The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Bankruptcy is a legal process that individuals and businesses can undertake to eliminate their debts under the oversight of a bankruptcy court.

Bankruptcy is a legal process that individuals and businesses can undertake to eliminate all or part of their debts under the oversight of a bankruptcy court. For individuals who have amassed debt beyond what they can reasonably pay, bankruptcy is a potential path toward a clean slate.

There are different types of bankruptcy, important terms to know and significant consequences to watch out for. If you’re wondering, “What is bankruptcy?” or you’re considering it for yourself, read on to get an overview, or you can use the links below to jump to a specific question.

- How does bankruptcy work?

- What are the different types of bankruptcy?

- What does it mean when bankruptcy is discharged?

- What is the benefit of filing for bankruptcy?

- How does bankruptcy affect your credit score?

- Bankruptcy terms you should know

- What does it cost to file for bankruptcy?

- Should you declare bankruptcy?

How does bankruptcy work?

Bankruptcy is a complicated legal process that involves several steps:

- A debtor files a legal petition for bankruptcy in federal bankruptcy court.

- The court appoints a trustee to oversee the case.

- The trustee examines the debtor’s assets and liabilities and determines if they have any assets which can be administered by the trustee.

While it’s technically possible to file for bankruptcy on your own, working with a qualified attorney is recommended, as the amount of legal knowledge required is beyond what the average person possesses.

During the creditor’s meeting the trustee will examine the debtor and the case and file a report. What happens next depends on whether you filed for Chapter 7 or Chapter 13. In both cases, your debt can be discharged, but the process for achieving that end varies.

