The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

A credit freeze is a free way to restrict access to your report, and federal law requires credit bureaus to offer it. A credit lock is a premium offering from credit bureaus, and the main advantage is that you can lock and unlock your report instantly.

In 2022, public data breaches exposed over 20 billion records, allowing bad actors to access sensitive financial information. While credit freezes and credit locks both help you protect your credit report, there are important differences. A credit lock is a premium offering from credit bureaus that you can lock and unlock your report instantly. A credit freeze is free but less convenient, and federal law requires credit bureaus to offer it.

Credit freezes and credit locks are useful ways of deciding who can access your credit report. Understanding the differences between these two methods of credit report protection can help you decide which is the best fit for your situation.

The three main credit bureaus—TransUnion®, Experian® and Equifax®—offer both credit freezes and credit locks to everyone with a credit report.

Read on to learn more about the differences between a credit lock vs. freeze and how each of these works.

Table of contents:

- What is a credit freeze?

- How to freeze your credit

- How to unfreeze your credit

- Is there a downside to freezing your credit?

- What is a credit lock?

- How to lock your credit

- Should you use a credit freeze or a credit lock?

What is a credit freeze?

A credit freeze is a free, secure way to restrict access to your credit report. Placing a freeze on your credit prevents anyone from opening up a new credit account using your information without your permission.

Because a credit freeze blocks new credit under your name, it’s a strong protection against fraud, especially for victims of identity theft.

The option to freeze your credit is a protected right under federal law, so TransUnion®, Experian® and Equifax® must provide this service to you at no cost. Additionally, they have to place the freeze within one business day.

Learn more about how to freeze and unfreeze your credit below.

How to freeze your credit

You can freeze your credit over the phone, online or by mail. However, you’ll need to request a credit freeze at each credit bureau, which means contacting TransUnion, Experian and Equifax separately. After verifying your identity and freezing your credit, you’ll receive a secure Personal Identification Number (PIN) that you’ll need when you’re ready to unfreeze it. You can still check your credit score when your account is frozen, and your existing creditors can also review your file.

In general, a credit freeze lasts until you choose to unfreeze it, but this varies in several states, so be sure to check applicable laws in your area.

Take action: Read our detailed guide about how to freeze your credit with each of the three credit bureaus, with simple steps for making requests over the phone, online or by mail.

How to unfreeze your credit

You can unfreeze your credit by making a request with the credit bureaus and providing your secure PIN. This step also requires proof of your identity, which you can provide over the phone, online or by mail.

You can permanently unfreeze your credit, unfreeze your credit for a specific amount of time or unfreeze your credit only for a specific creditor.

Federal law requires credit bureaus to process your request within one hour if you ask them to unfreeze your credit online or over the phone. On the other hand, requests via mail may take up to three days after receipt before they are processed.

Take action: Read our detailed guide to learn how to unfreeze your credit with each of the three credit bureaus, including information about requests over the phone, online or by mail.

Is there a downside to freezing your credit?

Freezing your credit is a straightforward way to lower the risk of bad actors opening any new credit accounts with your information. That said, when you want to open a new account yourself, you’ll need to go through the process of unfreezing your account before you can do so. Though credit freezes are impactful in preventing identity theft, the planning they require can be inconvenient.

If you’re looking for a more immediate way to restrict and allow access to your credit, a credit lock may be a better option.

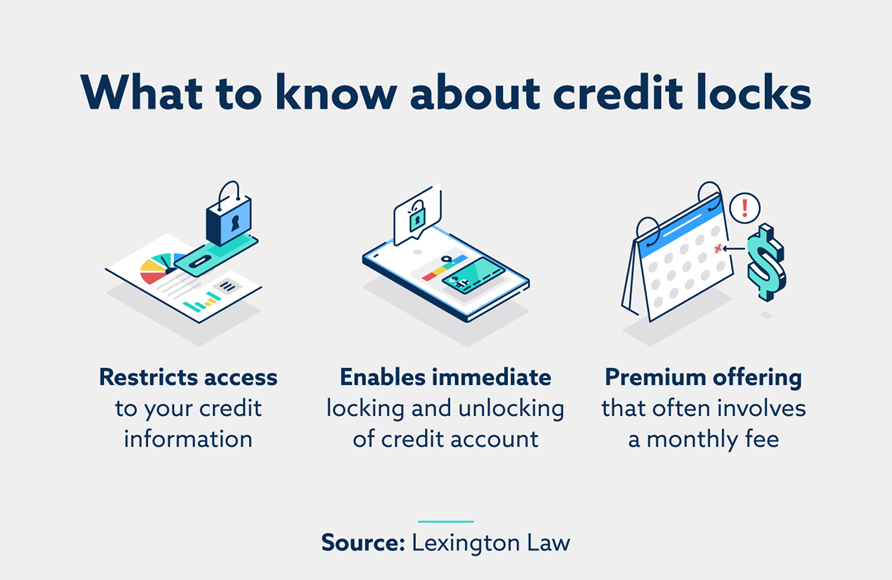

What is a credit lock?

A credit lock is a premium offering from the credit bureaus that provides a more immediate method for allowing and restricting access to your credit information.

Like with credit freezes, you must request separate credit locks from each credit bureau. But credit locks aren’t protected by federal law and often entail a monthly fee, so you should read the agreement with each credit bureau carefully.

A credit lock enables you to lock and unlock your credit immediately using a website or app. This means that you can keep your account locked most of the time, but when you need to unlock it—for instance, when getting a credit card or taking out a personal loan—you don’t have to wait.

How to lock your credit

You can lock your credit by signing up for a premium credit monitoring service. This can also be done with all three credit bureaus: TransUnion, Experian and Equifax.

Take action: Learn more about these products’ costs and specific features by visiting each bureau’s website. Equifax offers its Lock & Alert service, Experian provides CreditLock and TransUnion bundles a credit lock option with its Credit Monitoring service.

Should you use a credit freeze or a credit lock?

Deciding between a credit freeze vs. lock depends on your particular circumstances and needs.

A credit freeze has the advantage of being free and backed by federal law. On the other hand, unfreezing credit takes some time, which can be inconvenient. A credit lock enables you to instantly lock and unlock your credit accounts, but it typically involves a monthly fee and may offer fewer legal protections.

No matter what you choose, both credit freezes and credit locks are valuable tools for protecting your identity. If you have been the victim of identity theft, you may have inaccurate items on your credit report. Get your free credit assessment at Lexington Law Firm to ensure your report is accurate and your identity is safe.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.