Personal loan interest rates can range from 6 to 36 percent and are based on various factors. Your interest rate may depend on your credit score, the lender type and other factors based on your financial situation.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Recent data shows Americans have over $241 billion in personal loan debt. Whether you have personal loan debt or are considering taking out a personal loan, this may not always be bad debt. When used responsibly, personal loans can help you get better interest rates by consolidating other debts or help when you need additional funds. When taking out a loan, it’s helpful to know the average personal loan interest rates so you can get the best deal possible.

The interest rate is a fee based on the percentage of the loan amount, so ideally, you want the lowest interest rate possible. We’re going to discuss the average interest rates based on various factors, like your credit score and lender types, to help you find a loan that has the best rates.

Average personal loan interest rates by credit score

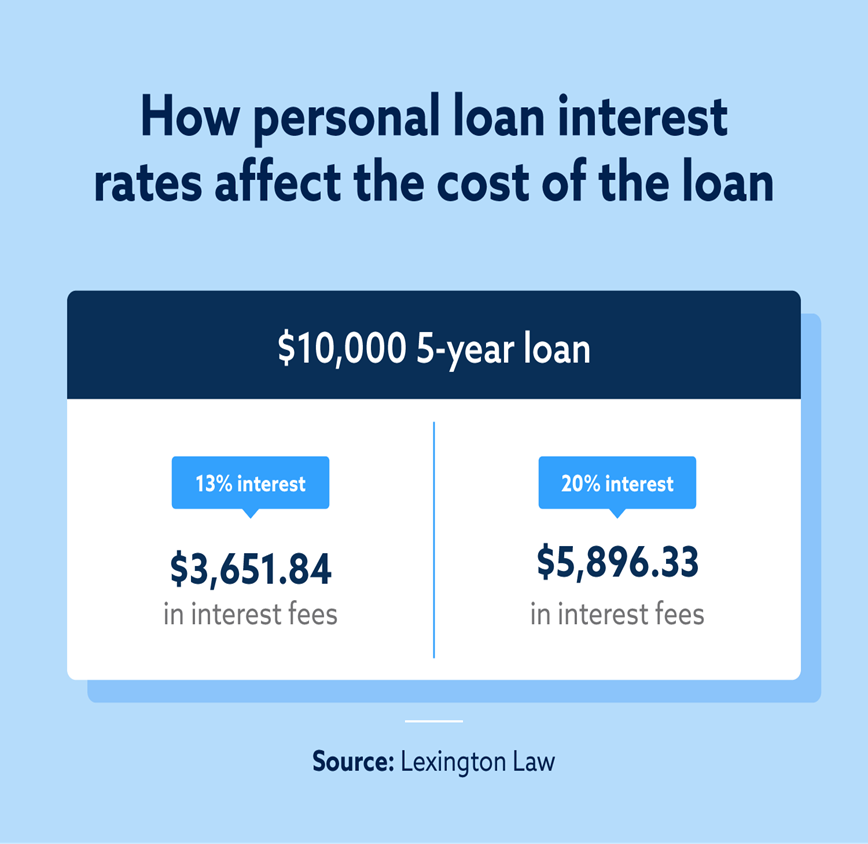

One of the best ways to get the lowest interest rates for personal loans is by having a high credit score. There are ways to get a loan with bad credit, but these loans often have some of the highest interest rates. High interest rates mean you may pay hundreds or thousands more in interest fees when you take out a loan. Below is a chart showing the difference between interest rates when taking out a loan based on your credit score:

| Credit score | Average loan interest rate |

|---|---|

| 300 – 629 | 28.50% – 32.00% |

| 630 – 689 | 17.80% – 19.90% |

| 690 – 719 | 13.50% – 15.50% |

| 720 – 850 | 10.73% – 12.50% |

Source: Bankrate

Average personal loan interest rates by lender type

You have a variety of options when taking out a personal loan. You can go into traditional brick-and-mortar financial institutions like banks or credit unions and find personal loans online. Some of these lenders may even offer bad credit loans, but remember, these typically come with higher interest rates.

In the following sections, we show interest rates from some of the most popular lenders from each category. As you’ll see, each lender has a range of interest rates, which depends on your credit score, income and other financial information.

Average personal loan rates by bank

Personal loan interest rates from banks can range from 6.99 percent to 24.99 percent. Currently, Santander Bank offers the lowest interest rate range.

| Bank | Interest rate range |

|---|---|

| Citi | 10.49% – 19.49% fixed rate APR |

| Santander Bank | 7.99% – 24.99% |

| Wells Fargo | 7.49% – 23.24% fixed rate APR |

| U.S. Bank | 8.74% – 24.99% fixed rate APR |

Average personal loan rates by credit union

Credit unions are another way to get personal loans, and they’re similar to banks except they’re member cooperatives and not-for-profit. Each of the credit unions listed below has lower interest rates on the higher end of the range, with none being over 20 percent.

