Retirement is an area that is full of confusion and uncertainty for most Americans. With conflicting online options regarding best practices, it is easy to get lost in how to correctly plan for retirement.

But does the average American know this information? We decided to find out. Our poll of over 3,000 found the following:

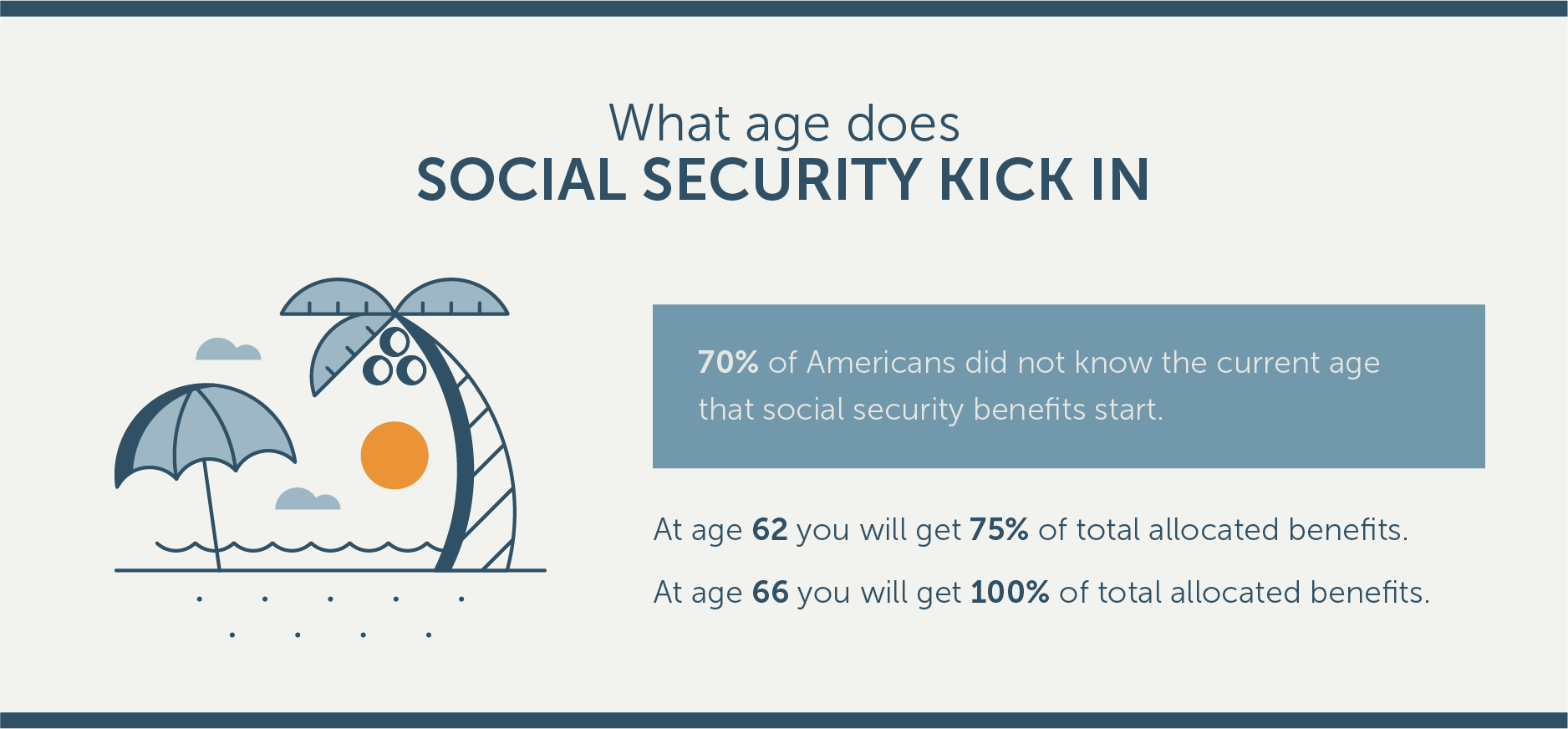

- 70 percent do not know the age at which social security benefits starts.

