The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Key takeaways:

- Variable APR will increase or decrease based on changes in the market.

- Lenders take your credit score into account when they issue an APR.

- If you pay off your card’s balance, APR won’t affect you.

An annual percentage rate (APR) is the price that you pay each year for borrowing money—like carrying a balance on a credit card. A card with a variable APR will charge more or less interest for carrying a balance depending on various factors.

APRs for credit cards are tied to the federal interest rate, so any changes to the latter will affect the former. It’s possible to manage a card with a variable rate once you understand its nuances. We’ll talk about the basics of how variable APR changes, factors that affect APR and how Lexington Law Firm can help you obtain various types of cards.

Table of contents:

- Variable APR basics

- Other factors that affect APR

- Fixed vs. variable APR

- How to calculate APR on a credit card

- How to get a lower APR on your credit card

- Prepare to apply for credit with Lexington Law Firm

How does variable APR work?

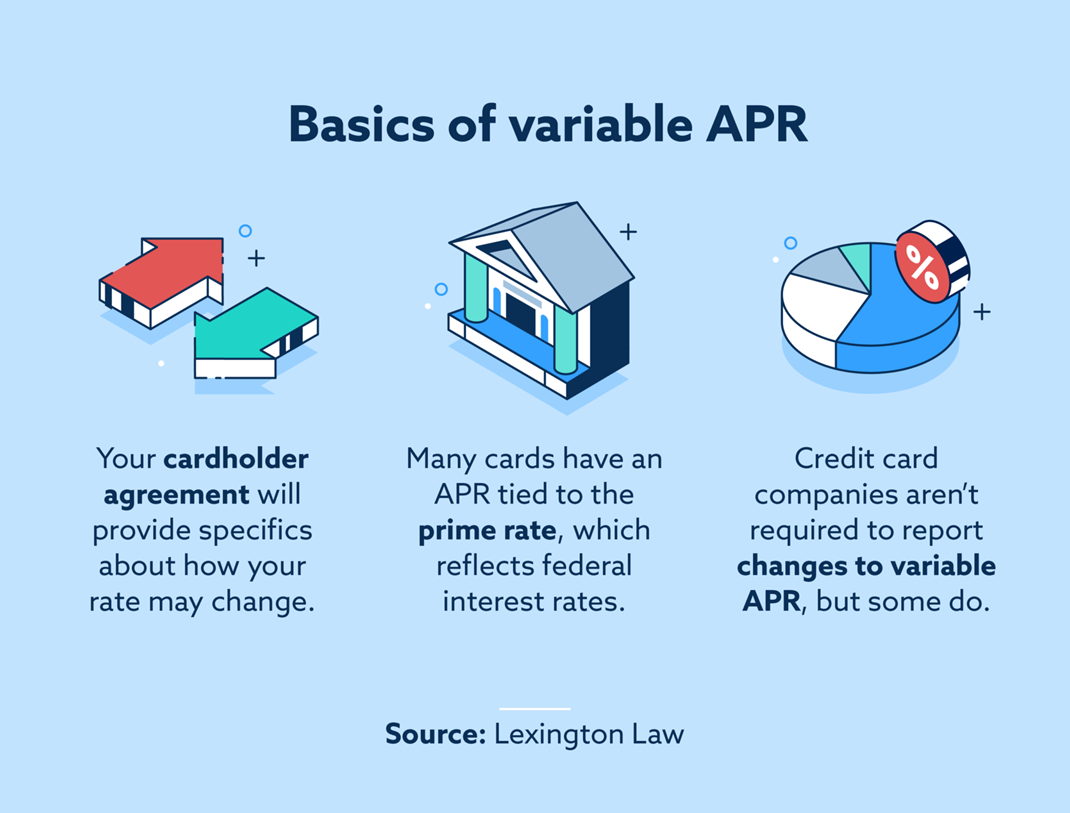

Variable APR increases or decreases based on current market conditions. Financial institutions use something called a “prime rate” to calculate your card’s interest rate.

