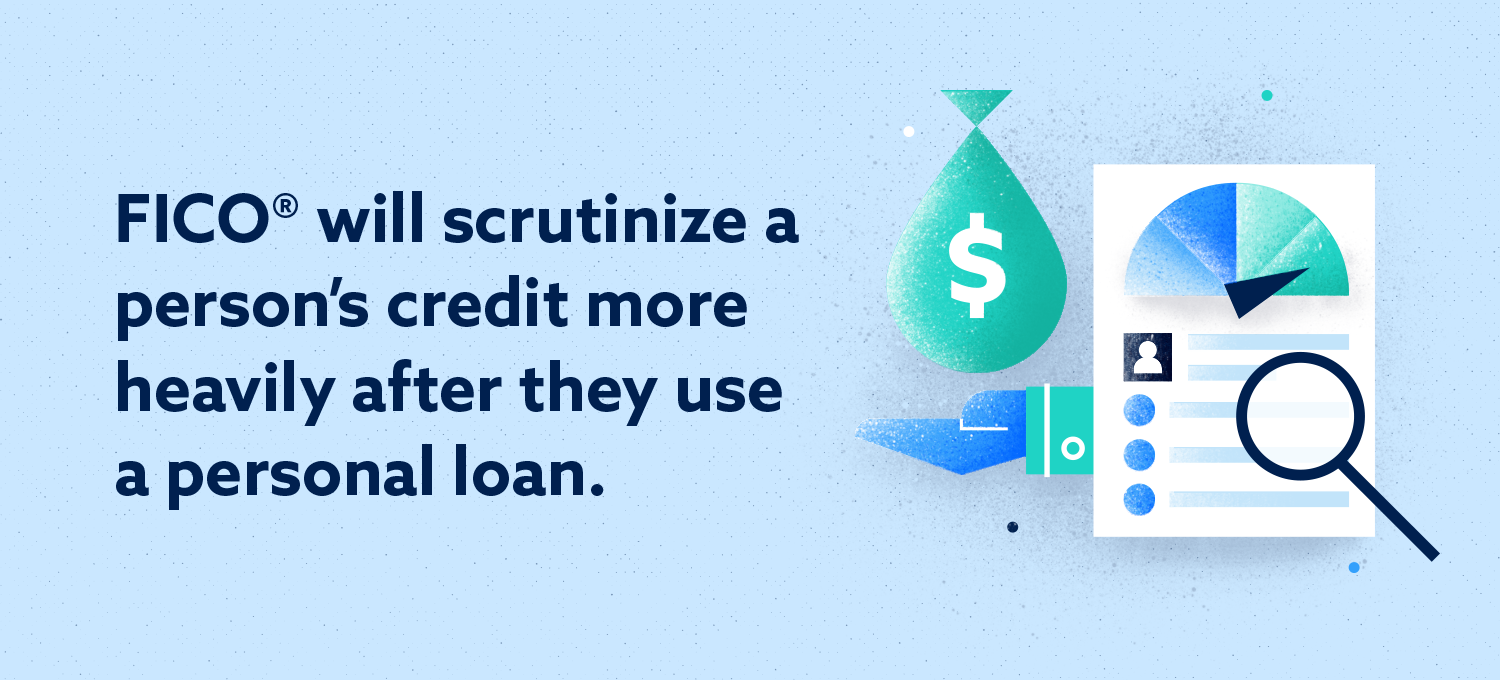

Personal Loans

Using personal loans can drop your score if FICO® determines you’re irresponsibly using it.

Vice President of Scores and Analytics at FICO®, Joanne Gaskin, said in an NPR interview that personal loans are now broken out into their own category to evaluate whether or not they are properly used.

In the old model, your score may have gone up if you paid off a large sum of debt with a personal loan. The new model will look at your behavior over a longer period of time to see if you continued to keep your balances low or if you increase your revolving debt after paying off the loan. For borrowers who do the latter, they can see a potential drop in their credit score.

High Balances, Revolving Debt and Late Payments

A high balance and revolving debt will more severely impact credit scores with this model compared to previous ones since FICO® Score 10 T can track your debt over time. Both high balances and revolving debt impact your credit utilization.

Late payments, also referred to as delinquency, will also more severely impact a person’s credit score. Payment history is the factor that most highly impacts your credit scores.

“Those consumers with recent delinquency or high utilization are likely going to see a downward shift, and depending on the severity and recency of the delinquency it could be significant,” FICO® Vice President of Product Management, Dave Shellenberger, said in a statement.