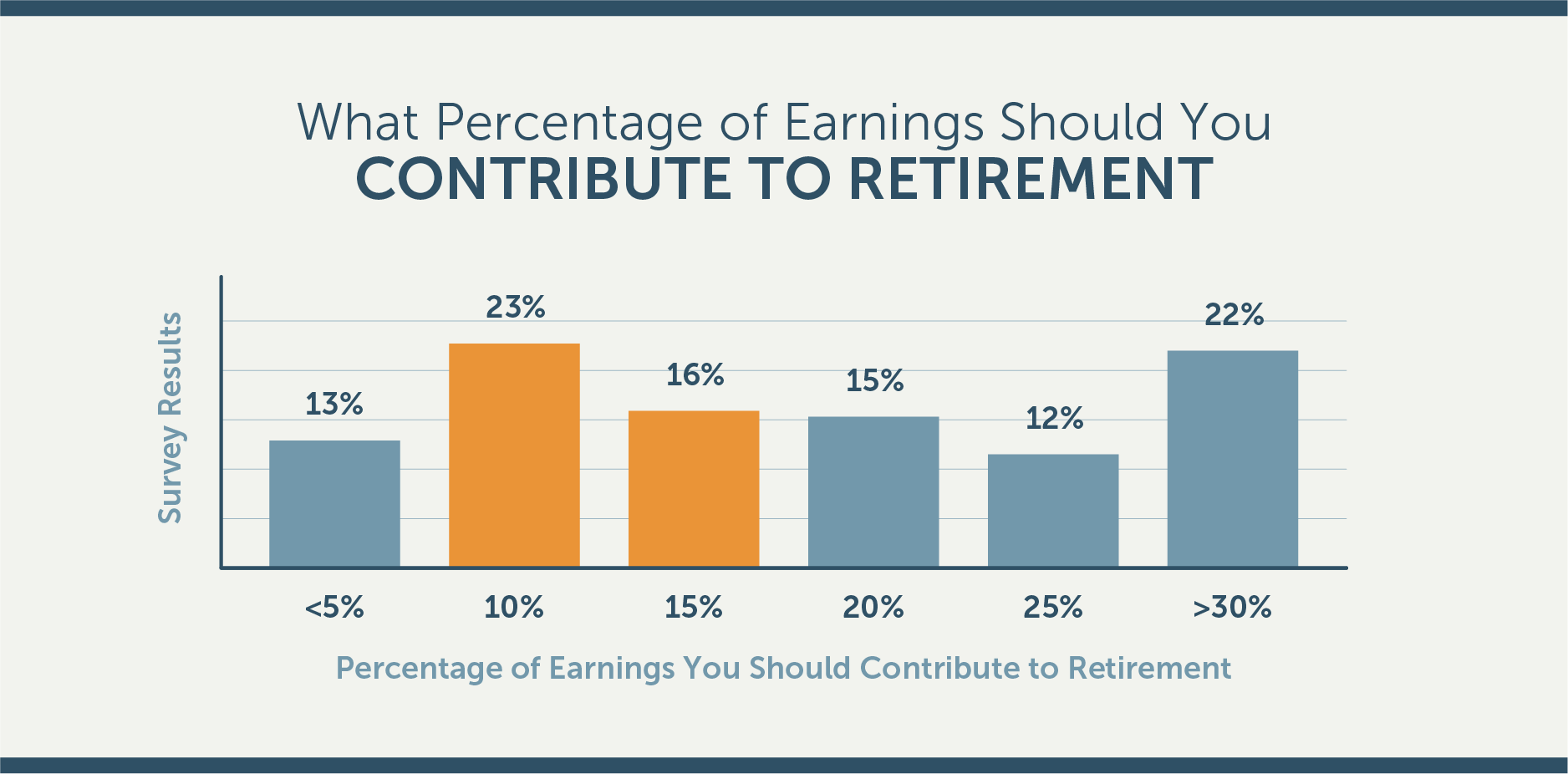

- Less than half know how much of their earnings they should contribute to retirement savings.

