Good credit etiquette, such as making timely payments and keeping low account balances, is the best way to rebuild your credit after a debt settlement.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

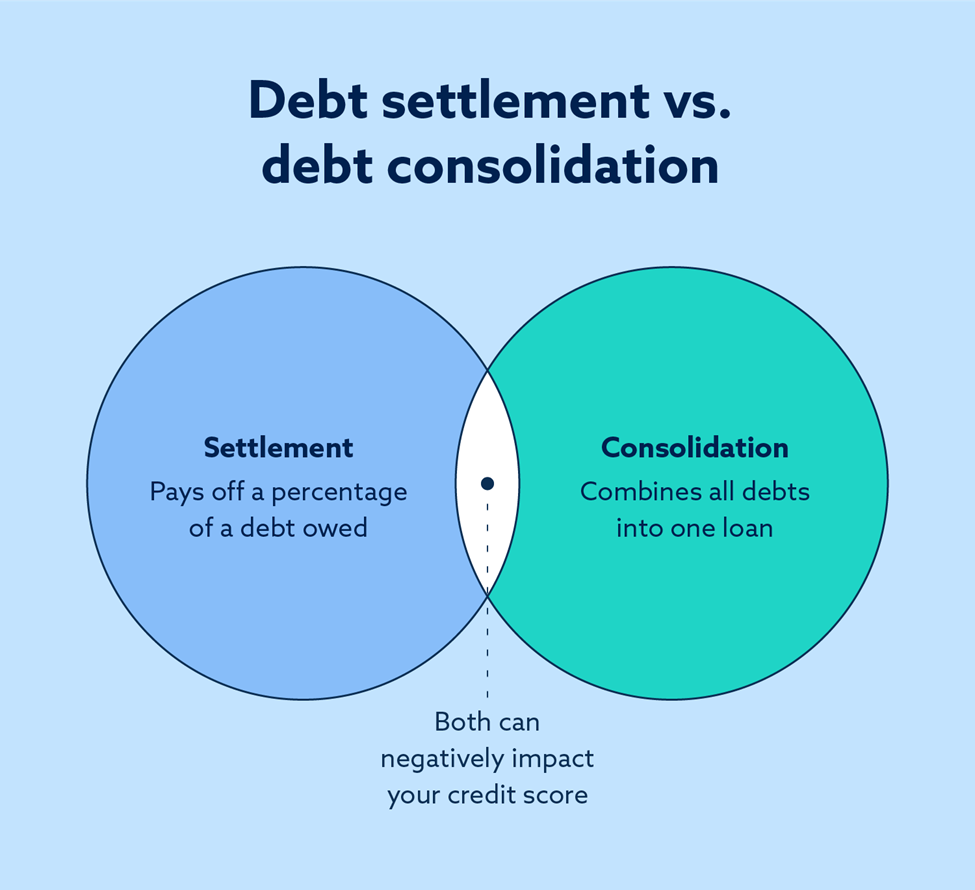

Debt settlement lets a person pay a lump sum to gain forgiveness on the remaining debt in an account. This procedure can help you get out of debt if the financial pressure becomes too extreme, but it can also negatively impact your credit in multiple ways. We’ll explore the impact of debt settlements and share strategies to help you rebuild your credit in the aftermath.

Key takeaways

- Payment history has the largest impact on your credit score.

- Debt settlement programs might ask you to stop making payments on an account.

- Credit repair services can help you quickly rebuild credit after a debt settlement.

Table of contents:

- Why does debt settlement negatively affect credit?

- 5 tips to rebuild credit right after a settlement

- Should you use your credit card during a debt settlement?

- Can a settlement be removed from credit reports?

- Work to rebuild your credit with Lexington Law Firm

Why does debt settlement negatively affect credit?

Debt settlement can hurt your credit by reflecting poorly on your loan handling habits. Payment history makes up 35 percent of your FICO® credit score, so settling a debt instead of completely repaying it can give a negative impression to creditors. Moreover, the debt settlement process may cause you to be late on payments or outright miss them.

A person’s credit profile is meant to represent their general spending habits and financial responsibility. While credit profiles aren’t perfect in this regard, they help lenders and credit card issuers decide who they will and won’t approve for funding.

5 tips to rebuild credit right after a settlement

Credit scores can fluctuate under the best circumstances. Even if a debt settlement case hurts your credit, rebuilding credit doesn’t have to take too long if you have a sound strategy.

1. Prioritize timely payments

The importance of payment history for your credit can’t be overstated. Regularly making payments on time after a debt settlement has been resolved displays your creditworthiness to lenders and credit bureaus. Just making the minimum payment requirements on your accounts will help you rebuild credit over time.

2. Maintain low account balances

Credit utilization compares your account balances against your total credit limit. For example, if you have a credit limit of $1,500 and your account balances come up to $500, your credit utilization ratio would be 33.33 percent.

Maintaining low account balances will also keep your utilization rate healthy. Financial professionals recommend staying below 30 percent utilization, and consistently staying below 10 percent could help you rebuild credit more quickly.

3. Limit your new credit applications

Limiting the number of times you apply for new loans or cards is another way to quickly fix your credit. Every time you apply for new credit, a hard inquiry is made into your credit history. Soft inquiries don’t lower your credit, while hard inquiries can reduce scores by several points. Receiving too many hard inquiries all at once can hurt your credit more substantially.

4. Try credit repair

Credit repair can help you rebuild credit through various methods, such as contacting credit bureaus and disputing errors on your behalf. First, check your credit report for potential errors, and then challenge these errors with a 609 dispute letter.

5. Review your credit reports

Reviewing your credit reports and identifying discrepancies can help you rebuild your credit if you address those errors. Studying your report can also give you another perspective on your financial habits and let you see if any unnecessary expenses are negatively impacting your credit history.

Should you use your credit card during a debt settlement?

Most debt settlement companies will ask you not to use your credit card during the process, as new account activity can complicate your settlement. As mentioned before, debt settlement companies may also ask you not to make payments on your account for a time.

Adding more debt to an account that you can’t pay down will raise your credit utilization rate and negatively affect your credit score in tandem.

Can a settlement be removed from credit reports?

In most cases, a debt settlement will stay on your credit report for seven years. If a settlement is still appearing on your report after that time limit, you can challenge this error by contacting the relevant credit bureau (such as TransUnion®, Equifax®, or Experian®).

Writing a goodwill letter might also clear a settlement from your credit report, though this method isn’t guaranteed. If you need help writing a goodwill letter, speaking with a financial advisor can set you on the right track.

Work to rebuild your credit with Lexington Law Firm

There’s a difference between learning how to rebuild credit and knowing the steps to take action. Explore Lexington Law Firm’s focus tracks to learn about alternatives to debt settlement and more strategies to rebuild credit over time.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.