A late payment can stay on your credit report for up to seven years, starting from the date it was first reported as delinquent, not from your original due date.

Table of contents

- How Long Do Late Payments Stay on Credit Reports?

- What counts as a late payment

- How long a late payment actually stays on your report

- How late payments affect your score

- How to remove a late payment from your report

- Minimizing the impact of an accurate late payment

- How to avoid late payments going forward

- Get additional help for managing late payments on your credit report

- Frequently Asked Questions

How Long Do Late Payments Stay on Credit Reports?

If you’ve seen your score drop after a missed payment, here’s the direct answer: a late payment can stay on your credit report for up to seven years, starting from the date it was first reported as delinquent. Below, we cover how that clock actually starts, how much a late payment affects your score, how to get an inaccurate one addressed, and how to minimize the impact of one that’s accurate.

What counts as a late payment

A payment is late once it passes the due date your lender set. Each lender defines its own threshold for when a late payment gets reported to the bureaus, but as a general rule, payments made within 30 days of the due date typically stay off your report, even though you may still owe a late fee to the lender directly. This 30-day cushion isn’t a law; it’s a widely followed industry practice tied to how often lenders report to the bureaus.

Federal student loans are a notable exception: they’re typically not reported delinquent until 90 days past due, rather than 30.

Late payments apply to more than credit cards. Car loans, mortgages, and personal or business lines of credit all report delinquencies the same way.

How long a late payment actually stays on your report

Once a payment is reported delinquent, the seven-year clock starts from that report date, not the due date. For example, if a payment was due in early 2026 but wasn’t reported delinquent until several weeks later, the seven years run from that later report date, even if you bring the account current shortly after. This lines up with guidance from the Consumer Financial Protection Bureau on how long negative information can stay on a report.

Your credit report shows the exact date the late payment was reported, so that’s the date to track. If you’re not sure where to find it, see our guide on how to read your credit report.

How late payments affect your score

The size of the hit depends on a few factors. Frequency matters: a single late payment does less damage than a pattern of them. Your starting score matters too, since late payments tend to hurt higher scores more than lower ones. And the number of accounts affected compounds the impact if more than one goes delinquent at the same time, separately from factors like credit utilization or a new hard inquiry, which have their own effect on your score.

The effect also fades with time. A late payment from three years ago carries much less weight than one from last month, even though both may still be visible on the report.

How to remove a late payment from your report

If you believe a late payment is being misreported, the Fair Credit Reporting Act gives you the right to dispute it directly with the credit bureau that reported it.

- Check for inaccuracy first. Automated and online payment systems occasionally misregister a payment. Keep confirmation numbers or payment emails so you have proof if you need to dispute it.

- Contact your lender. If they confirm the error, ask for written documentation stating they’ll correct it.

- Get documentation regardless of outcome. If the item doesn’t come off your report within a month or two, you’ll need this for the next step.

- If your lender won’t resolve it or the timeline stalls, move on to filing a dispute with the credit bureau directly, or look into removing late payments from your report more broadly.

Minimizing the impact of an accurate late payment

If the late payment is accurate, there are still a few paths worth trying.

Write a goodwill letter. Explain the circumstances plainly, note that it won’t happen again, and point to your broader payment history. Lenders are generally more receptive when the late payment was small, isolated, or clearly out of character for the account. See our guide on writing a goodwill letter for a template to start from.

Negotiate directly with your lender. Lenders usually want two things: to get paid, and to keep you as a customer using their credit line. A larger-than-minimum payment, or an offer to bring the balance current in exchange for reconsidering how the account was reported, can sometimes open the door to a resolution, especially if you catch the issue before it’s actually reported to the bureaus. Some readers also send a pay for delete letter as part of this conversation, though lenders aren’t obligated to agree to it.

Consider a third party if you’d rather not handle it yourself. A credit repair service or law firm can manage the negotiation and documentation on your behalf. See our guide on vetting a credit repair company before you hire one, since this space attracts bad actors who promise guaranteed removals they can’t deliver.

