The 28/36 rule is a financial rule of thumb that measures a borrower’s ability to pay off their mortgage by evaluating their financial health.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Around 27 percent of homeowners in the United States who hold mortgages are grappling with housing cost burdens. How should homeowners better prepare themselves for handling a home loan before accruing too much debt?

Achieving a secure and balanced financial life involves navigating through suggested guidelines and best practices. Among these is the 28/36 rule—a framework for financial decision-making.

In this article, we will break down what the 28/36 rule entails and how it can serve as a valuable tool for homeowners looking to budget more effectively.

Table of contents:

- What is the 28/36 rule?

- Front-end ratio: the 28 percent

- Back-end ratio: the 36 percent

- How does the 28/36 rule affect my ability to get a mortgage?

- Exceptions and special considerations

- 28/36 rule FAQ

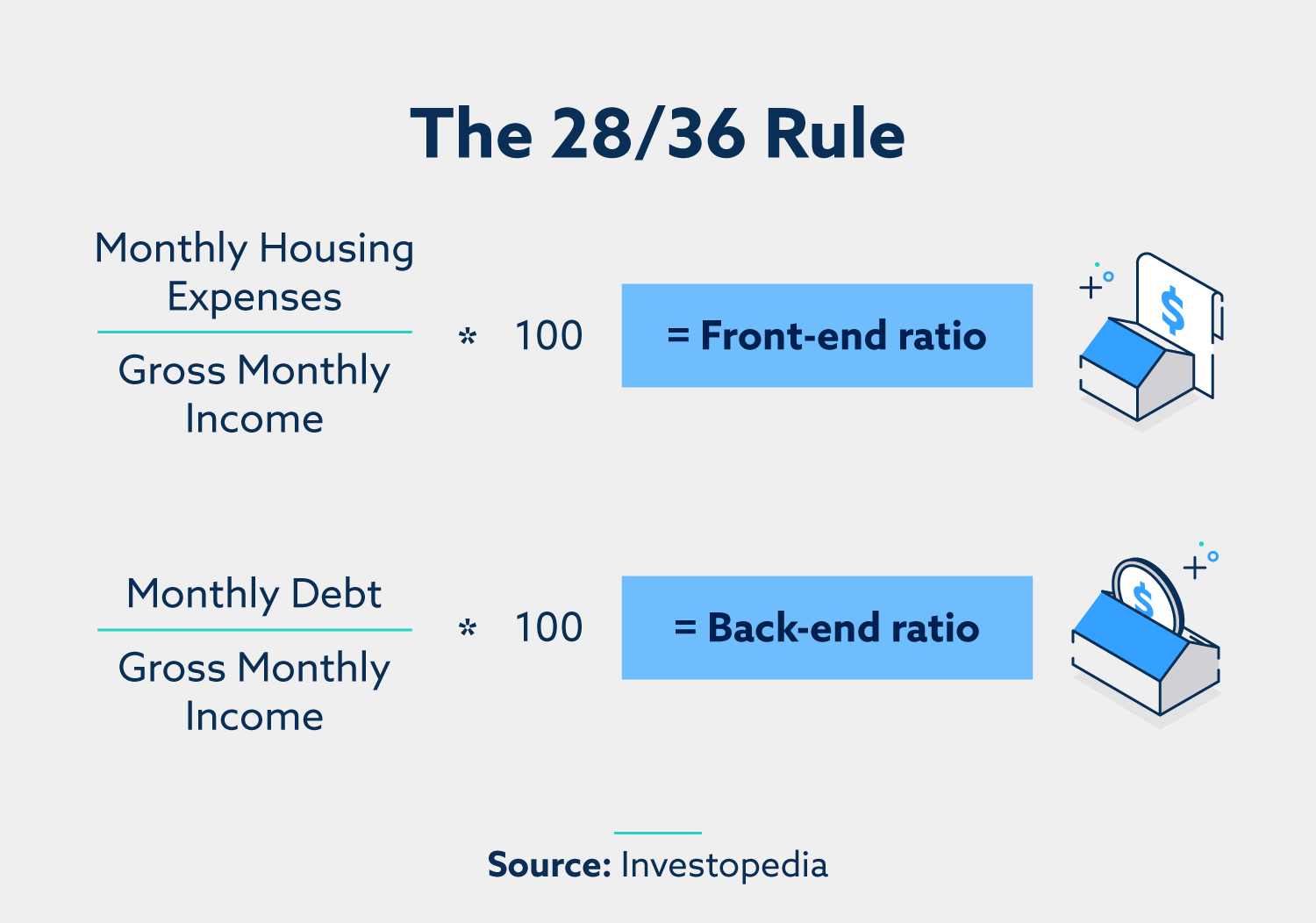

What is the 28/36 rule?

The 28/36 rule is a financial rule of thumb that measures a borrower’s ability to pay off their mortgage by evaluating their financial health.

The rule advises households to limit their spending on housing expenses to under 28 percent of their gross monthly income and their spending on all debt to under 36 percent of their gross monthly income.

This suggestion is particularly important for households planning to take on a mortgage, as lenders use it to decide if they will extend credit to borrowers.

Front-end ratio: the 28 percent

The front-end ratio, or the housing expense ratio, is a ratio that describes how much of one’s income goes toward housing payments. It is calculated by dividing housing expenses by gross income and should make up under 28 percent of total monthly income, according to the 28/36 rule.

You may be wondering what constitutes a housing payment. The following list details everything included in this category:

- Mortgage payments: This constitutes both how much money you borrow (principal) and the interest you pay on that borrowed money.

- Property taxes: It’s important to be aware of how high your area’s property taxes are, as they can vary drastically from locale to locale.

- Insurance: This includes both homeowners insurance and any added insurance on your house (tornado, earthquake, flood, etc.).

