Credit mix refers to the different types of credit accounts a person has open at any given time.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Credit mix refers to the different types of credit accounts a person has open at any given time. If your accounts are varied and include a diverse mix of loans and credit cards, they’ll positively affect your credit. However, it’s important not to take on more debt than you can handle as you work to increase your credit mix.

If you’re wondering “what is credit mix?” then this guide is for you. We’ll explain how this element impacts your credit and dispel several credit myths about credit mixes.

Key takeaways

- Auto loans, credit cards and student loans all contribute to credit mix.

- Credit mix accounts for 10 percent of your FICO® score and about 21 percent of your VantageScore®.

- Paying off a loan can decrease your credit mix.

What is a good credit mix?

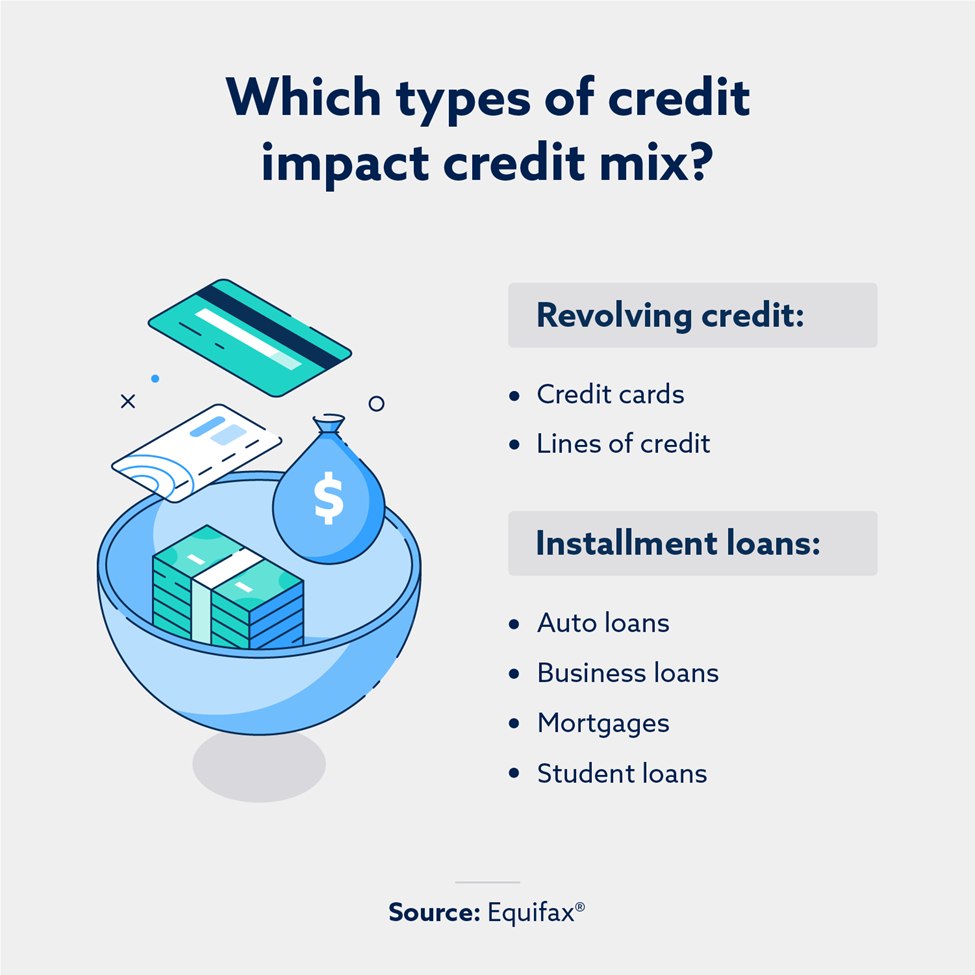

Credit accounts fall into two categories: installment loans and revolving debt. Installment loans refer to instances where you borrow a set amount of money and then repay your debt over time through installment payments.