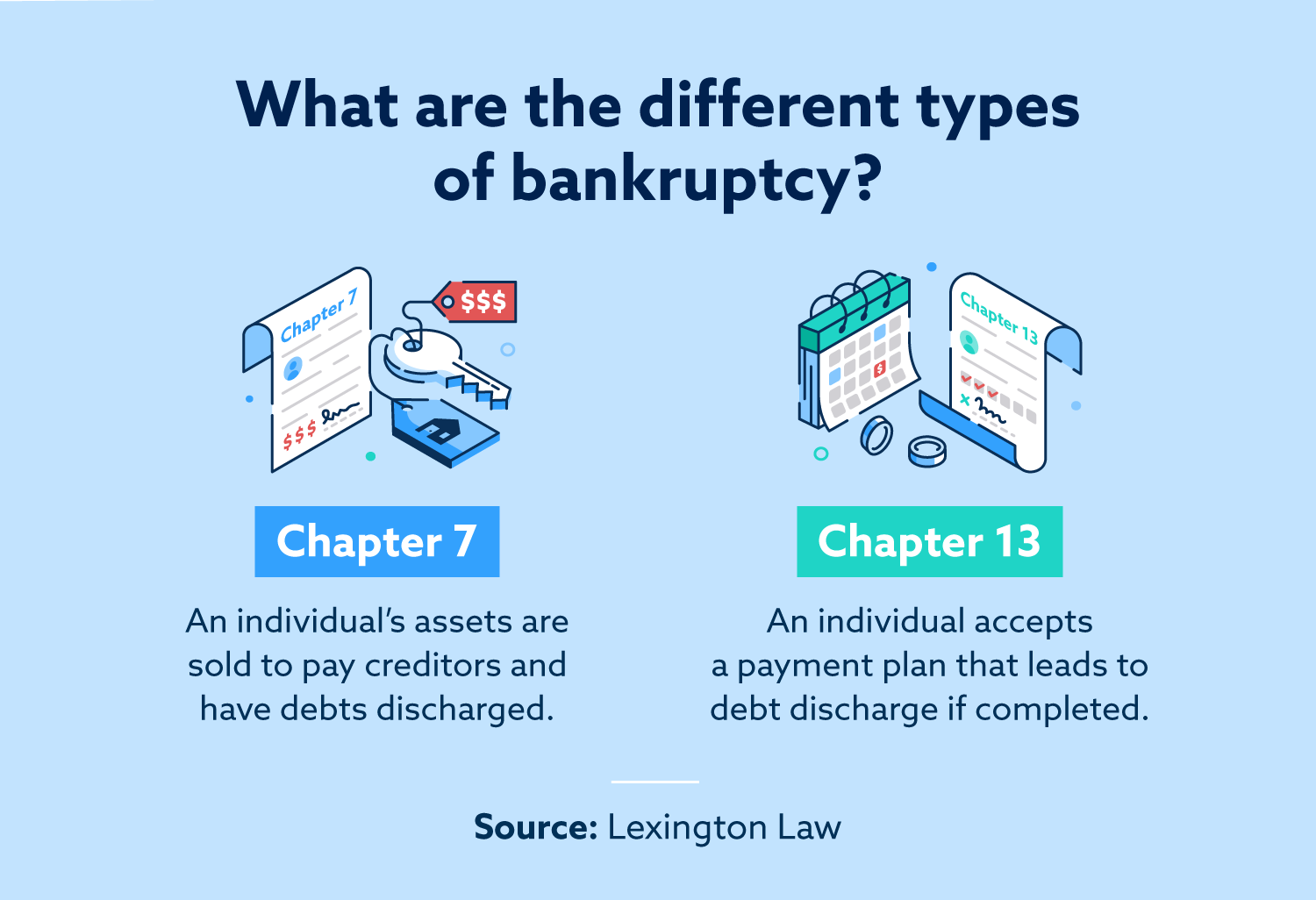

What are the different types of bankruptcy?

For individuals, the two most common forms of bankruptcy are Chapter 7 and Chapter 13. Businesses and local governments can also file for bankruptcy, but we won’t cover those types of bankruptcy in detail in this article.

Chapter 7

Chapter 7 bankruptcy is the most straightforward approach to filing for bankruptcy. Chapter 7 bankruptcy, also called liquidation bankruptcy or fresh start bankruptcy, sometimes involves the sale of assets to pay off debt. In most cases a debtor’s assets are exempt and no assets need be sold. This is best for debtors who have no way to repay their debt.

When a debtor files for Chapter 7 bankruptcy, the following process takes place:

- The debtor provides the trustee with tax returns and other financial documents relevant to the case, plus a list of all their assets.

- The trustee evaluates the assets to determine which assets, if any, are nonexempt.

- The trustee sells all nonexempt assets to pay off creditors. Debtors can keep exempt property, which varies by state law. For example, in New York, a debtor can keep their car if they own it outright and it is worth $4,000 or less.

- The debtor meets with their trustee and creditors at a Meeting of Creditors, also called a 341 Hearing, to verify the information they’ve filed in their bankruptcy petition is accurate.

- The trustee might pay some of the debt using the proceeds from liquidating the debtor’s nonexempt assets. However, this is rare.

- Any remaining debt is discharged. However, Chapter 7 does not eliminate all debt—debtors are still responsible for paying court-order alimony and child support, student loans and certain taxes.

The Chapter 7 process typically takes about four to five months from filing to final discharge of debt.

While Chapter 7 bankruptcy has powerful effects on debt, it also has consequences. The negative item from bankruptcy can remain on a credit report for 10 years.

A debtor can only file for this kind of bankruptcy once every eight years. For that reason, a condition of bankruptcy is always credit counseling and personal finance courses, which are aimed at supporting people to prevent them from ending up in the same financial situation again.

Chapter 13

Chapter 13 bankruptcy still leads to debt elimination, but it involves a debt payment plan. In Chapter 13 bankruptcy, debtors keep their property and pay debts over an agreed-upon period, usually three to five years. To qualify, a debtor must prove they have regular income. During the payment period, creditors are legally prohibited from collection efforts against the debtor. This type of bankruptcy is best for debtors who have steady income but still can’t afford to pay their debts in full.

If a debtor files a petition for Chapter 13 bankruptcy, the following will occur:

- The court reviews the repayment plan. Typically, repayment plans last three to five years and may repay some or all of the debt owed. The debtor prepares and files the plan and creditors have a chance to comment on it, the trustee comments on it and the court makes a final determination as to whether to approve the plan.