Typically, the prime rate is about 3 percent higher than the federal loan rate—i.e., the rate set by the Federal Reserve when banks borrow money from each other. When federal interest rates go up, your credit card’s APR will likely rise as well—and vice versa.

On February 21, 2024, the Federal Reserve published its daily selected interest rates and set the prime rate for bank loans at 8.50 percent. If you aren’t sure what your current APR is, double-check your credit card statement or call your credit card provider.

Other factors that affect APR

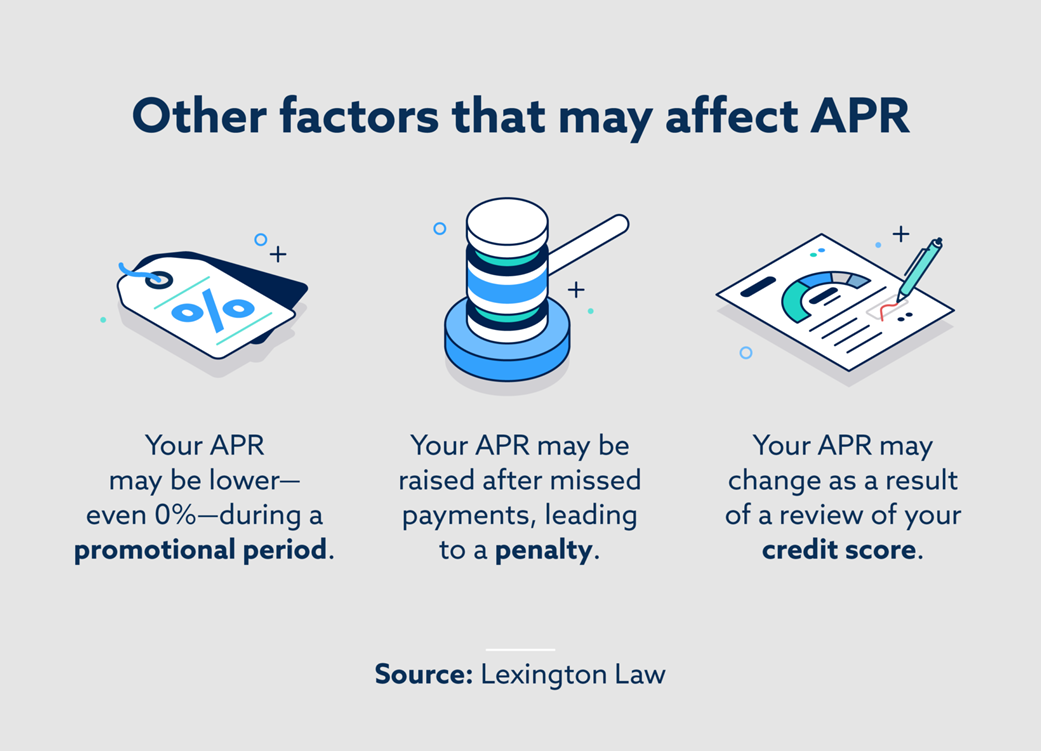

For anyone asking “Why is my variable APR so high?” know that the prime rate isn’t the other factor that influences APR. Some of the most common reasons that your APR may change include special programs, promotions, penalties and reviews.

- Special programs or promotions: Certain programs, like those that exist for service members, or promotions may lead to a lower APR. If those programs or promotions end, you may see a higher APR on your statement.

- Penalties: When you have one or more late payments over a certain period, your credit card company may establish a higher penalty APR that is detailed in your cardholder agreement.

- Reviews: As your credit score changes over time, your credit card company may review your credit file and raise or lower your rate accordingly.

APR can change for a variety of reasons, so it’s best to call your credit card provider if you aren’t sure what increased or decreased your rate.

Fixed vs. variable APR

A credit card with a fixed APR can only change from the rate outlined in your cardholder agreement if the card provider gives notice in advance. Fixed APR is consistent, but it can occasionally be higher than federal interest rates in certain instances.

