Bankruptcy will decrease your credit score, appear on your credit report for up to 10 years and make getting new credit very difficult.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Filing for bankruptcy can offer relief from overwhelming debt, but it will also have severe and long-lasting effects on your credit. Bankruptcy can remain on your credit report for seven to 10 years, and your score may take a significant hit in the immediate aftermath.

Rebuilding your credit after bankruptcy is possible, but it is often very difficult. Lenders may be hesitant to provide you with loans or credit cards, and securing low-interest funding can be challenging.

Learn how bankruptcy affects your credit, how bankruptcy appears on your credit report and what you can do to rebuild your credit afterward.

Key takeaways:

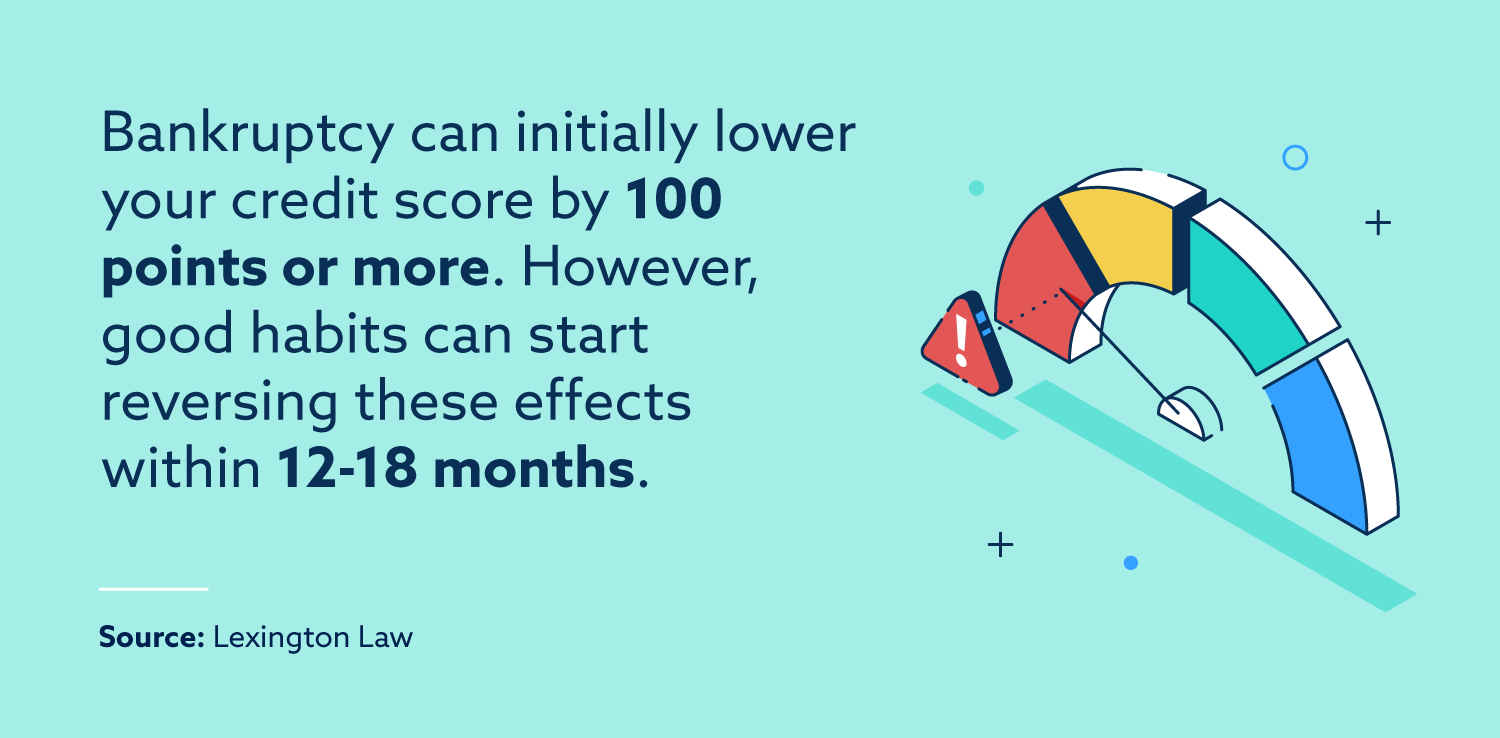

- Bankruptcy can cause your credit score to drop by as much as 240 points.

- Chapter 7 bankruptcy can stay on your credit report for 10 years. Chapter 13 can appear for about seven.

- It’s possible to remove bankruptcy from a report if there are errors.

What effects does bankruptcy have on your credit?

For anyone asking, “What is bankruptcy?” know that it’s a double-edged sword; on the one hand, you could free yourself from debt you had no possibility of paying back. On the other hand, filing for bankruptcy will make creditors feel less confident about their ability to repay borrowed funds.

Here are some of the immediate effects that bankruptcy can have on your credit:

- Your credit score may drop: Your score will take a hit after you file for bankruptcy, the extent varying from person to person.

- Your credit report will list your bankruptcy: Since bankruptcy is a public record item, it will appear on your credit report for seven to 10 years.

- You may not be able to get new credit easily: When you apply for a loan or credit card, lenders can see your credit report—and your bankruptcy may dissuade them from offering new credit regardless of your score.