- A court-appointed trustee collects your payments. Over the course of repayment, a trustee will collect funds and disburse them to creditors.

- After repayment, the bankruptcy is discharged. After the specified repayment period, the debtor becomes eligible for a discharge. If the debtor has complied with the trustee’s requests, has paid all required payments and takes a financial management course, then the remaining balance on debt (if any) is forgiven.

The entire Chapter 13 bankruptcy process can take up to five years from the filing date to the end of repayment.

While Chapter 13 bankruptcy also has detrimental consequences for credit and general financial health, it tends to be less detrimental than Chapter 7 bankruptcy.

Additionally, Chapter 13 bankruptcy remains on a credit report for just seven years, and the process can be repeated more often if necessary. Having debt discharged or reorganized can be a vital financial tool.

Other types of bankruptcy

While individuals file Chapter 7 and Chapter 13 depending on their circumstances, there are other types of bankruptcy that farmers and fishermen, businesses and city governments can use in difficult financial situations.

Here’s a quick overview of other forms of bankruptcy:

- Chapter 9 focuses on local governments and school districts that need to restructure debt in the wake of financial troubles. Similarly to Chapter 13, Chapter 9 utilizes a debt repayment plan.

- Chapter 11 enables businesses to create a debt repayment plan in conjunction with a revised business plan that is aimed at increasing profitability.

- Chapter 12 is a narrowly focused form of bankruptcy that is exclusive to family farmers and fishers hoping to avoid liquidation.

- Chapter 15 is an international provision that helps mediate bankruptcy proceedings that involve the United States and at least one other country.

While all of these forms of bankruptcy are useful, only Chapter 7, Chapter 11 and Chapter 13 typically directly affect individuals in financial distress.

What does it mean when bankruptcy is discharged?