| Credit union | Interest rate range |

|---|---|

| PenFed | 7.99% – 17.99% |

| Members 1st Federal Credit Union | Starting at 12.39% |

| Navy Federal Credit Union | 8.99% – 18.00% |

| USAA | 10.14% – 18.51% |

Average personal loan rates by online lender

Many people turn to online lenders because not only are they convenient, but they’re also more likely to lend to those with bad credit or those who need a personal loan after a bankruptcy. Depending on your credit score and credit history, some of these personal loans have the highest interest rates.

| Online lender | Interest rate range |

|---|---|

| Achieve | 7.99% – 35.99% |

| Avant | 9.95% – 35.99% |

| LendingClub | 9.57% – 35.99% |

| LendingPoint | 7.99% – 35.99% |

| Prosper | 8.99% – 35.99% |

| SoFi | 8.99% – 29.49% with Autopay |

| Upgrade | 8.49% – 35.99% with Autopay |

| Upstart | 7.80% – 35.99% |

5 factors that affect your personal loan interest rate

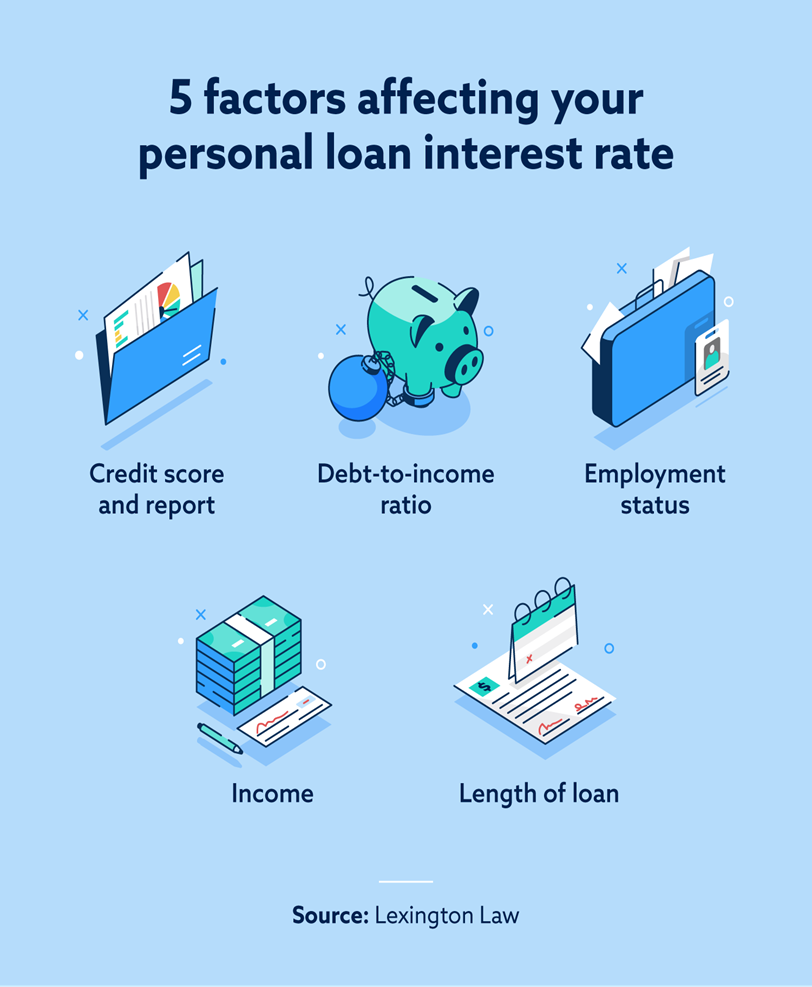

If you’re in the market for a personal loan, it’s helpful to know what lenders are looking for. This helps you get approved for the loan and the best interest rate possible. If you have poor credit, using a cosigner may help with approval, but if you want to get a personal loan without a cosigner, here’s what lenders are looking at:

- Credit score and report: Your credit score and report show your credit history and how likely you are to pay back your loan. A low credit score can lead to higher interest rates.

- Income: Lenders use your income to determine the loan amount and whether you can pay the amount back.

- Debt-to-income ratio: Your debt-to-income ratio is a calculation of how much debt you currently have compared to your income. Ideally, it should be low.

- Employment status: Employment shows a steady flow of income. If you’re self-employed or an independent contractor, it may make getting a loandifficult.

- Length of loan: Shorter loan terms often come with higher interest rates.

What is a good personal loan interest rate?

What’s considered a “good” personal loan interest rate will depend on the person and their situation. Typically, a good interest rate is anything below the average rate for your credit score. Ideally, you want to improve your credit to get even better interest rates on personal loans.

How your credit score affects your personal loan interest rate

Your credit score and credit history play a big part in getting a good personal loan interest rate. As mentioned earlier, a high interest rate can cost you thousands in additional interest fees. If you have a bad credit score, you may have errors on your credit report that are hurting your credit. Lexington Law Firm offers an in-depth credit assessment that shows you where your credit stands before you apply for a loan. Get your free credit assessment today.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.