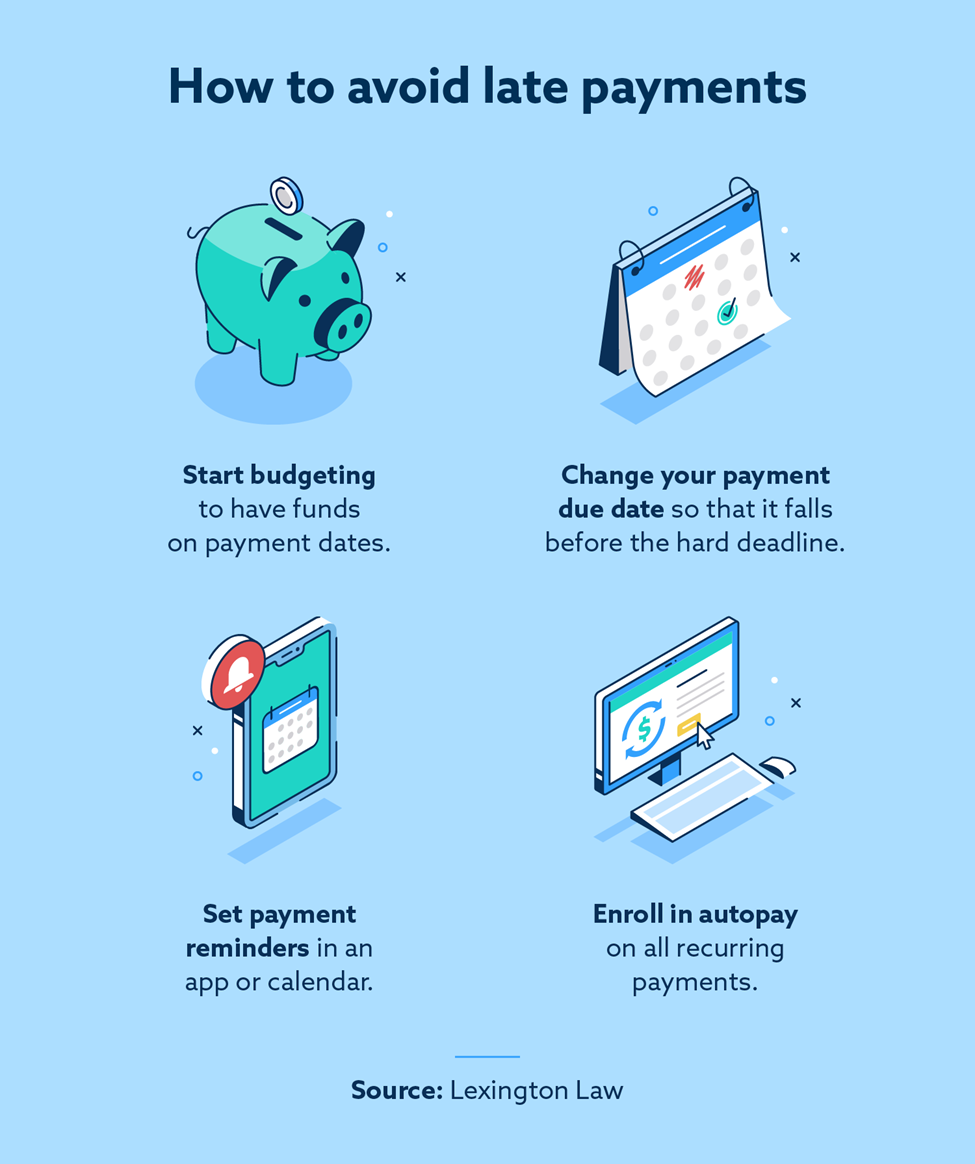

How to avoid late payments going forward

A few habits go a long way toward preventing the next one:

- Budget around your due dates, setting money aside for upcoming payments before the date arrives rather than after.

- Move your due date to better line up with your pay schedule, if your lender allows it.

- Set reminders, whether through a calendar app, a smartphone alert, or a note somewhere you’ll actually see it.

- Set up autopay, and check whether your lender allows splitting a payment into weekly or biweekly installments instead of one lump sum.

These habits are also part of a broader strategy for improving your credit overall, not just avoiding late payments specifically.

Get additional help for managing late payments on your credit report

A late payment is easier to prevent than to undo. If one is already on your report, we can review your file, help you evaluate whether it’s accurate, and challenge items that appear inaccurate, unfair, or unverifiable with the credit bureaus. If you need assistance with filing a dispute or addressing a late payment on your credit report, contact us today for a consultation.

Frequently Asked Questions

How long does a late payment affect my credit score?

The impact fades over time. A late payment from several years ago carries far less weight than one from the past few months, even though it can remain visible on your report for up to seven years.

Can a late payment be removed early?

Only if it’s inaccurate, or if your lender agrees to a goodwill adjustment. There’s no guaranteed way to remove an accurate late payment before its reporting period ends.

No. Paying the balance brings the account current, but the late payment itself typically still shows in your payment history for the reporting period.

A payment made after your lender’s due date. Many lenders don’t report a payment as late to the bureaus until it’s roughly 30 days past due, though late fees can apply sooner.

No. Federal student loans are generally not reported delinquent until 90 days past due, a longer window than most other credit types.

A single late payment can cause a noticeable drop, especially for higher scores, but it’s rarely catastrophic on its own and its effect lessens over time.

Note:

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.