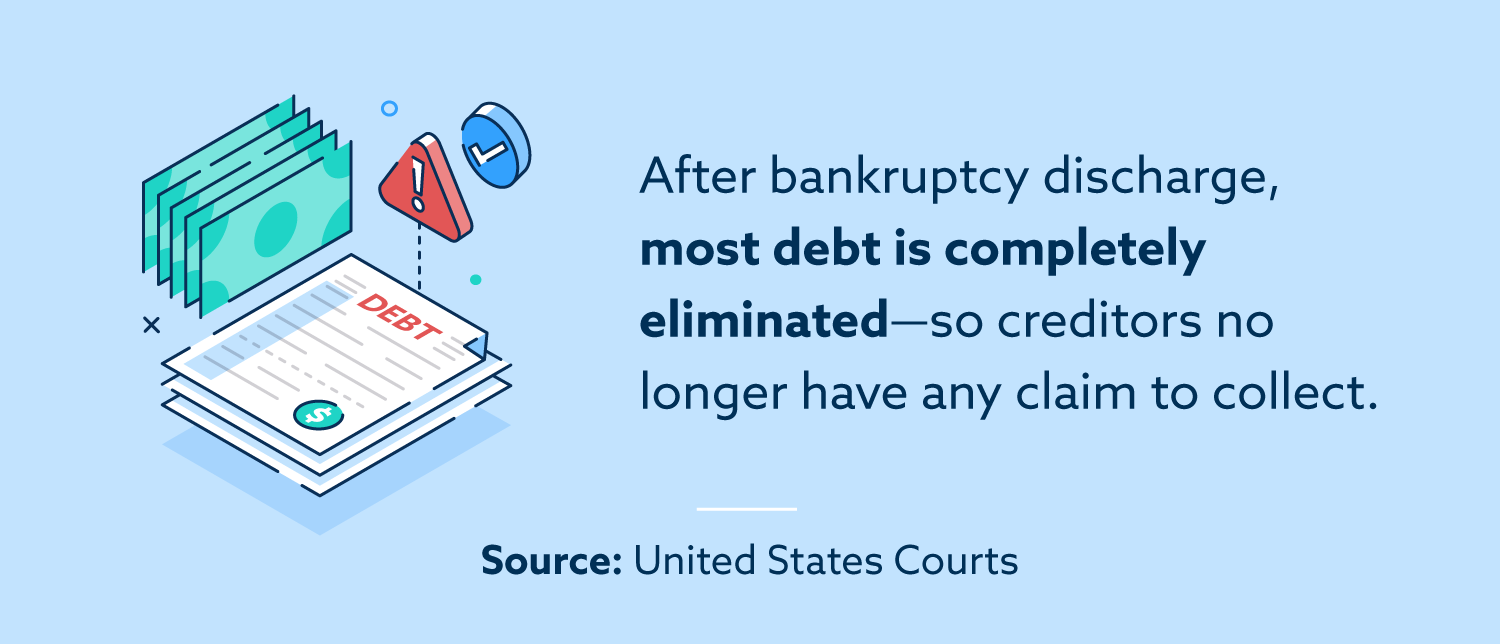

A bankruptcy discharge means a debtor is no longer personally responsible for certain debts. Regardless of the remaining balance of a previous debt, once a bankruptcy discharge is entered, creditors can no longer collect on the debt.

- With Chapter 7 bankruptcy, discharge usually occurs after the creditor’s meeting. There is typically a 60-day window after the meeting of creditors for creditors to file complaints, after which the discharge may take effect.

- With Chapter 13 bankruptcy, discharge typically takes place after the repayment plan is completed.

However, not all debts are eligible for bankruptcy discharge. Depending on the type of bankruptcy filed, the following debts may not be discharged:

- Alimony

- Child support

- Tax liens

- Some federal, state and local taxes (depending on the age of the debt)

- Student Loans.

- Debts for willful and malicious injury to a person or property

- Debts for death or personal injury caused by the debtor driving while under the influence of alcohol or drugs

- Any debt not listed in the bankruptcy filing

In general, a discharged bankruptcy is permanent, meaning creditors no longer have any claim to previous debt. In some cases, however, a bankruptcy discharge could be revoked if the party proves to the court that the initial petition was made fraudulently. The time period for taking an action in this way is limited to one year after discharge.

What is the benefit of filing for bankruptcy?

There are advantages to filing for bankruptcy for individuals who can no longer deal with overwhelming debt.

Some of the most important benefits of bankruptcy include:

- The elimination of many types of debt

- A fresh start with finances

- An end to calls and letters from collection agencies

- Relief from wage garnishment, foreclosure or repossession

- Protection of certain kinds of property

Bankruptcy courts exist for a reason, and bankruptcy serves an important financial function for many individuals whose debts significantly exceed their ability to repay. For those who have no other good options, bankruptcy provides important benefits and the chance for relief and a second chance at financial security.

How does bankruptcy affect your credit score?

Bankruptcy has a serious detrimental effect on your credit, though it is possible to rebuild credit after bankruptcy.

The negative item from bankruptcy will remain on your report for seven to ten years, depending on the type of bankruptcy. Any time you apply for credit, that negative item will be visible to creditors, who will factor it in when deciding whether to approve your application.

For those looking to rebuild credit after bankruptcy, a secured credit card is often the best starting point. A secured credit card is backed by a deposit, so creditors are usually willing to provide it even to those who have a bankruptcy on their record. Responsibly using the card and making payments on time can slowly lead to improved credit in the future.

Additionally, many people who have gone through bankruptcy choose to work with a credit repair company, which may be able to support the process of rebuilding credit.

Bankruptcy terms you should know

A bankruptcy score is used by financial institutions to predict the likelihood that an individual will file for bankruptcy within a certain period of time. Similar to credit scores, bankruptcy scores are calculated using a wide variety of factors. Unlike credit scores, however, bankruptcy scores are not available to consumers, so you can’t know your own score or make efforts to improve it directly.

Still, regardless of your bankruptcy score, the same financial habits that support a strong credit score are also likely to help prevent you from needing to file for bankruptcy:

- Create and maintain a budget. Spending within your means and prioritizing essential expenses is an excellent way to maintain financial health.

- Make full and on-time debt payments. Make timely payments for loans and credit cards, and avoid keeping a credit card balance from month to month.

- Avoid unnecessary lines of credit. While credit is a valuable tool, it’s important to avoid opening too many lines of credit and letting debt become overwhelming.