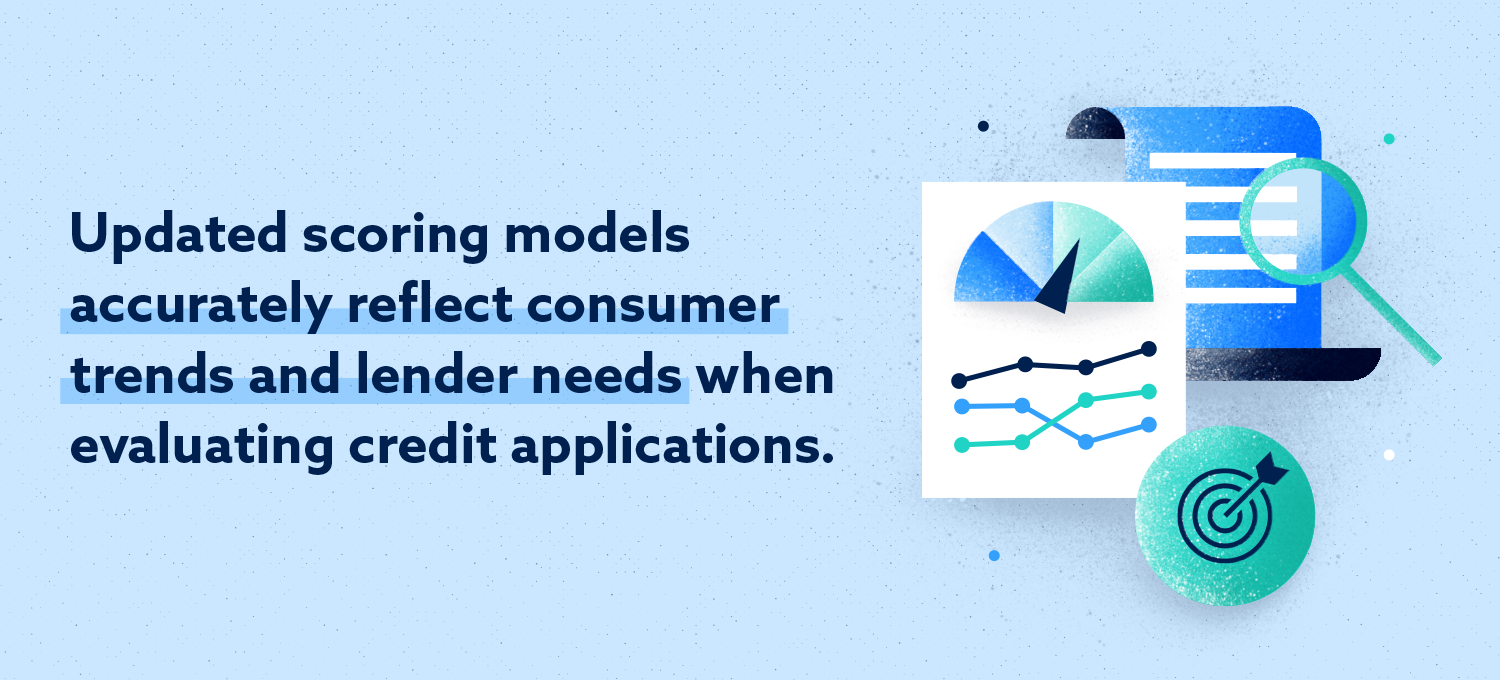

Why Does FICO® Update Their Scoring Model?

FICO® updates their scoring model to reflect consumer trends and lender needs. They update their scoring model about every four to five years, but this fluctuates depending on need and the types of changes needed.

These updates help lenders make more accurate decisions when evaluating credit applications. Changes can sometimes work in favor for consumers if they are more accurately scored as a result.

For example, FICO® predicts that the new FICO® Score 10 T will allow credit card lenders to approve up to 6 percent more applicants while keeping default rates steady, compared to FICO® Score 8.

When Will Lenders Adopt the FICO® Score 10 Suite?

FICO® will release the FICO® Score 10 Suite this summer, but it may take some time before lenders adopt the new model. FICO® says most lenders still use FICO® Score 8, which was introduced in 2009.

Although FICO® is used by most lenders, some use other scoring models like VantageScore. This is a newer scoring model created by the big three credit bureaus: Experian®, TransUnion® and Equifax®. Despite this, lenders may be tempted to use the newest FICO® score because of its stronger predictive model.

“When we release a stronger more predictive model we see that lenders will migrate to the stronger model because it allows them to make more loans to more consumers without taking more default risk,” Shellenberger said to MarketWatch.

How Could the Changes Affect Me?

Borrowers will see their credit score improve if they currently have a good credit score, but will see a decline if they’re in a lower FICO® score range, about 580 and below, Gaskin said in that same NPR interview.

About 110 million consumers will see a change of less than 20 points to their score under the new credit score model and roughly 80 million consumers will see a change in score of 20 or more points in either direction, upward or downward, FICO® said as reported by CNBC.

What Should I Do if I Think My Score Will Be Negatively Affected?

You can pay down and keep balances low, start an emergency fund, and avoid accumulating debt after using a personal loan if you think the new scoring model is going to hit your score. Take a look at below at how you can do these things to prepare.

- Pay down any high balances: Chip away at high balances since it has a more pronounced impact with the new scoring model.

- Pay balances more frequently to keep them low: Trended data can work against you if your balance is consistently high throughout the month. You can make smaller payments more frequently and decrease your spending to keep utilization low.

- Start and maintain an emergency fund: Instead of turning to credit cards or loans to cover an unexpected expense, an emergency fund is a great resource in a pinch that won’t impact your credit score. Start by putting aside what you can afford each month.

- Avoid building high balances after paying off debt with a personal loan: Since personal loans are given extra attention with this new model, be careful not to generate more debt after paying it off with a loan. Explore other options before taking out a personal loan and create a budget you can stick to in order to avoid taking on more debt.

How Can I Maintain a Good Credit Score During Scoring Model Changes?

Although it’s great to stay on top of scoring model changes, it’s best to continue engaging in good credit habits to maintain a good score. Keeping your balances down and paying bills on time are things you should always do since the factors that affect your credit score likely won’t change.

You can look into options like secured credit cards and credit builder loans if you have bad or nonexistent credit. These are options you can use to build or rebuild your credit if you have difficulty applying for unsecured credit cards or other types of loans.

Take a look at our tips for building credit if you want to take a deeper dive into improving your credit score and establishing good habits to keep your credit and finances in good shape.