A purchase annual percentage rate (APR) determines the amount of interest credit card issuers add to an outstanding credit card balance each month. The average credit card APR is 22 percent.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Key takeaways:

- The average credit card APR is 22.16 percent as of May 2023, a 33 percent increase from the previous year.

- You can negotiate a lower purchase APR with your credit card issuer.

- APR can change over time due to a promotional period ending, penalties, credit score changes and more.

A purchase annual percentage rate (APR) determines the amount of interest added to an outstanding credit card balance each month. While the rate is calculated by the year, the interest rate charge is added monthly to the unpaid balance. Most credit cards include a purchase APR that the issuer uses to calculate the interest.

While APR is an annual percentage rate, credit card interest is applied monthly by calculating one-twelfth of the APR. For example, a credit card with an APR of 24 percent would have a 2 percent interest charge added monthly to any outstanding balance.

Since APR only applies to outstanding balances, interest charges can be avoided entirely by paying off the full balance of a credit card by the due date each month.

Read on to learn more about different aspects of APR as well as real-world examples of how APR works.

Table of contents:

- What is a good credit card APR?

- How to determine what your purchase APR is

- Important aspects of credit card APR

- Examples of purchase APR

- Understand your APR to protect your credit health

What’s a good credit card purchase APR?

A “good” credit card APR can lead to better future offers and terms as cardholders demonstrate responsible financial habits and establish or maintain good credit.

The current average credit card APR is 22.16 percent, a 33 percent increase from the previous year. Any APR below this threshold is favorable, even though credit cards generally impose higher interest rates than other financial products like auto loans.

How to determine what your purchase APR is

Being aware of your purchase APR allows you to make informed decisions about your credit card usage and helps you understand the interest charges you may incur.

To determine your credit card purchase APR, you can start by checking your monthly credit card statement. Look for a section that mentions interest rates or the finance charge, as it should provide the APR associated with purchases.

You could also review the credit card agreement or terms and conditions provided by your card issuer. This information is typically available on their website, or you can request it by contacting customer service. You can also check your online credit card account, as it may display your current purchase APR. Remember to note any promotional or introductory rates that may apply, as these rates can change after a specific period.

How to lower your purchase APR

To save money on interest charges, you can negotiate a lower interest rate and APR with your credit card issuer. Some common methods include:

- Improving your credit: Reaching a FICO® score of 670 or higher increases your chances of qualifying for low-interest-rate cards, including those with introductory 0 percent APRs on purchases for up to 18 months.

- Consider a balance transfer card: You can look into getting a balance transfer card with an introductory zero percent APR for around 21 months, but be aware of transfer fees. Compare regular APRs and consider multiple issuers for the best credit card offers.

- Responsible credit card use: Paying bills in full and on time, reducing debt and minimizing credit utilization can also lead to lower APR cards.

Important aspects of credit card APR

Although APR is a straightforward calculation, there are a few important details to consider when looking at a credit card’s APR. Keep in mind that credit cards often have multiple APRs and that APRs can change over time.

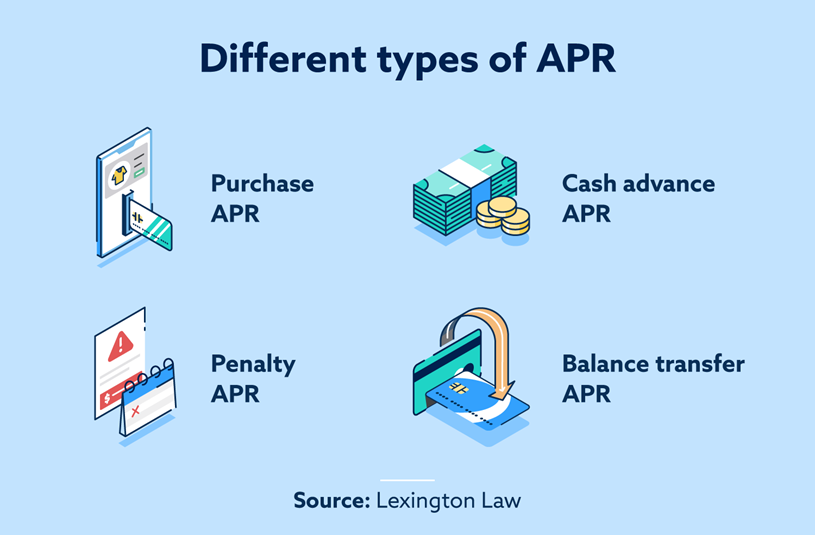

Other types of credit card APRs

When discussing APR, most people refer to a credit card’s “purchase APR,” also referred to as “standard purchase APR.” This is the rate that’s applied to regular purchases, including goods and services.