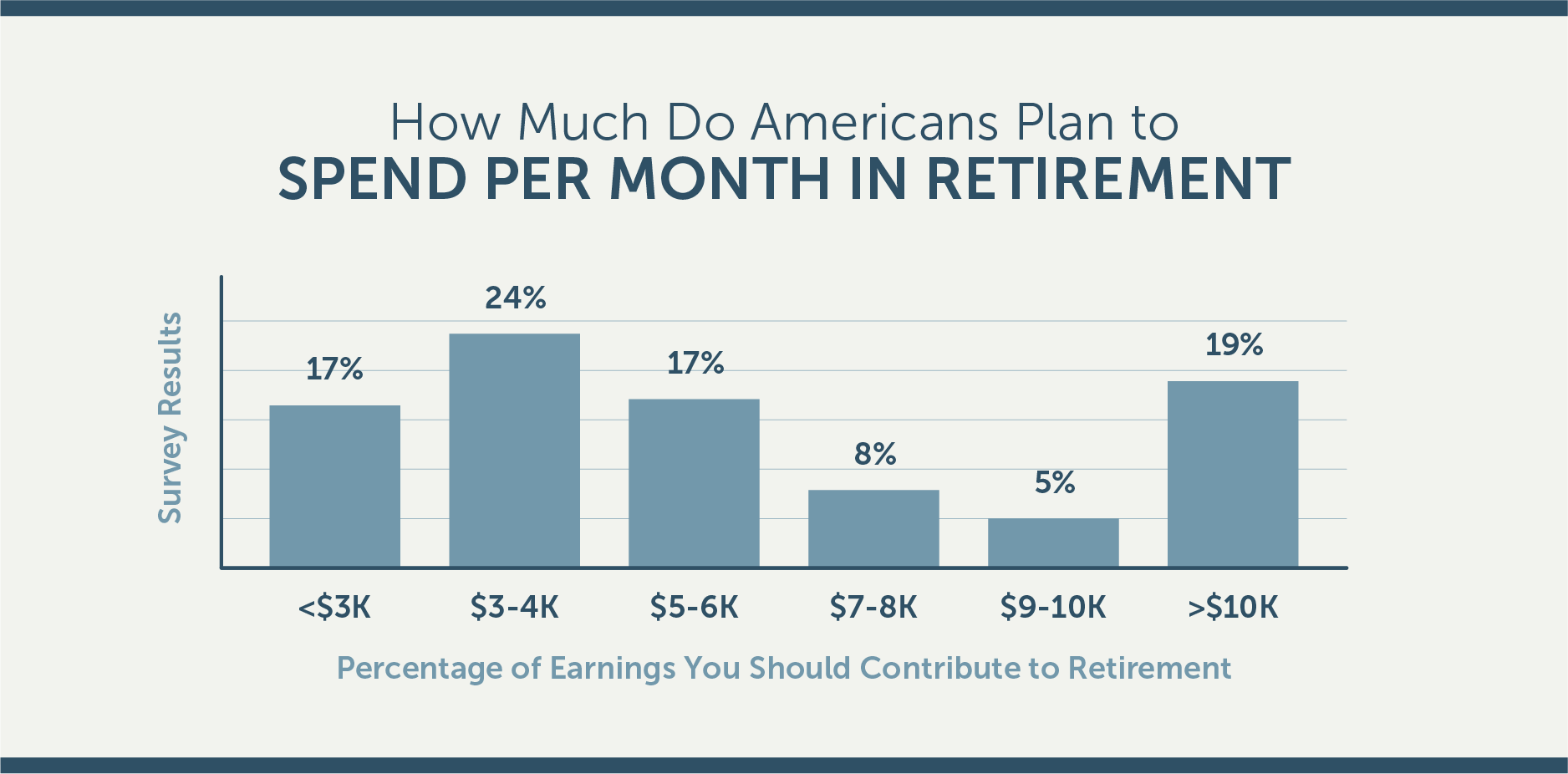

- 83 percent expect to spend more than $3,000 per month in retirement.

In its current form, social security operates on a sliding scale of monthly benefits depending on which age you begin retirement. The Social Security department lists full retirement ages depending on the year of which you were born. For Americans born after 1960, the full retirement age is listed as 67. But, the The youngest you can start earning social security benefits is actually at the age of 62. This is the age where you earn 75 percent of the total allocated benefits.