Some advantages of fixed APR compared to variable APR are:

- Interest rates are consistent

- Budgeting is easier because your monthly payments won’t fluctuate too much

Some disadvantages include:

- Fixed APR can be higher than federal interest rates

- Cardholders might not be flexible with their rates

Fully paying off your balance each month will help you avoid interest whether your card has fixed or variable APR. That said, there are a few things to keep in mind if you’re trying to get a lower APR on your credit card.

How to calculate APR on a credit card

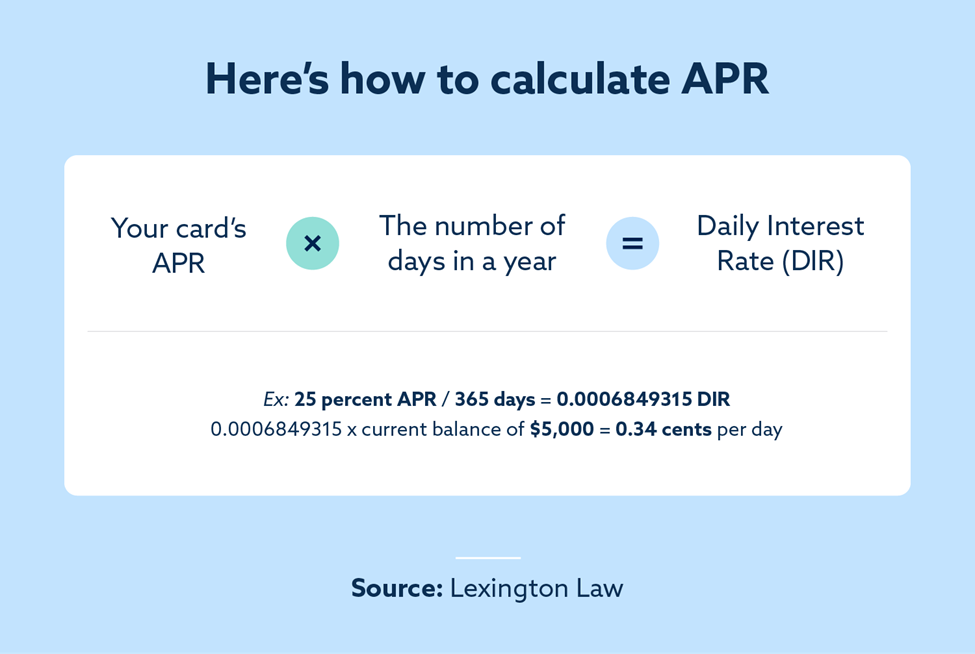

You can determine how much the APR on your card will affect your balance with the following formula:

- Divide your card’s APR (for example, 25 percent) by the number of days in a year (365). The resulting number (0.0006849315 in this case) is your daily interest rate.

- Next, multiply your daily rate by your current balance (e.g., $500). You should get 0.34 or 34 cents per day.

An annual rate between 20 and 25 percent is considered average for those asking “What is a good APR for a credit card?” However, your credit score significantly influences what sort of credit card and APR offers you’ll be eligible for. Banks might even preapprove a person with good credit score for a card with 0 percent APR for 12 months or more.

How to get a lower APR on your credit card

People who use credit responsibly are the lowest risk to lenders, so lenders are usually willing to offer better rates to them.

If you’re working toward a lower APR credit card, try out some of the following ideas to improve your credit:

- Pay your balance off each month: Paying your balance off each month has two benefits. It positively affects your credit score and you won’t have to worry about interest charges.

- Aim for low credit utilization: Using no more than 30 percent of your available credit shows lenders that you can budget your funds. Keeping your utilization below 10 percent can significantly boost your credit.

- Keep open accounts in good standing: If you have credit cards that are in good standing, you can keep them open even if you don’t use them often. Having older accounts increases your overall length of credit history, which is a factor in your score.

Prepare to apply for credit with Lexington Law Firm

You’ll want to review your credit report before you apply for new credit. Derogatory marks can affect your credit health, which may influence the APR of the credit cards you’re offered.

Consider using Lexington Law Firm’s credit repair services if you need help reviewing your credit report or addressing an error. Our services can help you contact credit bureaus and challenge errors on your report if need be.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.