However, credit cards can do more than just make purchases, so there are several other APRs depending on the activity:

- Cash advance APR: If you use a credit card to receive a cash advance, you’ll pay interest according to the cash advance APR. Often, the rate for cash advances is higher than normal purchases. Also, interest typically begins to accrue immediately rather than after the due date for the monthly bill.

- Balance transfer APR: After you transfer a balance from any line of credit to a credit card, interest will begin to accrue at the rate set by the balance transfer APR. Some credit cards offer a promotional period where transferred balances accrue no interest.

- Penalty APR: When your credit card payments are late—typically by more than 60 days—many credit card companies will institute a higher penalty APR, which can affect both the outstanding balance as well as future purchases on the credit card. Penalty APRs can also be activated for other reasons outlined in a cardholder agreement.

Understanding these different kinds of APR makes it easier for you to use credit cards to their fullest while avoiding costly interest payments.

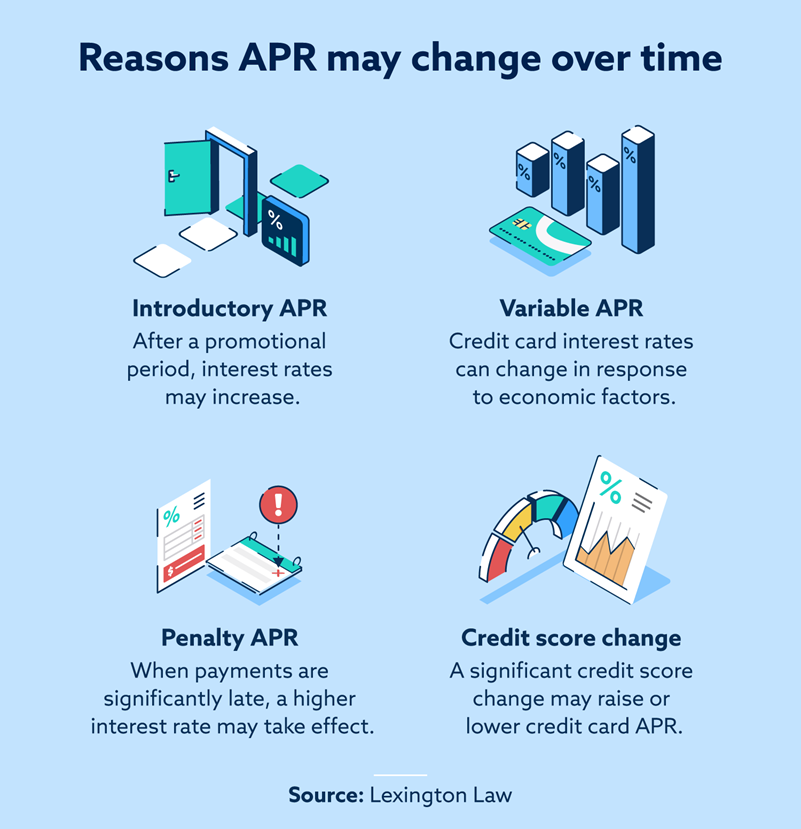

That said, it’s also important to note that APR is not a permanent number, and it can change over time for various reasons.

How your APR can change over time

The initial APR for purchases and other activities will be laid out in the cardholder agreement you sign when the card is issued. Typical APR ranges from 15 percent to 22 percent, but cards can have higher or lower APR for various reasons. In any case, the initial APR for your credit card may change over time.

Here’s what you need to know about how and why APR changes over time.

- Introductory APR: Some credit cards include a lower introductory or promotional APR for a set period of time, usually between three and 24 months after the credit account is opened. After the introductory period ends, a higher APR takes effect.