- HOA dues: Homeowner’s associations charge monthly dues. If you live under an HOA’s jurisdiction, be sure to add them to the equation.

You might have noticed that utility bills, internet and cable TV services are not listed. Although they are typically grouped under the umbrella term of “housing expenses,” they aren’t part of the calculation that lenders make to determine your financial health.

To better visualize the front-end ratio, imagine you have a gross monthly income of $4,500 per month ($54,000 annually). Every month, your mortgage payments come out to $1,250, your property taxes are $200, and your homeowner’s insurance costs $100. You don’t live in a neighborhood with a homeowners association, so there are no HOA dues.

Added together, your housing payments come out to $1,550. Divide that by your monthly income ($4,500), and you have a front-end ratio of 0.34, or 34 percent. Because it’s more than 28 percent, this would signify that you should pursue additional income, move somewhere that is less expensive to live or both to have a chance at a decent mortgage.

Back-end ratio: the 36 percent

The back-end ratio, represented by the “36” in the 28/36 rule, is the ratio measuring how much of one’s income is used to pay off debt every month. This encompasses mortgage payments, student loans, car loans, credit card debt and all debt in between.

It’s calculated by dividing the amount of monthly debt owed by gross monthly income.

Since child support and alimony payments are also included, it’s important to take a comprehensive look at all of your expenses in this category to ensure you fall below the 36-percent threshold before taking on any additional debt.

Imagine you have a gross monthly income of $3,500 per month ($42,000 annually). You haven’t accrued credit card debt, but your car loan and student loan payments come out to a monthly total of $600. Divide your total debt ($600) by your monthly income ($3,500), and your back-end ratio totals 0.17, or 17 percent.

How does the 28/36 rule affect my ability to get a mortgage?

If taking out a mortgage would cause your front-end ratio to go above 28 percent, or your back-end ratio to go above 36 percent, then it will probably be difficult to get the high mortgage loan and low APR you were hoping for. You may still qualify for a mortgage, but the lender will likely turn down your initial request and offer a smaller amount.