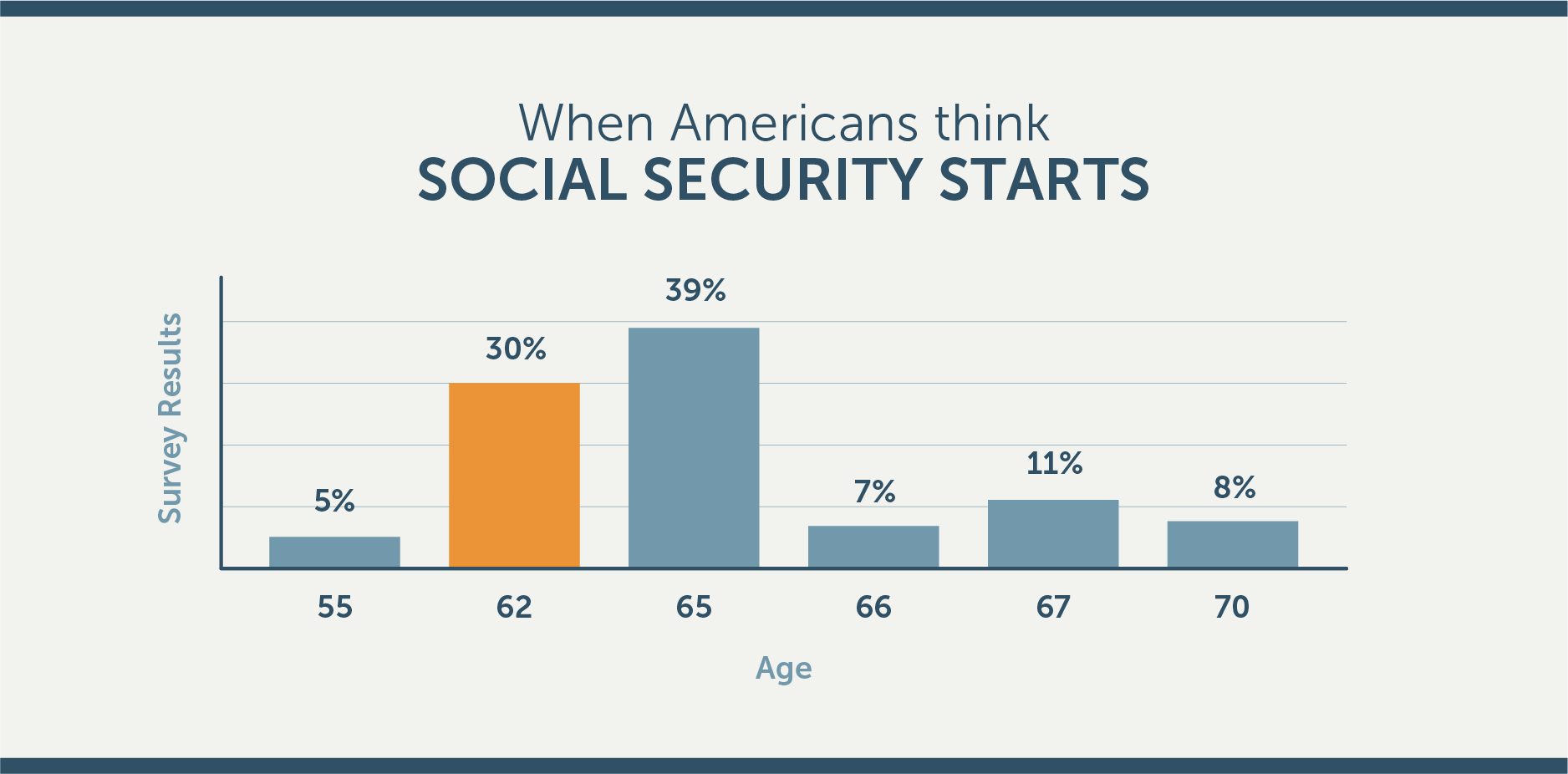

Only 30 percent of Americans surveyed know the correct age that Social Security benefits begin. For some, there may be a mentality that social security starts when it offers its full amount of benefits. The confusion may come from the fact that after you turn 62, the percentage of total benefits increases eachmonth until the age of 67 where it pays out at 100 percent. Additionally, the Center for Retirement Research reports that 27 percent of women and 34 percent of men wait to begin claiming social security benefits from the age of 65–66, which may also be why people misunderstand the age it begins.

Why is everyone confused about social security?

Most Americans may also believe that social security starts at the age of 65 because it is also the first year you can withdraw from a 401k or an individual retirement account penalty free. As many people associate the retirement programs with social security it is not without reason to understand that 65 was the most popular choice.

The third most popular social security age answer by Americans, collecting 11 percent of total responses, was the age of 67. Social security benefits reach 100% of the total allotted amount at the age of 67.

How much do Americans think they need to contribute to retirement?

America is split when it comes to the ideal percentage of earnings contributed to retirement. The percent of your earnings you should save dependents on a wide range of factors including how early you begin to save, how much money you earn when you plan on retiring and what quality of life you expect when you retire.

When asked what percent of earnings people should save for retirement, less than half knew you should save between 10 and 15 percent. Most financial advisors suggest that you should save 10 to 15 percent of your yearly earnings to a retirement program starting in your early 20s. However, if you do not start contributing to savings early in life you should be contributing even more. Vanguard reported the average deferral rate among users of their platform was 6.2 percent in 2016, and 44 percent of all accounts only contributed 3 percent of their salary.

When it comes to how much you should contribute to retirement, Americans are split among contributing 10 percent and contributing more than 30 percent. For younger Americans, planning for retirement does not seem to be their top priority. In fact, 35 percent of 18–24 year olds think you should only be saving less than 5% of your earnings for retirement.

For someone who makes around $50,000 each year until they retire, 5% savings would only leave them with a little over $100,000 at the age of 62.