Examples of installment loans include:

- Auto loans

- Business loans

- Mortgages

- Student loans

Revolving debt, on the other hand, refers to accounts that let you repeatedly borrow money up to a preset credit limit. Credit cards and home equity lines of credit are the most prominent examples of revolving debt.

A good credit mix will incorporate a combination of revolving debt and installment loans. Responsibly managing two to three credit cards, one auto loan and one mortgage will positively impact your credit.

Do different types of credit cards affect your credit mix?

Yes, which is one of the reasons why institutions like Equifax® recommend holding at least 2 different types of credit cards. For example, managing one credit card from a commercial bank and another from a retail store can steadily improve your credit.

How does credit mix affect your credit score?

Credit mix weighs on your credit score differently depending on which scoring model is considered. Most lenders use FICO score and VantageScore when approving people for loans—and both models have different credit score factors.

FICO score

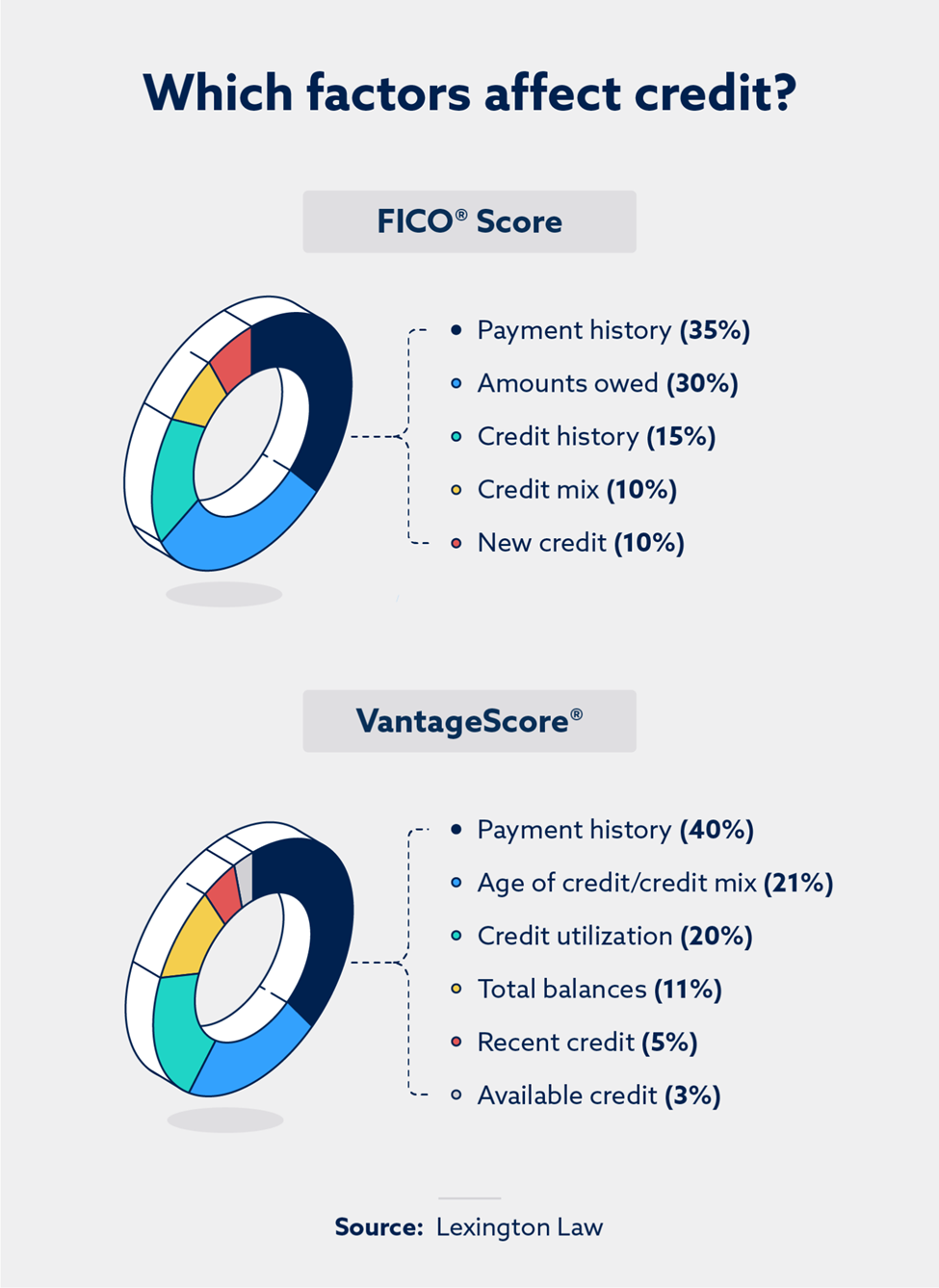

Created by the Fair Isaac Corporation (FICO), this model looks at the following five factors when calculating credit scores.

- Payment history (35 percent)

- Amounts owed (30 percent)

- Credit history (15 percent)

- New credit (10 percent)