The 28/36 rule is just one of many factors that go into determining your ability to get an ideal mortgage. These factors determine the size of your loan, and thus what percentage of income should go to mortgage payments. They include:

- Credit score. Your credit score has a major impact on your mortgage rate. Lenders rely heavily on borrowers’ credit scores to determine their risk whenever considering whether to lend money. This holds especially true for a very large purchase like a home.

- Income. Whether you plan to take on a new mortgage or refinance a current mortgage, your income has an impact on your lender’s willingness to help out. A higher income communicates a better ability to pay off a mortgage, so we recommend pursuing a side income if your income won’t impress lenders as it stands.

- Size of down payment. Similar to income, larger down payments on a house (20 percent and higher) send a positive message to lenders by positively impacting both your front- and back-end ratios. It’s worth taking extra time to save up to make a larger down payment.

Exceptions and special considerations

While the 28/36 rule tends to be the gold standard for winning lenders’ trust, this rule primarily applies to conventional mortgages. If achieving these ratios doesn’t feel realistic at the moment but you’re serious about buying a home soon, you should be aware of other types of mortgage loans that are an exception to the rule.

Aside from having excellent credit and making a larger down payment, you may qualify for a government-insured mortgage. For example, the Federal Housing Administration (FHA), the U.S. Department of Veterans Affairs (VA) and the U.S. Department of Agriculture (USDA) all offer mortgages that allow for approval at higher front- and back-end ratios. If your home is energy efficient, it may further increase your ratio’s threshold.

| Type of mortgage | Front-end ratio | Back-end ratio |

|---|---|---|

| Conventional | 28% | 36% |

| FHA | 31% | 43% |

| FHA (Energy-efficient home) | 33% | 45% |

| VA | N/A | 41% |

| USDA | 29% | 41% |

28/36 Rule FAQ

Below are commonly asked questions about the 28/36 rule and finances.

What happens if you exceed the 28/36 rule?

If you find that you’re putting more money toward paying back debt and exceeding the 36 percent rule, you’ll need to reduce your debt before applying for a mortgage.

We recommend that you:

- Assess your financial situation: Determine your sources of income and debts.

- Create a budget: Develop a budget with your monthly gross income and expenses. Include your necessities, like groceries and utilities, as well as optional expenses, like eating out or going to the movies.

- Identify unnecessary expenses: Evaluate your optional expenses and decide which of them you can realistically cut back on.

- Prioritize your debts: Start paying your smallest debt balance first and work your way up, or start with your largest balance and work downward. Add this to your monthly budget plan.

Avoid allocating any new debt while you focus on paying off your existing debt. That way, you can stay focused on meeting the 28/36 rule and building a better financial portfolio for home buying.

What’s included in housing expenses?

Housing expenses include all costs associated with renting or owning a home. Housing expenses vary if you rent or own the home, but these are the most common for homeowners:

- Monthly mortgage payment

- Mortgage insurance premium (MIP)

- Property taxes

- Homeowners association (HOA) fees

- Home maintenance and repairs

- Homeowners insurance

Instead of mortgages, renters can include rent payments, renters insurance and utilities as some of their housing expenses.

What is gross income?

Gross income is the total income you earn before deductions and taxes are taken out. After deductions are taken out, the result is considered your “net income.” This is the amount you take home to pay off expenses and debt.

Your total debt from all loans should not exceed what percentage of your gross monthly salary?

Your total debt from all your loans should not exceed the 28/36 rule. Exceeding the rule puts you at a higher risk and may sway your lender to not approve you for a home loan.

In addition to alternative mortgage options, it’s important to consider what type of loan you want to pursue, whether it’s a home equity loan or a line of credit. How you’re going to buy a home is one of the most significant life decisions to make. As such, it’s important that you do your due diligence and think ahead. From improving your credit with the help of a credit monitoring service to paying off debt, there are a wide variety of ways to practice good personal finance in order to potentially qualify for the mortgage you want.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.