The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

If you have a car loan, making your payments on time and in full each month should help build your credit over time.

Having good credit can save you a significant amount of money in interest fees on a car loan. Ideally, you’ll want a credit score of 660 or higher to get a favorable interest rate, but did you know that having a car loan may also help improve your credit?

We’re going to explain how car loans can affect your credit report and how they may be able to help raise your credit. You’ll also learn how to find the best car loans to help you save money on your new vehicle.

Is a car loan good for your credit?

Applying for a car loan can hurt your credit temporarily, but your credit can recover and even improve in time. When you apply for a car loan, the lender needs to run a hard inquiry to check your credit history, which is what can lower your score. The decrease can also happen if you refinance your car, but in both cases, the impact is usually minimal.

The good news is that a car loan can help you boost your credit in the long term. One of the primary factors that determines your credit score is your payment history. If you take out a car loan and make your monthly payments on time, these payments are reported to the major credit bureaus. If you’re wondering how fast a car loan will raise your credit, the answer is that it can take a few months to start seeing results.

One way to ensure you make your monthly payments on time is to set up automatic payments. After months of making these on-time payments, the consistent positive payments should far outweigh the temporary decrease from the hard inquiry.

How auto loans affect your credit report

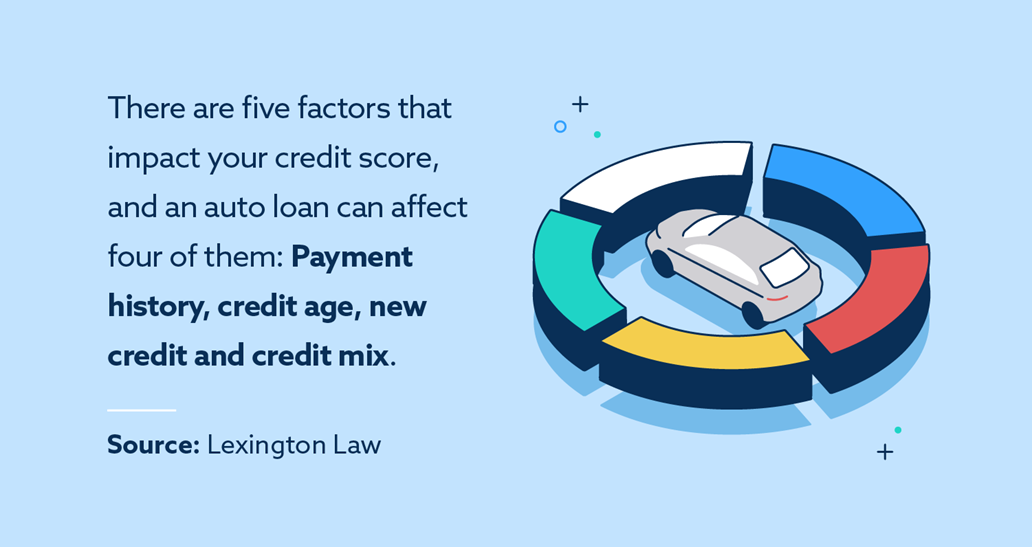

Your credit report has a lot of data, and it can seem a bit overwhelming. Before going over how auto loans affect your credit report, it’s helpful to know the five factors affecting your credit score.

Each factor is weighted differently, so they’ll have a different level of impact on your credit. The following percentages are based on the FICO® scoring model, which is the most commonly used model.

Payment history (35 percent)

Your payment history is the most heavily weighted factor of your credit score at 35 percent. Late and missed payments can result in derogatory marks, which have a negative impact on your credit. On the other hand, when you make your car payments on time, the credit bureaus report them, which can help your credit.

Credit utilization (30 percent)

Credit utilization is how much you owe compared to your overall credit limit. Your utilization is often in the form of a percentage or a ratio. Ideally, you want to keep your credit utilization under 30 percent. For example, if you have a $1,000 credit limit and only owe $200, that’s a 20 percent utilization rate. Your car loan won’t affect your credit utilization.

Credit age (15 percent)

Your credit report also shows the length of your credit history, and this helps lenders see how much experience you have with credit. When you acquire an auto loan, you’re typically paying off the vehicle for years, and this is factored into the average age of all of your credit accounts. By having a long history of making your payments on time, it can help your credit.

New credit (10 percent)

Earlier, we mentioned that the application process can temporarily lower your credit due to hard inquiries. If someone is regularly applying for new lines of credit, it may be a red flag to lenders. But remember, financing a car can also help you build your credit over time, eventually outweighing the negative impact of the hard credit check.

Credit mix (10 percent)

The two primary types of credit are installment credit and revolving credit. Credit cards are considered revolving credit because when you make your payments, you can access that money again. With a line of installment credit, you owe a set amount each pay cycle, and car loans fall into this category. When you have a variety of types of credit, it helps improve your credit mix.

On your credit report, you will find two categories that will provide information about your car loan:

- Types of accounts: In this category, you will find your credit mix, and under the installment accounts category, you will find your car loan as well as other installment loans. Other examples of installment loans include mortgage loans and student loans.

- Current status: You will also see the status of your auto loan. If you make your payments on time, it may say that the account is “current,” or it will say “paid as agreed.” Basically, this showcases your payment history on a specific account. If you’re 30 days late on your payments, this can hurt your credit, and the lender may even repossess your vehicle.

It’s also possible that a reporting error inaccurately shows a missed or late payment, and this can unfairly lower your score. Should this happen, you can file a dispute to address it.

How to find the best car loan

It’s common for people to shop around for the best deal on a car, but it can also be helpful to shop around for the best car loan. When taking out a loan, one of the primary considerations should be the interest rate. The overall interest rate of the car can vastly change the price.

For example, let’s say you put $1,000 down on a $20,000 vehicle with a loan term of five years and a 5 percent interest rate. The total interest on the vehicle would be $2,513, making the vehicle cost $21,513.

Using that same example, you would pay far more at an 8 percent interest rate. At an 8 percent interest rate, the total interest would be $4,115, which is around $1,500 more than the 5 percent interest rate.

You may be able to find better interest rates by going through your current bank or other lenders. Good credit is another key factor in finding a good interest rate.

Repair your credit before shopping for a car

Your credit can have a major impact on how much interest you pay for your vehicle. According to recent data, the average car loan interest rate for a new car for people with a credit score of 781 or higher is 5.07 percent. If your credit score is under 661, the average interest rate for a new car is 8.99 percent.

If you need help with your credit prior to getting a car, reach out to Lexington Law Firm. There may be errors on your credit report hurting your credit, and we have a team who will work to address these errors on your behalf. Sign up today to get a free credit assessment.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.