Because bankruptcy comes with serious financial consequences, it’s important to weigh the advantages and disadvantages before proceeding. In most cases, filing for bankruptcy requires legal assistance—so it’s a good idea to contact an attorney and financial advisor to see whether your specific circumstances make bankruptcy a wise choice.

If you follow through on filing for bankruptcy and have your debt discharged, ensure you clearly understand how that decision will affect your credit score and credit report for years to come.

Myth: Having debt discharged through bankruptcy offers a complete financial reset.

Truth: In fact, while bankruptcy removes the obligation to pay debt, lasting effects can damage a person’s credit for years.

How much will your score drop after filing for bankruptcy?

The most common scoring model is provided by FICO®, which can drop after a bankruptcy notation. The impact of bankruptcy on credit scores varies from person to person; depending on your previous credit history, you could see a modest or a massive drop in your score.

Here are a few general rules to keep in mind when considering how your score may be affected by bankruptcy:

- Bigger drops for higher scores: For example, someone with a 780 score could see a drop of up to 200 points, whereas someone with a 670 score may only see a drop of around 150 points.

- Score changes are not permanent: You can eventually rebuild your score with responsible credit usage and time. Bankruptcy will eventually fall off your report after seven to 10 years.

- Chapter 7 vs. Chapter 13 bankruptcy: Chapter 7 bankruptcy can potentially absolve all approved debts and can remove secured debt if a property is offered. Chapter 13 implements a repayment plan while letting people hold on to their property.

Although it’s hard to predict exactly how your score will be affected by anything, there are ways to estimate the impact of filing a bankruptcy.

First, find out your current credit score, which is provided for free by many banks and financial apps.

Second, use the myFICO Score Estimator, which asks 10 questions to determine a rough score range. You can answer some of these questions hypothetically—like saying that you’ve filed for bankruptcy—to see how your score changes.

Your credit score is not a fixed number. With time and responsible credit usage, you can often raise your score, enabling access to credit with lower interest rates.

Myth: There’s a specific credit score drop associated with bankruptcy.

Truth: Actually, the severity of a score drop depends on various factors, like a person’s current credit score and previous negative items.

How does bankruptcy show up on your credit report?

Bankruptcy discharge is part of the public record, and it appears as a negative item on your credit report. As a result, when a lender views your credit report via a hard inquiry, your bankruptcy notation will be visible.

That said, the Fair Credit Reporting Act (FCRA) has specific guidelines for how long bankruptcies remain on your credit report.

- Chapter 7 bankruptcy can stay on your report for up to 10 years from the date you filed.

- Chapter 13 bankruptcy can stay on your report for up to seven years from the date you file.

Since Chapter 7 and Chapter 13 function differently, lenders may view the two types of bankruptcy differently when making decisions about new credit. Specifically, while Chapter 7 bankruptcy discharges most debt without payment, Chapter 13 establishes a payment plan, which a potential lender could consider more favorable.

Regardless of whether you’ve filed for bankruptcy, regularly checking your credit report is a good habit. Everyone is entitled to a free credit report every year from each of the three credit bureaus: Equifax®, Experian® and TransUnion®.

Occasionally, credit reports include false or misleading information. For example, if there’s an error on your report after seven to 10 years, it helps to know how to remove a bankruptcy from your record. Should a bankruptcy show up on your credit report in error, you can file a dispute with a 609 letter to potentially have it removed.

Looking over your credit report can also give you clues about how to work to rebuild your credit after bankruptcy.

Myth: A bankruptcy remains on your credit report forever since it’s part of the public record.

Truth: While bankruptcy remains an item in the public record, it’s only noted on a credit report for seven to 10 years.

How can I rebuild my credit?

Even though bankruptcy can take a significant toll on your credit, it is possible to rebuild your credit with time and a few key habits.

Try to stick to the following strategy when rebuilding your credit after bankruptcy:

- Set a goal: Figure out what score you’re trying to achieve and why. Do you want to buy a car or a house and get a great interest rate on your loan? Setting a specific goal helps you keep the finish line in sight.

- Review your financial habits: Find out what habits, circumstances and financial decisions made bankruptcy necessary in the first place. Making incremental changes in those areas of your life will help you along the way.

- Learn what affects your credit score: Knowing what leads to a good credit score can help you make better decisions. For example, making on-time payments and keeping your overall credit utilization low can make a big difference.

- Get new credit—when you’re ready: Rebuilding your credit requires you to use credit, but only when you’re ready. In many cases, a secured credit card (backed by a deposit) is a great first step after bankruptcy.

- Monitor your progress: Learn how to check your credit score and regularly review your report to get another perspective on your habits.

Reestablish your credit with Lexington Law Firm

While rebuilding credit can be difficult, it is important to remember that the damaging effects of bankruptcy and other negative items diminish over time. Consistent and responsible use of credit will start to outweigh the effects of your bankruptcy—and eventually, the bankruptcy will leave your credit report entirely.

Whether you’ve already had your bankruptcy discharged or you’re just exploring the possibility, know that you can always rebuild your credit. Lexington Law Firm’s focus tracks can help you find your footing after major life events. You can also sign up for a free credit assessment for an in-depth look at your credit situation.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.