- Variable APR: Some credit cards have a variable APR that is tied to economic factors, like the “prime rate,” which is published by the U.S. Federal Reserve. As this number changes, the APR on your credit card will also change.

- Penalty APR: As noted above, certain actions—like late payments—can lead to a penalty APR that is often significantly higher than the standard APR. The APR often decreases again after six months or more of on-time payments.

- Credit score change: If you have a significant change in your credit score or credit report, the credit card company may raise or lower your purchase APR accordingly.

Although APR can change, credit card companies are generally not allowed to change your APR in the first year of your account’s existence. Credit card issuers typically provide notice at least 45 days before increasing a card’s APR. There are a few exceptions to this rule, however, like if your promotional period ends within the first 12 months of your account being opened.

Let’s take a look at some examples of how purchase APR works.

Examples of purchase APR

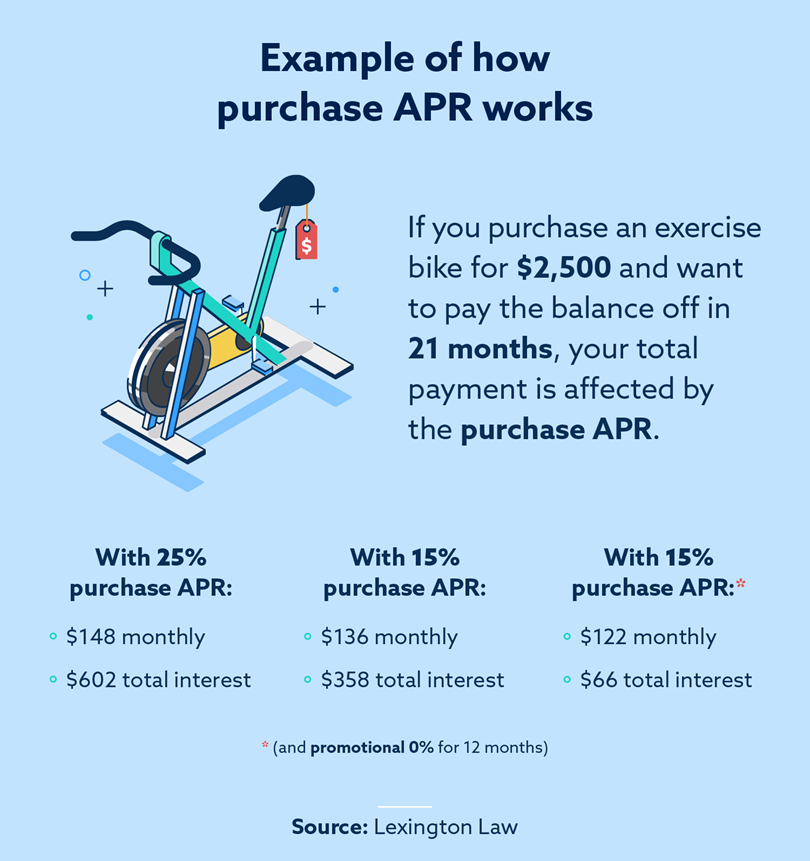

Looking more closely at different purchase APRs makes it clear that interest rates make a big difference when you carry a balance on your credit card.

Suppose you purchase a $2,500 exercise bike with your credit card and plan to pay off the balance over the next 21 months.

With a credit card that has a 25 percent APR, you’ll spend $149 each month to pay off the balance for that purchase, and you’ll have paid for more than $600 of interest along the way.

With a credit card that has a 15 percent APR, your monthly payment will be $136 until the balance is paid off, and you’ll accrue $358 of interest as you make payments.

With a credit card that has a promotional 0 percent APR for 12 months (then a 15 percent APR), your monthly payment will be $122, and you’ll only accrue $66 of interest over the course of the 21 months.

Understand your APR to protect your credit health

Purchase APR makes a huge difference when paying off credit card debt. It affects both how long it takes you to pay off your credit card and how much it will cost you, so understanding how your APR works will benefit you in the long run.

Getting a card with a low APR may depend on a person’s credit history. If you need help managing your credit profile, Lexington Law Firm provides qualified credit repair services. Get your free credit report assessment for your credit journey.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.