Lexington Law offers a free credit repair consultation, which includes a complete review of your FREE credit report summary and score. Call us today to take advantage of our no-obligation offer.

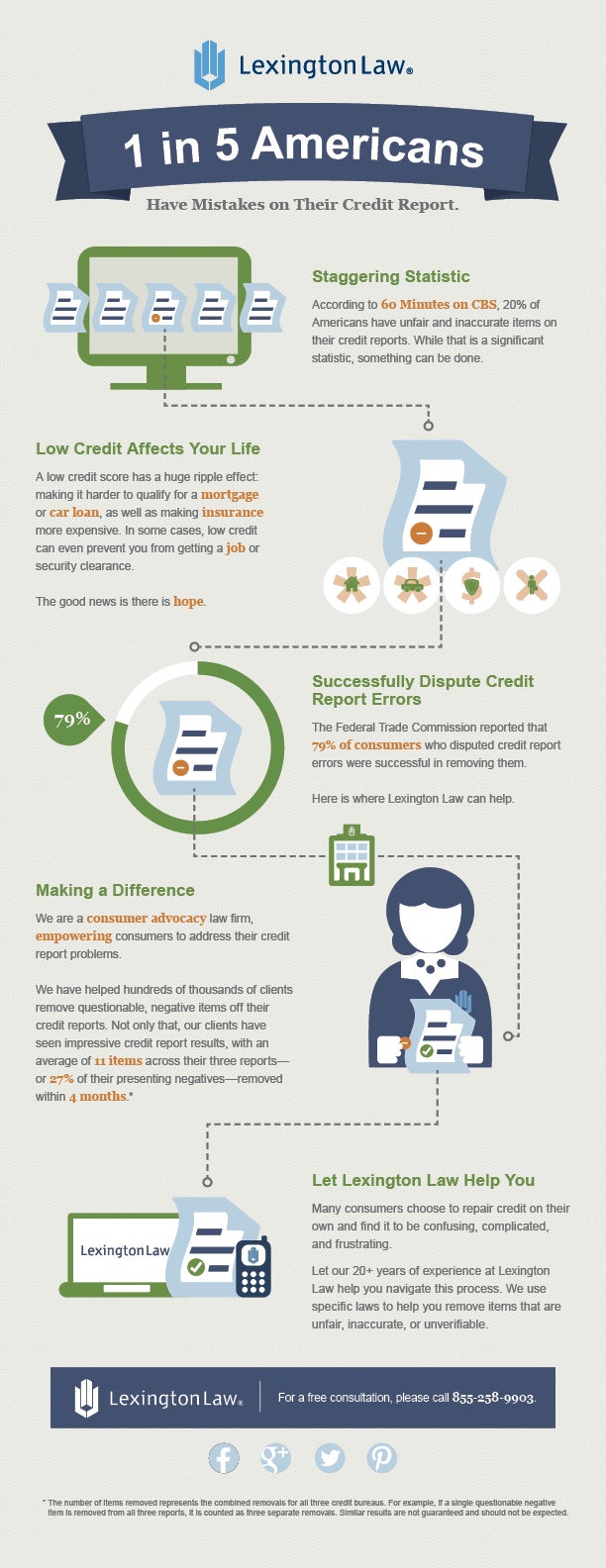

1 in 5 Americans have mistakes on their credit report according to CBS 60 Minutes. Those mistakes can often lead to poor credit scores, disqualification for mortgages […]