32 percent of Americans aged 25 to 34 years olds answered that you should be contributing over 30 percent of earnings to retirement. This may be a sign that many feel overwhelmed when they first start to save. For Americans contributing to retirement savings later in life, it can come as a shock of how much you actually need to retire. With other priorities such as student loan debt and credit card debt upon entering into the workforce, it can be hard to decide between contributing to retirement and paying down debt.

The general rule for retirement is that you should have saved 8 to 10 times your salary by age 67. This savings approach will leave a large enough of a nest for general retirement spendings to live a quality life and to bridge the gap between social security and actual retirement costs.

When we compare what Americans are planning on spending in a month during retirement by region we can see some general trends. For the most part Americans agree on how much they are planning to save, with the majority of Americans planning on spending under $4,000 a month.

If someone making $50,000 per year was only saving 5%, they’d have about $48,000 per year if they spent $4,000 every month. This would leave them without any funds after two years.

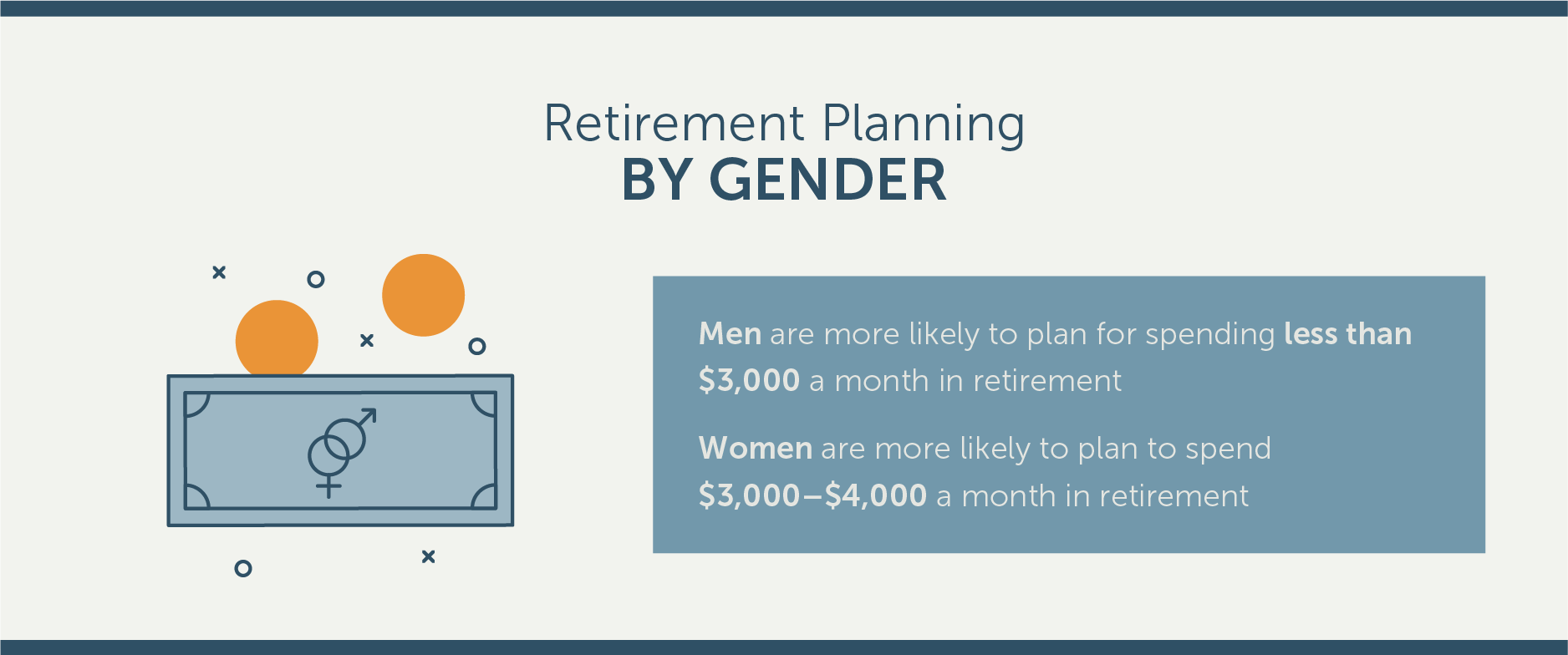

Our study found that on average men tended to plan on spending less money in retirement than women. The difference in costs among men and women can be extreme with products marketed towards women costing 48 percent above the male equivalent, which can point to the reason women plan to spend extra cash.

For most Americans, the path to a healthy retirement lies between cutting down on debt and contributing the most amount of money early in life to retirement. Although retirement for many Americans is still a distance away, it is important to start planning early. As retirement is still a difficult area for many Americans to plan there is a growing need for many to practice better financial planning and overall retirement literacy.