Bankruptcy scores are important tools for financial institutions making lending decisions, but they are largely unimportant to consumers. As long as you are making wise financial decisions over time, creditors will continue to recognize your efforts and your risk of bankruptcy will remain low.

Bankruptcy terms you should know

As you navigate bankruptcy, you’ll come across a variety of terms that may be unfamiliar. Understanding all of these terms makes navigating the process of bankruptcy much easier, and fortunately, none of them are difficult to understand.

Here’s a list of terms that you should know if you’re trying to understand bankruptcy better.

- Assets and liabilities: An asset is anything you own, whereas a liability is anything you owe.

- Chapter: A chapter is simply the specific type of bankruptcy being declared under Title 11 of the United States Federal Bankruptcy Code.

- Discharge: A discharge means the associated dischargeable debts no longer need to be paid.

- Lien: A lien is a claim against a piece of property from a creditor who is owed a debt, such as a mortgage lender or a car creditor.

- Liquidation: Liquidation is the process of selling assets, usually to pay debts—for instance after filing Chapter 7.

- Means test: The means test is used to determine who is eligible to file for Chapter 7 by accounting for income and debt.

- Repayment plan: An approved repayment plan is a court-authorized plan to give creditors back some or all of what they are owed. At the completion of a repayment plan under Chapter 13, remaining dischargeable debt is typically forgiven.

- Secured and unsecured debt: A secured debt has some sort of valuable property as collateral—for instance, an auto loan is secured by the car itself. An unsecured debt has no associated collateral—for instance, a credit card is unsecured.

- Trustee: Appointed by the court, the trustee is responsible for reviewing the debtor’s financial situation and documentation relation thereto, conducting the meeting of creditors and collecting and liquidating non-exempt assets or ensuring payments are made according to the repayment plan.

Armed with knowledge of these terms, you’ll have a much greater understanding of bankruptcy moving forward.

What does it cost to file for bankruptcy?

The cost to file bankruptcy can be broken down into two parts: court fees and attorney fees. According to the U.S. Court, you’ll pay a $78 administrative fee and a $15 trustee fee to file for Chapter 7 or Chapter 13 bankruptcy, plus any additional relevant fees. The total filing cost is generally under $500.

If a debtor cannot pay the fees associated with filing for bankruptcy, the court may break the fee payment into up to four installments or waive them altogether. Debtors who wish to have the fee waived must submit Form 103B. Bankruptcy filing fees are not typically waived, even for the most destitute.

That said, most people will also require an attorney for bankruptcy proceedings, and fees can vary significantly. According to All Law, fees for Chapter 7 typically range from $1,000 to $3,500, whereas fees for Chapter 13 are a bit higher, ranging from $2,500 to $6,000. Depending on your location, fees may be lower or higher, so you’ll want to consult a local lawyer to determine a more accurate cost before proceeding.

Should you declare bankruptcy?

Deciding whether or not to declare bankruptcy can be difficult, so make sure you think about all of the alternatives first. People often consider bankruptcy due to unexpected or overwhelming debt—like a medical bill that has ballooned through interest or a handful of loans that have become unmanageable.

There may be ways to deal with these debts before resorting to bankruptcy. For example:

- Negotiate with your creditors. Ultimately, creditors are looking for you to repay your debt. By contacting your creditors, you may be able to work out a favorable payment plan or have some of your debt erased in order to make it more manageable.

- Get a debt consolidation loan. A debt consolidation loan enables you to simplify and often reduce your debt payments by lowering your interest rate or extending your payment timeline.

- Work with a credit counselor. A credit counselor may be able to help you evaluate your entire financial picture and create an action plan to make debt more approachable.

Still, even after these alternatives, there are some people for whom bankruptcy is the best available option. If you have no means to pay back your debts and you’ve exhausted other options, contact a bankruptcy attorney to determine your best next steps.

Overall, bankruptcy exists to protect individuals from long-term financial ruin. Though the credit consequences of bankruptcy are long-lasting, the benefits of freedom from debt are absolutely essential in some cases.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.