- Credit mix (10 percent)

Credit mix will somewhat affect your FICO credit score, while payment history is the most significant factor.

VantageScore

VantageScore Solutions, LLC, created this model, which incorporates credit mix into the same category as credit age. Here’s how VantageScores are calculated:

- Payment history (40 percent)

- Age of credit and credit mix (21 percent)

- Credit utilization (20 percent)

- Total balances (11 percent)

- Recent credit (5 percent)

- Available credit (3 percent)

Credit mix can moderately affect your VantageScore, though payment history is still the most important factor.

How can you fix your credit mix?

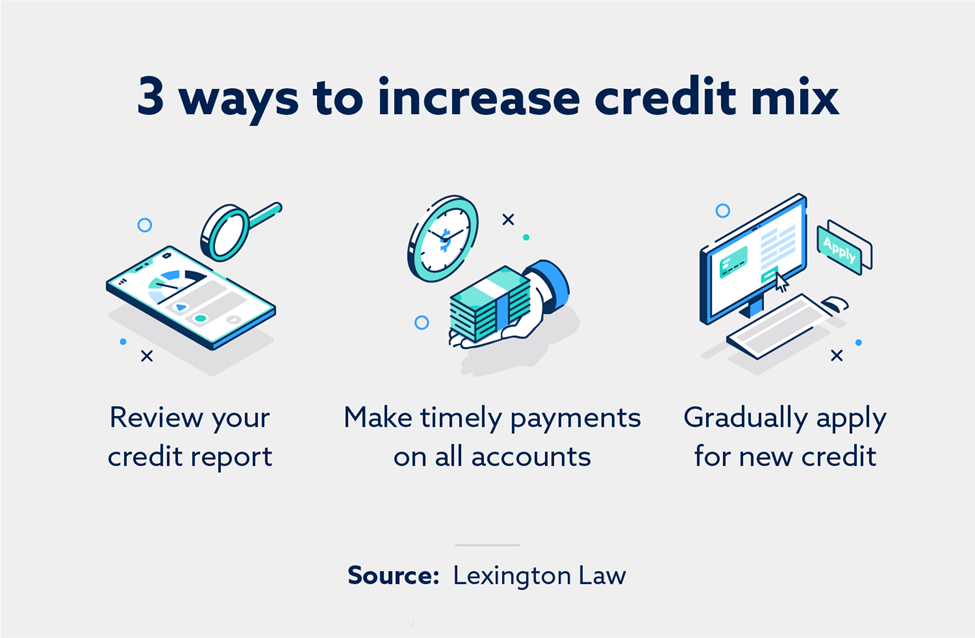

Opening a multitude of credit accounts might sound like a good idea, but this can significantly hurt your credit if these accounts are mismanaged. Instead, it’s better to gradually open new accounts that accommodate your financial situation—then commit to making timely payments on any account in your name.

Checking your credit report can help you understand your current credit mix and get a sense of what credit you might want to apply for next.

Learn more ways to improve your credit mix with Lexington Law Firm

Lexington Law Firm offers tiered services to help clients with their credit needs and answer their credit questions. Get started with a free credit assessment now.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.